TL;DR: Authorized user tradelines usually report within one billing cycle, but the exact timing depends on three different dates: the statement closing date, when the card issuer reports to the credit bureaus, and when credit monitoring apps update. Many major credit card companies report within a few days after the statement closes, while some issuers report with a one-month delay. Understanding this timing can make a big difference if you need fast results for things like auto loans or apartment applications.

Why reporting timing matters so much

For many people, timing is everything. If you are preparing for an auto loan, a rental application, or your first major credit decision as a new immigrant, even a small delay can change the outcome. This is especially common for immigrants who may have income but limited U.S. credit history and need fast improvements to qualify.

Authorized user tradelines are popular because they can work quickly, but only if you understand how reporting actually works.

The three dates that control tradeline reporting

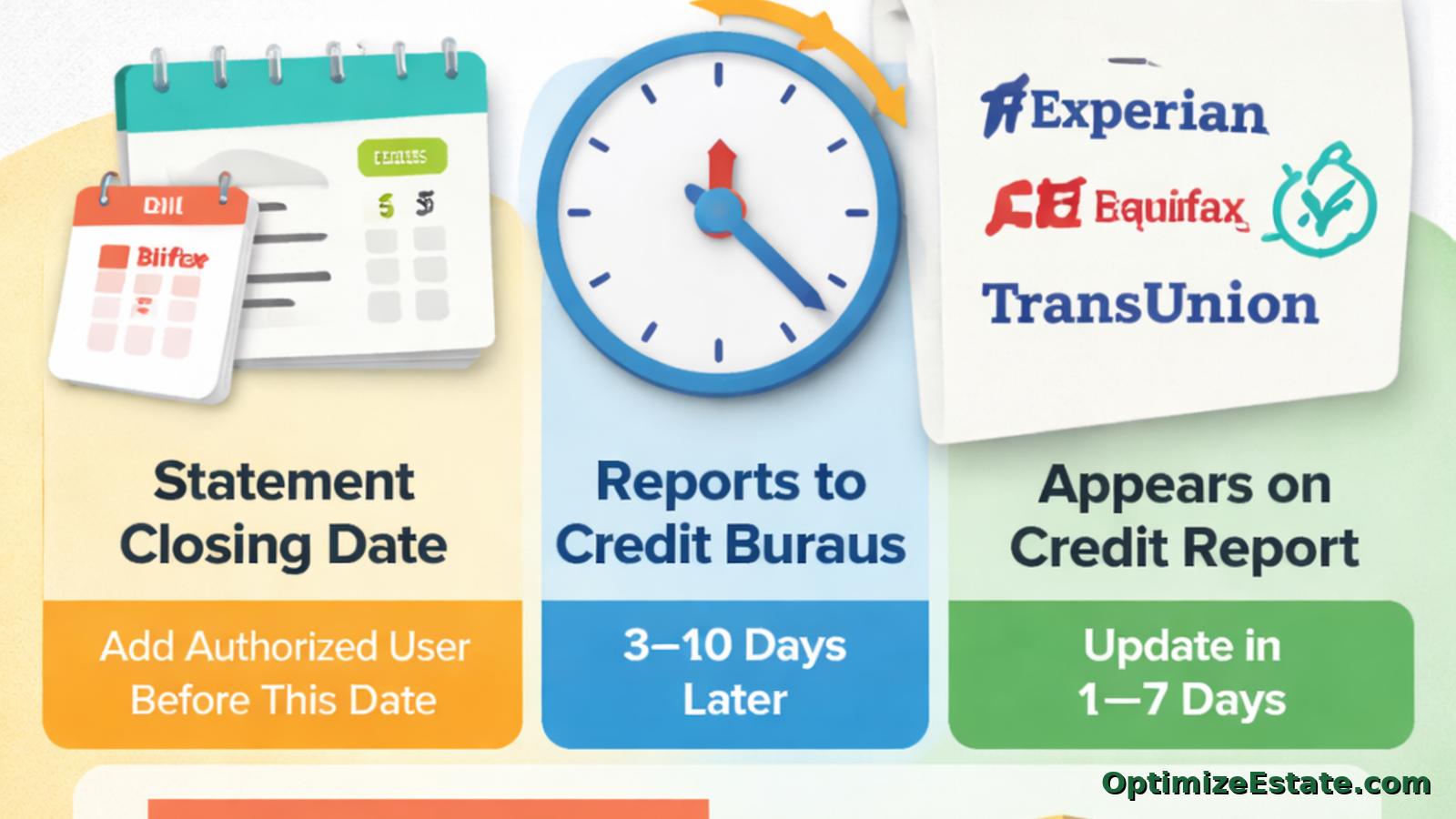

Most people think tradelines "just show up." In reality, there are three different steps, each with its own timing:

- Statement closing date: This is the date your credit card statement closes each month. Most card issuers only consider authorized users who are added before this date.

- Reporting date to the credit bureaus: After the statement closes, the card issuer sends updated account data to Experian, Equifax, and TransUnion. For many issuers, this happens about 3 to 5 days after the statement closing. Experian confirms that most major issuers report AU accounts to all three bureaus.

- Credit monitoring update delay: Even after the bureaus receive the data, credit monitoring sites may take extra time to show it, depending on whether you have a paid subscription or are using free access.

Typical reporting timelines by issuer

Most major credit card companies follow a predictable pattern. While some report nearly immediately, others require a full cycle to process an authorized user.

| Card Issuer | Reporting Speed | Expected Update Window |

|---|---|---|

| Chase / Amex | Fast | Within a few days after statement closes |

| Citi / Bank of America | Delayed | Typically requires one full statement cycle (approx. 30 days) |

| Capital One / Wells Fargo | Standard | 3 to 7 days after statement close |

With Citi, the authorized user account usually does not report until the next statement cycle. For example, if a statement closes on March 6 and the user is added before then, the report typically will not hit the bureaus until April 6. This creates a one-month delay that is crucial for those in a rush.

Why you may see different dates on Credit Karma or Experian

Even after the card issuer reports to the credit bureaus, you might not see the update right away. Updates often appear within 1 day on paid services like Experian.com, whereas free monitoring apps typically lag by 3 to 5 days.

Example Timeline:

- Statement closes: 6th

- Issuer reports to bureaus: 10th to 11th

- Paid monitoring shows update: 12th to 13th

- Free monitoring (e.g. Credit Karma) shows update: 15th to 16th

How to get the fastest possible results

If timing is critical, planning around the statement closing date matters. In many cases, if a tradeline closes on the 6th and you are added on the 1st or 2nd, reporting can happen within a week. This is one of the fastest ways to see movement before applying for an auto loan, refinancing, or leasing an apartment.

Who benefits most from fast tradeline reporting

Tradelines tend to help the most for people in these situations:

- People preparing for auto loans

- New immigrants building U.S. credit

- Young adults with thin credit profiles

- Borrowers with high utilization and low limits

- Anyone facing a time-sensitive application

Tradelines That Actually Report

We focus on what actually moves credit scores: utilization, account age, and clean reporting. With 500+ successful placements and excellent reviews on TrustPilot ★★★★★, every tradeline is screened for reporting consistency before it is listed.