Show your clients the real cost of 20 FICO points

When a client asks "Does my credit score really matter that much?" this is the article you send them. While 20 FICO points may seem minor to a client, in the world of mortgage pricing they can represent the difference between a standard tier and a high-cost tier — or between approval and denial. Mortgage pricing is non-linear and often moves through Loan-Level Price Adjustments (LLPAs) that trigger at thresholds such as 680, 700, and 740. A small score move that crosses one of those lines can reduce your client's monthly payment, lower DTI pressure, and save them tens of thousands of dollars over a 30-year loan.

More importantly for you: this is the math that justifies your action plan, keeps deals alive, and turns borderline clients into closings.

What is an LLPA and how does it affect your client's rate?

LLPA stands for Loan-Level Price Adjustment. In plain language, it is part of the risk-based pricing logic used in conventional mortgage execution. A lender or investor charges more when a client's file is viewed as riskier based on score, LTV, occupancy, or other factors. You can review the current adjustment matrix directly from Fannie Mae's LLPA matrix.

Your clients do not always see LLPAs as a separate line item. They feel them through:

- A higher interest rate

- An upfront fee or discount-point style pricing hit at closing

- Higher cash-to-close requirements

- Pricing differences that seem disproportionate to a "small" score gap

When a client says "Why is my rate higher than my neighbor's?" — LLPAs are usually part of the answer. Understanding this lets you explain the problem and present a solution.

Why 620, 680, 700, and 740 are the thresholds that make or break deals

These numbers matter because real client conversations often become threshold conversations.

- Client near 620 — the issue is usually access or product eligibility. Below this line, the deal may not exist at all.

- Client near 680 — the issue can include PMI and broader pricing pressure. Moving above this saves the client real monthly dollars.

- Client near 700 — the client may still be paying noticeably more than a stronger file. This is where small moves yield outsized savings.

- Client near 740 — many clients are trying to reach a classic top pricing tier. Getting them here is the difference between good and excellent terms.

While 740 remains the classic benchmark in many conventional conversations, some lender overlays or product-specific pricing grids reward even higher scores. Verify the actual pricing matrix in play for each client rather than assuming every 740 file is treated identically.

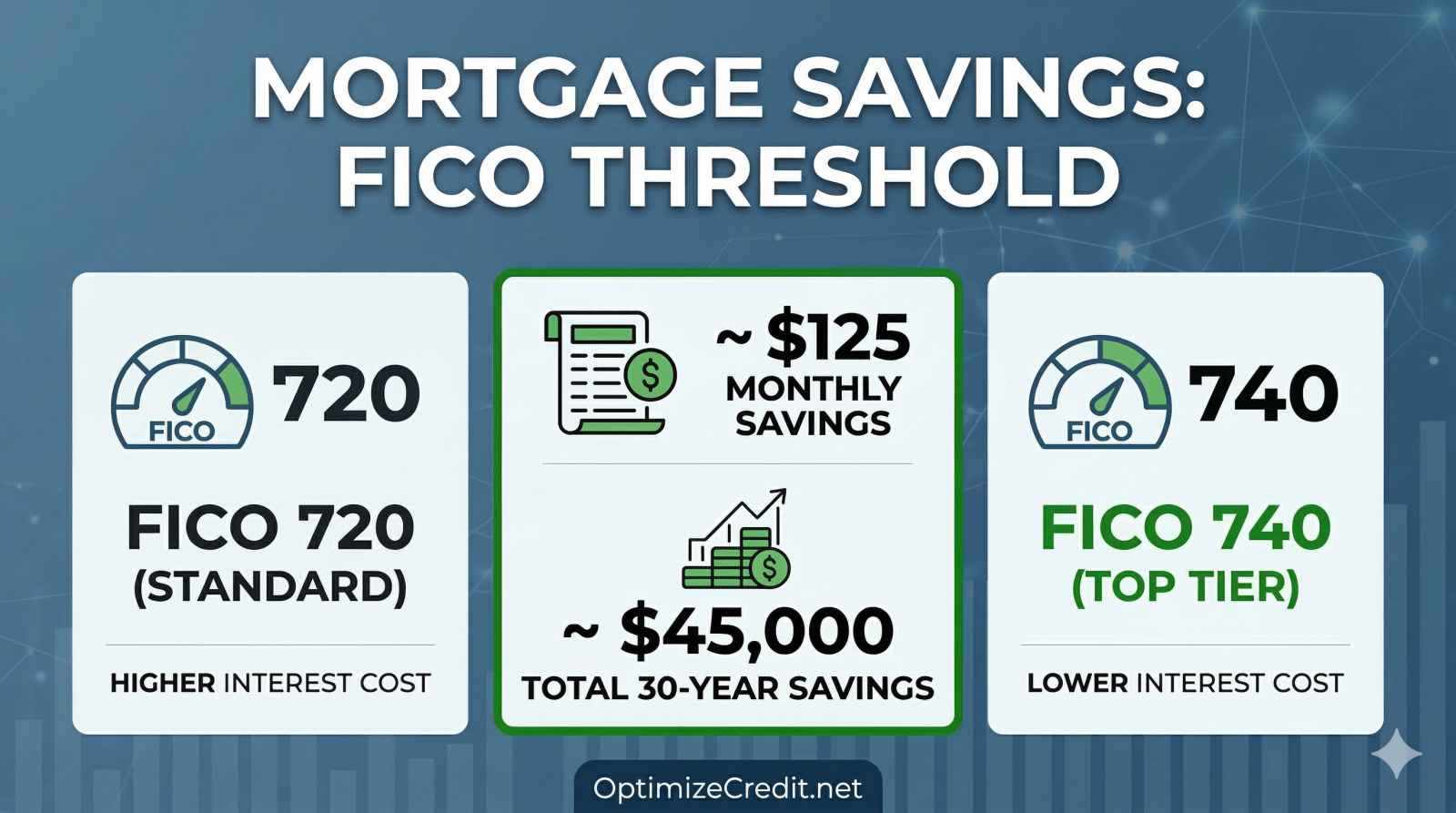

The math your clients need to see: what a 0.375% rate difference really costs

Assume a 30-year fixed conventional loan. These numbers isolate principal and interest only so the rate impact is clear.

Example: $500,000 loan

- 6.875% monthly principal and interest: about $3,285

- 6.500% monthly principal and interest: about $3,160

- Monthly savings for your client: about $125

- 10-year savings: about $15,000

- 30-year savings: about $45,000

When you put this in front of a client who is hesitating on your action plan, the conversation changes. "Only 20 points" becomes "$45,000 over the life of your loan."

Rate gap across different loan sizes — the table that closes deals

Use this table with clients. Same 0.375% rate gap on a 30-year fixed loan:

| Client's Loan Amount | Higher Rate Payment | Lower Rate Payment | Monthly Savings | 30-Year Savings |

|---|---|---|---|---|

| $300,000 | $1,971 | $1,896 | $75 | $27,000 |

| $400,000 | $2,628 | $2,528 | $100 | $36,000 |

| $500,000 | $3,285 | $3,160 | $125 | $45,000 |

The exact figures will vary by lender and lock date, but the directional message is stable: a moderate pricing difference becomes large over time. This is the math that motivates clients to follow through on your recommendations.

Why 20 points can save the deal, not just save your client money

For a borderline DTI client, a better rate does more than lower total interest — it can keep the loan approvable.

Higher rates increase the monthly housing payment. Higher payments raise DTI. For some clients, that means 20 points are not just about cost — they are about staying under a critical qualification line. Lose those 20 points and the deal dies.

This is where your expertise matters most. When you identify a tactical lever that can move the client's score before the rate lock expires, you are not just advising — you are saving the deal and earning a commission that would otherwise walk out the door.

Generic score advice versus professional deal-closing advice

Generic advice says "A better score is always good." Professional advice says "A better score matters most when it moves your client across a threshold or reduces risk-based price hits."

That framing answers the real client question: not "Is a 720 better than a 700?" but "What does the 20-point difference actually do to my payment?" When you can answer that with specific numbers, clients trust you — and they refer you.

What the underwriter actually cares about in your client's file

A lender is not only watching the client's score. They are watching the file behind it. Help your clients understand:

- A large payoff can improve utilization but may require clear sourcing documentation.

- A rushed new account can damage age and inquiry profile even if it improves available credit.

- A balance transfer can improve one card but leave another ratio looking worse.

That is why the tactical execution covered in the last-mile problem article matters. The score move has to be both real and operationally clean — or the underwriter will flag it and the deal stalls.

Should your client wait three months to gain 20 points?

Not always — and this is where you earn your keep as a professional.

A client may be correct that waiting could improve the score. But if market rates rise by 0.50% while they wait, the better score may not offset the worse rate environment. The deal you could have closed today becomes harder tomorrow.

Frame this as a trade-off with your client:

- What is the cost of waiting versus acting now?

- What is the probability of improvement in the available timeline?

- Does the file have tactical levers or only structural ones?

If the client's file has tactical levers — utilization cleanup, a correctable reporting error, or strategic timing — the improvement may happen in weeks rather than months. The optimizer can identify which levers are available so you and your client can make a data-driven decision instead of guessing.

What drives score movement when your client needs it fast

If the client's main suppressor is revolving utilization or thin revolving depth rather than derogatory history, an authorized user tradeline can improve the denominator quickly without a new hard inquiry. In the right file, that can be enough to cross a pricing threshold or reduce LLPA pressure — turning a borderline deal into a closed deal.

In other client files, the fastest lever may be utilization cleanup, dispute resolution, or strategic timing — the optimizer identifies which. A client with a reporting error dragging one bureau below the threshold may benefit most from an FCRA dispute. A client with high balances and plenty of limits may just need to pay down before the next statement close date.

The right answer depends on the client's file, not on a default recommendation. Your value as a professional is matching the right lever to the actual file characteristics and timeline.

This article owns the math — the hub owns the advisory framework

Not every client should optimize the same way. That is why the professional strategy hub owns the recommendation logic and the five-question intake framework.

This article gives you the math to show clients why the score move matters economically. The hub gives you the decision framework for whether that score move is realistically attainable for a specific client without damaging the file.

Together, they give you everything you need to advise clients with confidence, close more deals, and build a reputation as the professional who actually understands credit.

The bottom line: rate math is your best closing tool

A 20-point move can be small in conversation and worth $45,000 to your client.

When a client's score crosses a threshold, they get:

- A better rate

- Lower monthly payment

- Lower total borrowing cost

- Reduced DTI pressure

- Better odds of a smoother approval

And you get a closed deal, a satisfied client, and a referral source that keeps producing. That is why mortgage rate math is not just a credit topic — it is a business development tool for every lending professional.

Important calculation note

These examples assume a fixed-rate conventional mortgage and isolate principal and interest only. They do not include taxes, insurance, PMI, HOA dues, or lender fees. Actual payment and total-cost outcomes vary by market, lender, product, and timing.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →