Quick answer

If you use a personal loan, balance transfer, debt management plan, or home equity product to lower revolving credit card utilization and keep payments current, your score often improves after the new balances report. If you add new debt, miss payments, close useful card limits, or use a debt-settlement company that tells you to stop paying, your score can get worse instead.

Why debt consolidation affects credit at all

Your credit score does not care that your monthly life feels simpler. It reacts to the information reported on your credit file.

That means debt consolidation changes your score only through a handful of mechanisms:

- a new account appears

- a hard inquiry may appear

- revolving balances may drop

- available revolving credit may stay open or disappear

- installment debt may increase

- payment history may improve or deteriorate depending on execution

The most important distinction is revolving debt versus installment debt.

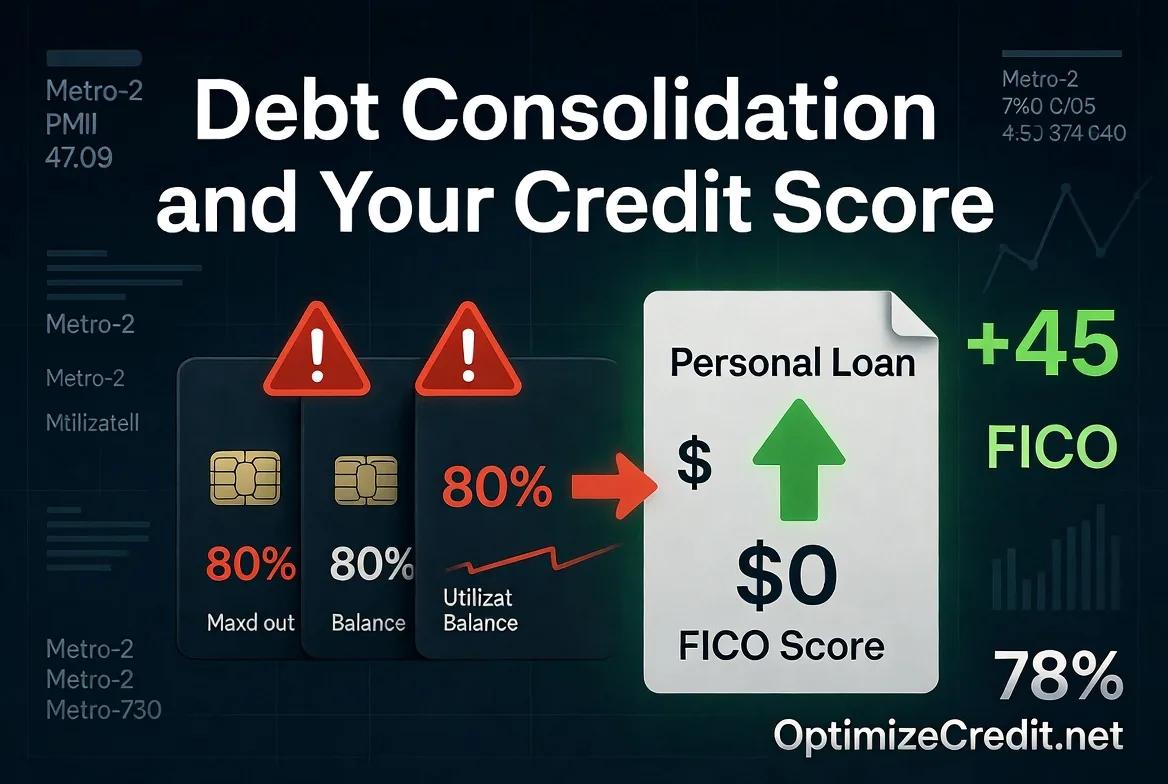

Credit cards are revolving debt. Personal loans, home equity loans, auto loans, and mortgages are installment debt. In FICO scoring, revolving utilization tends to matter much more than installment balance-to-loan ratio. That is why consolidating maxed-out cards into a personal loan can help even though total debt did not magically vanish.

The four main types of debt consolidation

1) Personal loan

This is the most common consolidation structure. You borrow a fixed amount and use the proceeds to pay off several credit cards.

What usually helps

- credit card balances can drop to $0

- aggregate revolving utilization can collapse

- per-card utilization can also collapse

- you may improve credit mix if you previously had only revolving accounts

What can hurt at first

- one or more hard inquiries

- a brand-new account lowers average age of accounts

- the new installment loan often reports near 100% of original balance at first

The reason this option often works best for scores is simple: it can move debt out of the most heavily scrutinized utilization bucket. That does not guarantee a score increase, but it often creates the cleanest scoring setup when the cards are actually paid down and left alone.

2) Balance transfer card

A balance transfer is still consolidation, but it keeps the debt inside the revolving category.

This matters because the scoring effect depends on where the transferred debt lands.

Best case

You open a new card with a large enough limit that your overall utilization and the utilization on the transfer card both end up materially lower than before.

Weaker case

You transfer balances onto a card that ends up nearly maxed out. Your aggregate utilization may improve, but the individual card can still report very high utilization, which many scoring models dislike.

So a balance transfer can help, especially if it creates more total available limit and lowers interest expense, but it is usually less structurally clean than moving the debt into an installment loan.

3) Debt management plan (DMP)

A debt management plan is typically arranged through a nonprofit credit counseling agency. You make one consolidated payment, and the agency distributes it to participating creditors.

What people often misunderstand

A DMP is not debt settlement.

A legitimate DMP is usually built around repaying debt on agreed terms, often with reduced interest rates or adjusted payment structures. FICO does not directly punish a DMP notation by itself, but creditors may close or freeze participating cards, and future manual underwriters may notice the notation as a sign of recent financial stress.

Why the score impact can be mixed

- on-time payments can stabilize the file

- balances can decline over time

- but closed cards can reduce available revolving credit

- and reduced available credit can make utilization math less favorable

That is why a DMP can be financially smart while still being neutral or mildly negative for scores in the early phase.

4) Home equity loan or HELOC

This is debt consolidation using your house as collateral.

A home equity loan is installment debt. A HELOC is a line of credit secured by your home. Either one may lower your card balances and help utilization, but the tradeoff is serious: you are converting unsecured debt into debt tied to your home.

That means the scoring mechanics may improve while the financial risk gets worse. If you default, the consequences are far more severe than defaulting on an unsecured personal loan.

The math: three cards at 80% consolidated into one loan

Here is the clean example most people need to see.

Before consolidation

| Account | Limit | Balance | Utilization |

|---|---|---|---|

| Card A | $5,000 | $4,000 | 80% |

| Card B | $5,000 | $4,000 | 80% |

| Card C | $5,000 | $4,000 | 80% |

- Total revolving limit: $15,000

- Total revolving balance: $12,000

- Aggregate revolving utilization: 80%

That is a stressed revolving profile.

After a $12,000 personal loan pays all three cards to $0

| Account | Limit / Original Amount | Balance | Utilization Type |

|---|---|---|---|

| Card A | $5,000 | $0 | 0% revolving |

| Card B | $5,000 | $0 | 0% revolving |

| Card C | $5,000 | $0 | 0% revolving |

| Personal loan | $12,000 | $12,000 | 100% installment balance-to-loan |

The total debt still exists, but the revolving utilization penalty is removed. That is the core reason consolidation can help scores.

The improvement is often not visible on day one. The new loan may report first, while the cards still show old balances until the next reporting cycle. That temporary mismatch is why some people see a short dip before a later rebound.

Why personal-loan consolidation often helps more than people expect

The scoring system generally treats high credit card utilization as a stronger risk signal than a fresh installment loan with a fixed payoff schedule.

That means this sequence is common:

- the inquiry and new account cause a small short-term drag

- the old cards later report lower balances

- the utilization improvement outweighs the early drag

- the file continues to improve if payments stay on time

This is also why people checking too early sometimes think consolidation "did not work." Often the score has not failed. The reporting cycle just has not caught up yet.

Do not close the zero-balance cards

This is one of the biggest mistakes after successful consolidation.

If you pay off cards and then close them, you remove available revolving credit from the denominator of your utilization equation.

Using the example above:

- keep all three cards open and a later $1,500 balance equals 10% utilization across $15,000 of limits

- close two cards and that same $1,500 on the last card equals 30% utilization across only $5,000 of limits

Same spending. Very different scoring result.

Keeping paid-off cards open usually preserves both utilization capacity and account age benefits. The behavioral exception is obvious: if an open card creates a high relapse risk, the household-budget problem may outweigh the scoring advantage. But from a pure scoring standpoint, closing zero-balance cards is usually a bad trade.

When consolidation hurts your score instead

You run the cards back up

This is the most common failure mode. You now have the installment loan and new revolving balances. The score can fall back because the utilization problem returns while total debt service gets worse.

This is closely related to The Utilization Trap.

You pick the wrong balance-transfer setup

A balance transfer is not automatically good for scores. If the destination card reports near its limit, the file may still look stressed even if you saved on interest.

Your DMP closes too much revolving capacity

A DMP can improve payment behavior and reduce rates, but if it removes most of your available credit lines, the utilization profile may stay tighter than expected.

You consolidate with home equity but add serious financial risk

The score may improve while your downside risk gets worse. Lower rate does not always mean better strategy if the debt is now secured by your house.

You use debt settlement instead of consolidation

This is where many consumers get burned.

Some debt-settlement companies tell you to stop paying creditors and instead build up money for later negotiations. That can trigger late payments, charge-offs, collections, lawsuits, and long-lasting credit damage. It is not the same thing as ordinary consolidation.

Debt settlement warning: what actually happens

Consolidation

- creditors are typically paid in full or under current agreed terms

- accounts may remain current

- the main score variables are utilization, inquiries, and new accounts

Settlement

- consumers are often told to stop paying first

- late marks begin to stack up

- accounts may charge off

- collections may appear

- the final account may report as settled for less than full balance

That is why settlement can damage a file much more severely than a personal loan, balance transfer, or DMP.

For consumer guidance on debt-relief programs and the risks of stopping payments, see the CFPB's explainer at consumerfinance.gov.

How long it usually takes to see score movement

There is no universal timeline, but the usual sequence looks like this:

- Immediately to 30 days: inquiry and new-account effects may show first

- Next card reporting cycle: paid-off or reduced card balances begin reporting

- 30 to 60 days after payoff: many files start reflecting the utilization improvement

- 3 to 6 months: the new account ages a bit and the file stabilizes

- Longer term: ongoing on-time payments matter more than the initial event

The key operational detail is that consolidation works on bureau reporting cycles, not on the day money moves.

Bottom line

Debt consolidation can be a genuine scoring improvement strategy, but only when the structure is right.

A personal loan often helps the most because it can remove debt from revolving utilization. A balance transfer can help, but only if the new card does not end up maxed out. A DMP can be financially smart, yet mixed for early scoring because cards may be closed. A home equity product may improve utilization while exposing your house to risk.

The biggest mistake is believing consolidation solved the problem by itself. It only changes the scoreboard. The real win comes when the cards stay low, payments stay current, and the new structure is used as a payoff path rather than a temporary reset.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →