Direct Answer: Why Did Your Score Drop After You Paid Off Your Cards?

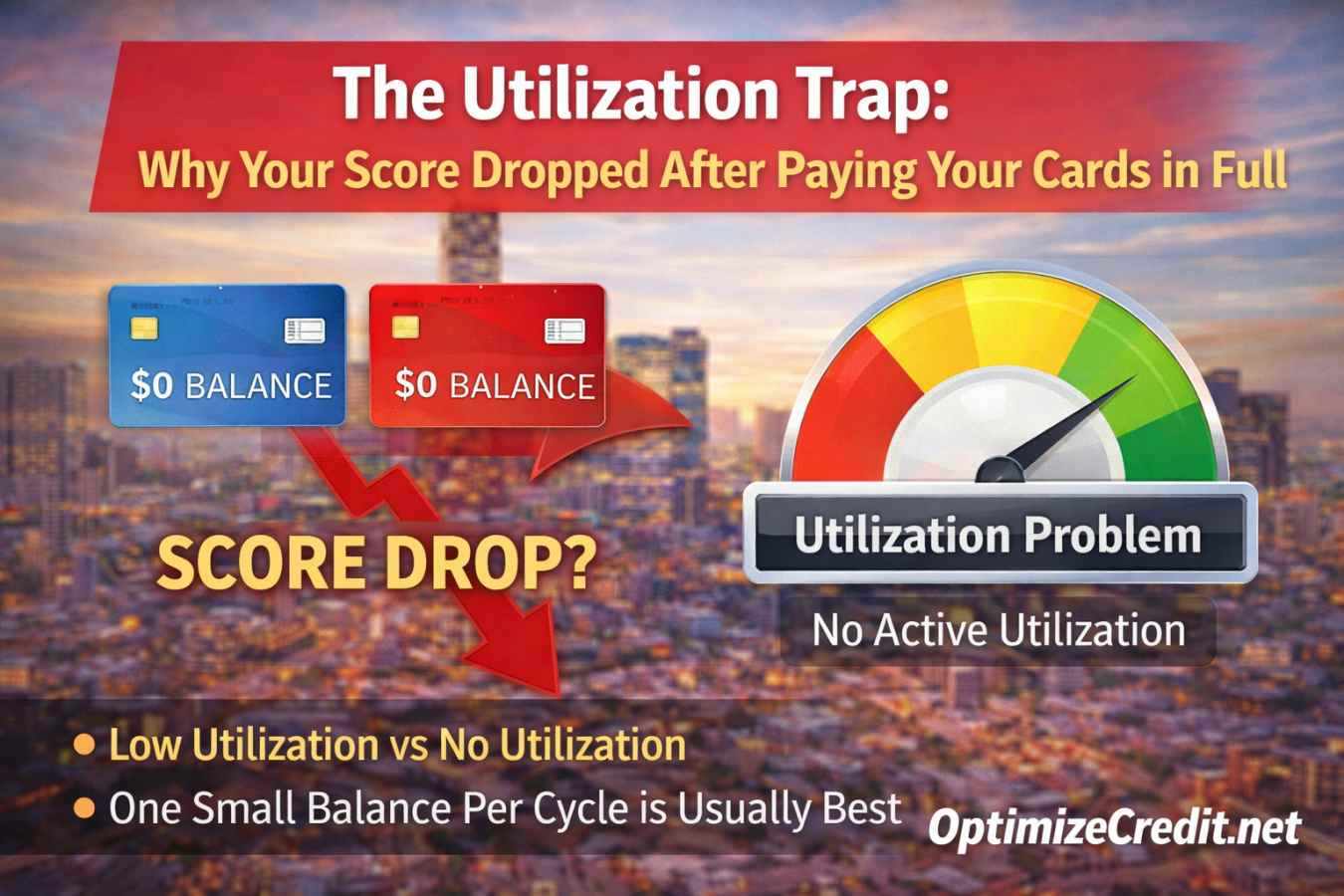

It feels like a betrayal: you pay your credit cards to zero, only to watch your score drop or refuse to rebound. In most cases, you have not hurt yourself financially. You have simply run into a scoring mismatch between what you owe now and what the bureaus still see. Sometimes you also trigger the all-zero issue, where every revolving account reports zero and the file scores slightly less efficiently than when one card reports a tiny balance.

Usually for one of two reasons:

- The high balance had already been reported, so the bureaus still show the old snapshot until the next cycle.

- Every card reported zero, which can be slightly less efficient for score optimization than one card reporting a very small balance.

Those are different problems. They need different fixes.

The First Trap: The Bureau Snapshot Was Already Locked In

This is the bigger one.

If your statement closed at a high balance on the 15th and you paid the card in full on the 18th, you did the right thing financially. But the credit bureau may still show the 15th snapshot until the next cycle updates.

That means you can:

- Owe less in real life

- Still look highly utilized on the report

- Still see a weaker score until the next reporting cycle finishes

That is why understanding the gap between statement dates and bureau updates is the natural companion to this concept. Your payment date and your reporting date are not the same event.

The Second Trap: The All-Zero Issue

A second, smaller issue appears when every revolving card reports zero.

For many files, all-zero reporting is completely fine. But in optimization mode, some score versions can score a little more efficiently when one card reports a tiny balance and the rest report zero.

That is where AZEO comes in.

What Is AZEO?

AZEO stands for All Zero Except One.

It is a score-optimization tactic, not a debt tactic.

The logic is:

- All cards except one report zero

- One card reports a very small balance

- The file shows low risk and active revolving use at the same time

This is why AZEO is best understood as a system hack for reporting, not a reason to carry debt.

A Statement Balance Is Not the Same as Carried Debt

This is the part that confuses people.

You do not need to pay interest to use AZEO.

A card can:

- Generate a small statement balance

- Report that small balance to the bureaus

- Then be paid in full during the grace period

That means the account can show activity for scoring purposes without you carrying interest-bearing debt month to month.

So when people hear "leave a balance," the correct interpretation is usually:

- Leave a small statement balance

- Do not carry an interest-bearing revolving balance if you can avoid it

How Small Should the Balance Be?

"Leave a small balance" is too vague to be useful.

For many optimization cases, a tiny reported balance — often roughly 1% to 3% on one card, or simply a small dollar amount such as $10 to $20 — is enough to avoid all-zero reporting without creating meaningful utilization pressure.

The point is not the exact dollar figure. The point is low reported usage.

Individual-Card Utilization Matters Too

A common mistake is thinking only about total utilization. For a deeper look at how credit limits, reported balances, and account age interact mathematically, the utilization math breakdown is worth reading.

Example:

- Overall utilization = 12%

- One card = 88%

- All other cards = 0%

That single card can still suppress the score even if the total file looks moderate. This is why someone can say "my total utilization is fine" while still seeing a score problem.

The utilization trap is often an individual-card problem, not just an aggregate one.

Why One Maxed-Out Card Can Hurt Even If Your Total Looks Okay

Scoring models look at both:

- Overall utilization

- Individual-card utilization

That means a high-balance card can create a risk signal even when the file average looks manageable. This matters most for borrowers close to an approval threshold, because a single card reporting very high usage can cost points at exactly the wrong time.

The optimizer catches these individual-card utilization traps automatically, flagging which specific card is suppressing your score before the next statement cycle locks in the snapshot.

A Simple Timeline Example

| Date | Event | What the Bureau Sees |

|---|---|---|

| 1st-14th | Card balance grows to $4,000 on a $5,000 limit | Nothing reported yet |

| 15th | Statement closes | 80% utilization may be reported |

| 18th | You pay the full $4,000 | Great financially, but the bureau may still show the 80% snapshot |

| Next cycle | Lower statement balance reports | Score can finally reflect the lower utilization |

That is why people feel "punished" after paying cards off. In many cases, they are seeing lag, not damage.

What About Credit Limit Decreases?

This needs perspective.

Paying your cards in full does not automatically trigger a credit limit decrease. That would be an overstatement. But prolonged inactivity, account dormancy, or broader issuer risk management can sometimes lead to limit reductions or closures later.

That is a separate problem from the immediate utilization trap.

The practical takeaway:

- Do not carry interest out of fear

- Keep useful cards active with occasional light use

- Preserve valuable limits if the account is otherwise worth keeping

Trended Data Makes One-Time Fixes Less Magical

Newer trended-data models can see whether you have been carrying high balances for many months.

That means one perfectly timed payoff can still help, but it may not fully erase a longer revolving pattern. Long-term improvement beats last-minute cleanup.

So AZEO and timing strategy are useful. They are just not a substitute for months of lower-balance behavior.

What to Do Instead

If your score dropped after you paid your cards, use this sequence:

- Find the statement closing date for every card.

- Identify the card with the highest individual utilization.

- Initiate payments a few business days before statement close.

- Keep overall utilization low.

- Avoid having any one card report extremely high usage.

- If actively optimizing, let one card report a tiny balance and pay it after statement generation to avoid interest.

When This Strategy Helps Most

This helps most when:

- Your file is otherwise fairly clean

- Utilization is the main suppressor

- You are close to a lending threshold

- The score change clearly tracks a recent statement balance

It helps less when:

- Derogatories are the bigger issue

- The file is extremely thin

- Recent inquiries or underwriting overlays are the real problem

- Trended data is reacting to months of prior revolving behavior

When to Dispute Reporting Errors

If after checking your statement dates and payment timing everything lines up but the reported balance is still wrong, you may have a legitimate reporting error. In that case, dispute the specific data point through the bureau's formal process. The CFPB's credit reporting resource center provides guidance on how to file disputes and understand your rights under the Fair Credit Reporting Act.

Conclusion

The utilization trap is usually not a punishment for paying debt. It is a reporting problem, sometimes combined with an all-zero optimization issue. Once you separate those two ideas, the fix becomes much easier: control what gets reported, not just what gets paid.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →