The trust rule: explain the system before you explain the number

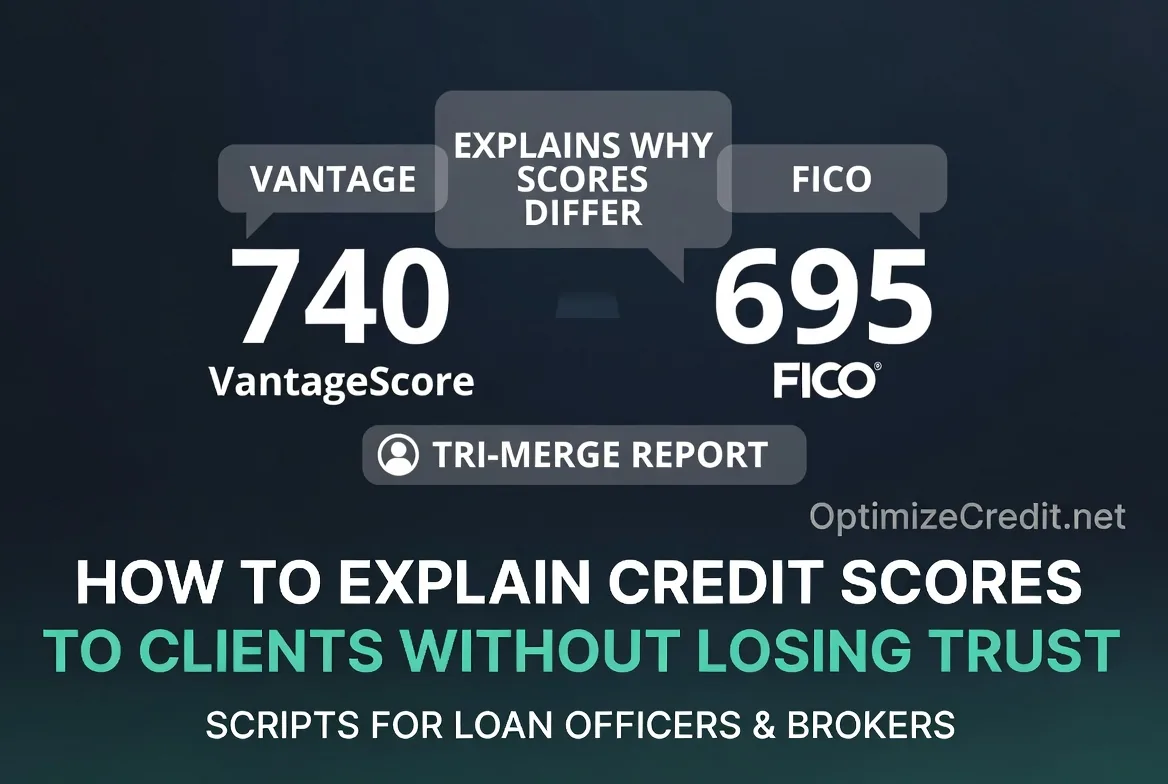

A client logs into Credit Karma, sees a 740, and walks into your office expecting prime pricing. You pull credit and the file comes back 695. If you handle that badly, the client hears "bait and switch." If you handle it well, the client hears "this person actually understands underwriting."

The difference is not charisma. It is framing.

Credit Karma says it provides VantageScore 3.0 scores from Equifax and TransUnion, while the CFPB explains that lenders may use different scoring models for different loans and that score differences can materially change the credit offers a consumer expects. In mortgage, the current Enterprise landscape is more nuanced than many professionals still realize: FHFA says lenders may use Classic FICO or VantageScore 4.0 via tri-merge for loans sold to the GSEs, while FICO 10T remains approved for future use. That means the safe professional move is not to memorize one score label — it is to explain which score family, bureau set, and workflow the transaction actually uses.

The biggest mistake professionals make is explaining the mismatch after the lender pull. At that point, the explanation sounds defensive.

Do it at intake instead.

Intake script

"Before we talk strategy, I want to separate the score you may see in a consumer app from the score set that may drive this transaction. Consumer apps often show a VantageScore from one or two bureaus. A lender may use a different model, a different bureau set, and a different pull date. So if your number and our number differ, that does not automatically mean either one is wrong."

That script works because it validates the client's score without surrendering control of the underwriting conversation.

Why scores differ: the three variables clients need to understand

There are three main reasons the number on the phone and the number in underwriting may not match:

| Variable | What changes | Why the client gets confused |

|---|---|---|

| Bureau | Equifax, Experian, and TransUnion may not have identical tradeline data | The client assumes all bureaus hold the same file |

| Model/version | VantageScore, Classic FICO, FICO Auto, and other versions weigh risk differently | The client assumes "a credit score is a credit score" |

| Timing | Scores change when report data changes, and different data may be present on different days | The client assumes paying today means scoring today |

That framework is the cleanest way to explain the mismatch without sounding evasive. Creditors do not always report to all three bureaus, and lenders use different models for different loan types. Understanding the difference between scoring systems is essential — for a deeper comparison, see FICO vs. VantageScore.

Script: "Your scores are different because…"

This is the line most professionals need to be able to say smoothly and repeatedly.

Short script

"Your scores are different because the bureau, the scoring model, and the timing can all be different at the same time. Your app may be showing a VantageScore 3.0 from Equifax and TransUnion, while the lender may be using a different score model or version and a different bureau set. That does not make either score fake. It means they are different measurements built from different inputs."

If the client needs a more visual explanation, use this:

Analogy script

"Think of your credit report as the raw ingredients and the score model as the recipe. Change the ingredients a little, or change the recipe, and the final number changes."

That is better than saying "Credit Karma is wrong," because it preserves trust instead of provoking a fight.

Script: "Your score dropped because…"

The score did not move "for no reason." It moved because either the file changed or the model changed.

The most common causes are:

- a higher reported revolving balance

- a new account

- a hard inquiry

- a closed card or reduced limit that raised utilization

- a different score model or bureau than the one the client checked

FICO explains that inquiries can affect scores, and myFICO says hard inquiries remain on reports for up to two years but generally affect FICO Scores for only 12 months. CFPB guidance also makes clear that utilization and available credit matter.

Short script

"Your score dropped because something in the file changed, and the model recalculated from the new file. The most common triggers are a higher reported card balance, a new account, a hard inquiry, or a lower amount of available credit. The next step is not guessing. It is comparing the current report to the prior one line by line."

Utilization script

"The payment may have posted, but if the card reported a higher statement balance first, the score can still drop until the next reporting cycle updates the file."

This is where calm beats certainty. Do not pretend you know the exact point impact before you isolate the changed tradeline(s).

Script: "You need to wait because…"

Timing is the easiest part of credit to explain badly. Clients hear "wait" as "you were wrong."

The fix is to explain the reporting chain:

- the consumer makes a payment

- the creditor updates its own ledger

- the creditor reports to the bureau, usually on a monthly cycle

- the bureau file refreshes

- the score recalculates from the refreshed file

Experian says creditors typically report monthly, often tied to the billing cycle, and scores reflect the information on file at the time of the pull.

Short script

"You need to wait because paying the balance and having the lower balance appear in the bureau file are not the same event. The lender can only react to the file that has actually been reported."

Better script

"Your cash movement happened today. Your bureau movement may happen later. Underwriting reacts to the bureau file, not the payment receipt."

That one line saves a surprising amount of trust.

When waiting is enough — and when rapid rescore is the right escalation

This is where many articles either under-explain or overpromise.

A rapid rescore is not a magic score boost. It is an expedited update process that a lender may use to get recent, documented changes reflected in the credit file faster. Experian, Equifax, and Capital One all describe it as lender-driven or lender-facilitated, generally used in mortgage contexts, and typically completed in a few business days. Consumers generally cannot order it directly on their own, and it does not guarantee a higher score or loan approval.

| Situation | Best professional guidance |

|---|---|

| Balance was just paid down and closing is not urgent | Wait for normal reporting |

| Balance was just paid down and closing is time-sensitive | Consider lender-initiated rapid rescore |

| Client wants accurate negative data removed "fast" | Do not promise rapid rescore as a fix |

| Client is near a threshold for eligibility or pricing | Model the benefit, document the change, then decide whether rapid rescore is worth it |

Rapid rescore script

"If timing is the only problem, there may be a lender-initiated rapid rescore option. It does not create a better score by itself. It only accelerates documented changes that are real and already supported by new information."

That is a far safer script than "we can force the bureaus to update your score in three days."

For the process details, the most relevant internal companion is the rapid rescore guide.

Loan eligibility: do not let clients think score equals approval

This is one of the most important trust-protection points in the entire article.

A stronger score can improve pricing and improve a file's approval odds, but a score is not a loan approval. Lenders also look at debt-to-income ratio, income, assets or reserves, loan type, program overlays, and overall ability to repay. CFPB says DTI is one way lenders measure repayment ability, and its auto-lending guidance notes that rate and approval decisions can reflect not just score, but credit history, income, debt, and down payment. Even excellent credit does not guarantee approval if other underwriting factors fail.

Eligibility script

"This score matters, but it is not the whole decision. A stronger score may improve the file, but approval and pricing also depend on debt, income, reserves, and the lender's underwriting rules."

That sentence prevents a lot of later resentment.

Compliance: how to stay useful without drifting into CROA territory

The FTC says CROA prohibits misleading claims in the offering or sale of credit repair services, bars advance payment by covered companies, and requires specific disclosures. It also warns that credit repair companies cannot legally promise to remove accurate and timely negative information.

That means non-CRO professionals should stay in an education-and-underwriting lane.

Safer language

Use:

- "Here is how the lender is likely to read this file."

- "Here is what changed."

- "Here is the timing issue."

- "Here is what may improve the file once updated."

Avoid:

- "I can fix your credit."

- "This will raise your score by 30 points."

- "You will qualify if you do this."

- "We can remove that negative."

Compliant script

"I can explain what the current file is showing, what factors may be suppressing the score, and what timing or reporting changes may affect the underwriting result. I cannot guarantee a score outcome or sell this as credit repair."

That is still useful. It is just clean.

The operational playbook professionals should use

If you want fewer trust breaks, standardize the conversation.

- At intake, separate app scores from underwriting scores.

- Before strategy, state which score family and bureau set matter for the transaction.

- When a score drops, compare the old and new file instead of speculating.

- When timing is the issue, explain reporting cycles clearly.

- When the client is near a threshold, evaluate whether waiting or rapid rescore is the correct tool.

- Never promise points or approval. Explain mechanism, not certainty.

That is the difference between sounding like a salesperson and sounding like the adult in the room.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →