Student loans can help your credit, hurt it badly, or do a little of both depending on how they are reported right now. That is the key idea. Credit scoring models do not give student debt a special emotional category. They read the data: current, deferred, in forbearance, delinquent, defaulted, closed, forgiven, or transferred.

For many borrowers, student loans are the oldest installment accounts on the file. That can help with credit mix and length of credit history. But the largest scoring lever is still payment history. If the loan is paid as agreed, it can support the file over time. If it turns delinquent or defaults, the damage can be severe. For an external authority explainer, myFICO's overview is a solid starting point: How Student Loans Affect FICO Scores.

The quick answer

| Student loan status | Typical credit effect | What usually happens on the report |

|---|---|---|

| Current and paid on time | Usually positive over time | Builds installment history and supports payment history |

| Deferment or forbearance | Usually neutral to mildly indirect | Generally reported as current or no payment due; balance remains |

| Income-driven repayment (IDR) | Usually neutral to positive if current | Reported as current if paid as agreed, even when the required payment is very low or $0 under program rules |

| Forgiveness or discharge | Usually cleaner debt profile, mixed score effect | Remaining balance goes to $0; account may stay as a closed or final-status tradeline rather than disappearing immediately |

| Delinquency | Negative | Late-payment history is reported once the servicer reports it |

| Federal default | Severe negative | Default status, collections consequences, and major credit damage can follow |

| Rehabilitation after federal default | Better than staying in default | Default status is removed, but earlier late-payment history may still remain |

Student loans are installment accounts, and that matters

Student loans are typically reported as installment loans, not revolving accounts. That matters because installment accounts contribute differently to a credit file than credit cards do.

First, they can help with credit mix. FICO considers whether you have experience managing more than one kind of credit. A file with only credit cards and no installment debt may be slightly less complete than a file with both. Student loans often fill that installment role early in adult life.

Second, they can help with account age. Student loans often open years before a borrower gets serious about credit cards, auto loans, or a mortgage. That means they can become some of the oldest tradelines on the report, which helps the age-of-credit profile.

There is also a reporting nuance many people miss: one student loan relationship may appear as multiple tradelines because separate disbursements or loans are often reported separately. That is normal, especially with federal loans serviced over multiple academic periods.

This is why student loans can quietly make a file look more established, even before they produce a large score benefit. But mix and age are secondary. The most important factor is still whether the account is being reported as current.

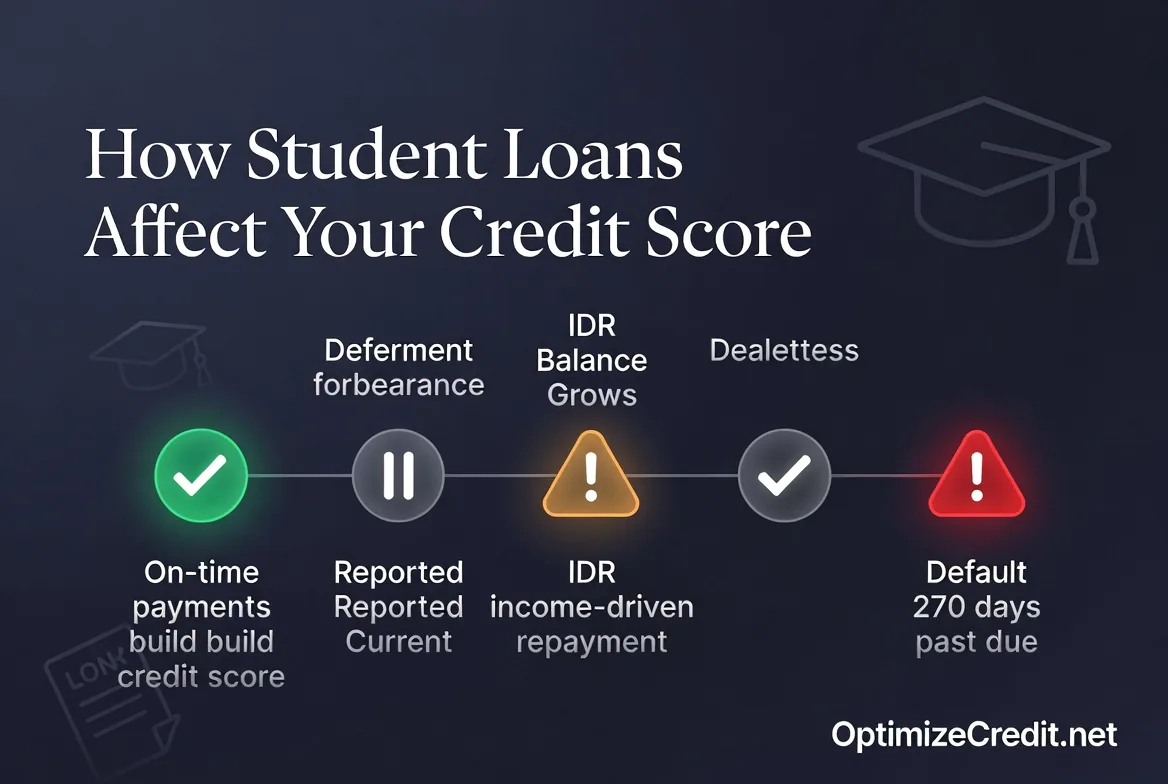

On-time payments help. Real delinquencies hurt.

This is the simplest section in the article because it follows standard credit logic.

If you make the required payment on time, student loans can help build a positive payment history over time. If you miss payments and the account is reported delinquent, the damage can be significant.

The federal and private timelines are not identical, and this is where many articles get sloppy. For federal student loans, servicer guidance says delinquencies are generally reported to the national credit bureaus at 90 days or more past due. For private student loans, lenders often follow ordinary consumer-credit reporting patterns and may report at 30 days late.

That means two things can be true at once:

- A student loan can absolutely become a serious credit problem from late payments.

- Federal student loans are not always reported to the bureaus on the same early timeline as private loans.

Once a late payment is reported, it can stay on the report for years. That is why borrowers should not confuse "I am late" with "the bureaus haven't seen it yet." The file can still move from current to delinquent fast enough to matter for a mortgage, auto loan, or rental application.

Deferment and forbearance usually protect the score, but not the balance

Deferment and forbearance are often described too loosely. They are not the same thing financially, even though they can look similar from a credit-reporting standpoint.

When properly approved, both statuses are generally reported as current or no payment due, rather than as ordinary missed payments. In practical terms, that means deferment or forbearance usually does not hurt the score the way a raw delinquency would.

But the balance side is different.

- In deferment, interest may not accrue on some subsidized federal loans, but it still accrues on many unsubsidized loans.

- In forbearance, interest generally continues to accrue.

That is the tradeoff: deferment or forbearance can protect payment history, while the balance may stay flat or grow. A borrower can finish a hardship period with a similar score but a larger loan balance.

Another nuance matters here. If the borrower was already delinquent before the deferment or forbearance was applied, that prior negative reporting may not automatically disappear. Some qualifying deferment periods can correct prior reporting in narrow cases, but retroactive cleanup is not guaranteed, and forbearance is especially weak for reversing already accurate derogatory reporting.

Income-driven repayment (IDR): credit-safe if current, but the balance may not fall quickly

Income-driven repayment plans are often misunderstood because people assume a small payment must look bad to the bureaus. That is usually not how it works.

What matters to the credit report is not whether the payment is "small." What matters is whether the payment being reported is the required payment under the plan, and whether the borrower is current under that requirement.

Under federal rules, a borrower on IDR may have a very low payment or even a required $0 payment. If that borrower is current under the plan terms, the account can still be reported as current. The repayment-plan label itself is generally not the important scoring issue.

The risk is balance behavior. Depending on the loan type, interest rules, and repayment plan design, the balance may not shrink quickly and in some cases can grow. That does not necessarily hurt the borrower the way a missed payment would, but it can keep the installment balance high for longer than expected.

So the clean summary is this:

- IDR can be good for credit stability if it prevents delinquency.

- IDR does not guarantee fast balance reduction.

- A borrower can have an account reported as current while still feeling frustrated that the principal has barely moved.

That is not a contradiction. It is a reporting-versus-balance issue.

Forgiveness and discharge: the balance goes away, but the tradeline may stay

This is one of the biggest factual mistakes in online content.

When student loans are forgiven or discharged through a program such as Public Service Loan Forgiveness (PSLF) or IDR forgiveness, the key reporting result is that the remaining balance is reduced to $0 and the account moves to a final status such as closed, paid, discharged, or forgiven.

What does not always happen is instant disappearance from the credit report.

Federal servicer guidance says paid, transferred, consolidated, and forgiven education loans can remain on the credit report for years as historical tradelines. So the best wording is not "forgiveness erases the account." The better wording is: forgiveness resolves the balance, and the tradeline may remain as closed historical data.

Score impact can vary.

If the loan was a large active installment balance, reducing it to zero may help the debt profile. But if the borrower loses one of the few active installment accounts on the file, there can sometimes be a small temporary scoring adjustment. That is usually a structural scoring shift, not a penalty for receiving forgiveness.

Default is where student loans become a major credit problem

For federal student loans, default generally happens after 270 days of missed scheduled payments. That is the bright-line rule borrowers need to know.

Default is much worse than ordinary delinquency because it can trigger multiple layers of trouble at the same time:

- severe negative credit reporting,

- transfer into collections channels,

- administrative wage garnishment,

- federal tax refund offset,

- and other collection consequences.

This is why default is not just "a worse late payment." It is a different stage of the problem, with much harsher credit and collection consequences.

For credit purposes, default is the scenario borrowers should avoid at almost all costs. A temporary deferment, a workable IDR plan, or direct communication with the servicer is almost always better than letting the account roll into default.

Rehabilitation: one of the few real cleanup tools after default

Federal loan rehabilitation is important because it is one of the few mechanisms that does more than simply mark the account as paid.

For Direct Loans and FFEL Program loans, rehabilitation generally requires nine on-time, voluntary payments within 10 consecutive months. After successful rehabilitation, the default status is removed and collections stop.

That is a meaningful credit repair outcome in the literal sense of the word repair. But it is not a total rewind.

The part many borrowers miss is this: rehabilitation removes the default status, but the earlier late-payment history that led up to default may still remain. So rehabilitation can make the file much better without turning it into a perfectly clean file overnight.

The best way to think about rehabilitation is:

- it is a major step up from staying in default,

- it can materially improve how the file looks to future lenders,

- but it does not erase every piece of negative history connected to the loan.

Student loans also affect mortgage DTI

Student loans affect more than just your credit score. They also affect debt-to-income ratio (DTI) for mortgage underwriting.

DTI is not part of your credit score. It is a separate mortgage-qualification metric: monthly debt obligations divided by gross monthly income.

This matters because a borrower can have a decent score and still run into trouble if the student-loan payment used for underwriting pushes DTI too high.

Agency rules vary, but the big picture is consistent: lenders usually cannot ignore student loans just because the current payment is low, deferred, or shown as $0 on the credit report.

For example, current Fannie Mae guidance says:

- if the credit report shows a student loan payment, the lender can generally use that amount;

- if the credit report shows $0 or no payment, the lender must determine a qualifying payment using the agency's allowed methods;

- if the borrower is on an income-driven plan and documentation shows the actual payment is $0, Fannie Mae allows qualification using $0;

- for deferred loans or loans in forbearance, Fannie Mae allows either 1% of the outstanding balance or a fully amortizing payment using documented repayment terms.

That is why student loans can feel "fine" from a credit-score perspective and still create a mortgage bottleneck. Credit score answers the question, "How have you handled credit?" DTI answers the question, "Can you afford the new payment with your existing obligations?"

The practical takeaway

Student loans are not automatically good or bad for your credit. They are highly status-dependent.

They help when they add installment depth and are paid as agreed. They are often neutral when they sit in approved deferment or forbearance, although the balance can still grow. They can remain credit-stable under IDR if the borrower stays current under the plan. They become very harmful when delinquency becomes default. And they improve meaningfully after rehabilitation, even though old late marks may still remain.

The most accurate way to think about student loans is not as one account type with one effect, but as a long-running tradeline whose impact changes as the reporting status changes. If something on your report looks wrong or your score is not reflecting what you expect, the credit score debugging guide can help you trace the actual suppressor. And if you are close to a goal but stuck, the last-mile problem breakdown covers why the final points are often the hardest. For more troubleshooting topics, visit the troubleshooting hub.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →