The core definition: what DTI actually is

A borrower can spend six months lifting a mortgage score from the mid-600s into the low 700s and still get stopped cold by underwriting. That is not a contradiction. It is how mortgage risk is actually measured.

Credit score and debt-to-income ratio are not competing systems. They are complementary systems. The score tells the lender how the borrower has handled credit historically. DTI tells the lender how stretched the borrower will be going forward once the new housing payment is added. A high score can help a file survive higher DTI. A weak score can make the same DTI feel unacceptable. But neither one replaces the other.

That is why brokers, loan officers, and financially literate borrowers should stop treating DTI as an afterthought. In many near-miss files, DTI is not just "the other metric." It is the actual reason the loan does or does not work.

For the cleanest consumer-facing definition, the CFPB still gives the best starting point: What is a debt-to-income ratio?

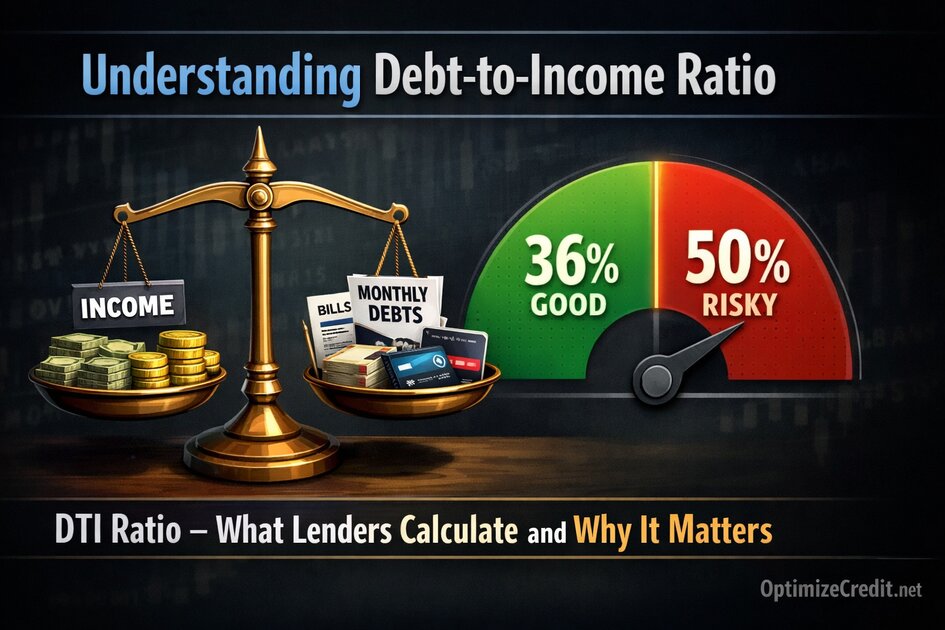

DTI is simple in formula and complicated in execution.

Debt-to-income ratio = total monthly debt obligations ÷ gross monthly income

If a borrower has $2,800 in counted monthly obligations and $7,000 in gross monthly income, the back-end DTI is 40%.

The reason professionals get tripped up is not the formula itself. It is the inputs:

- which debts count

- which debts do not count

- which student-loan payment must be used

- whether manual underwriting or AUS rules apply

- whether the borrower's credit profile supports a higher ratio

That is why DTI should be explained with the same care as score version, bureau data, and reporting lag.

Front-end vs. back-end DTI

Most people say "DTI" when they mean the total ratio, but underwriters often look at two separate numbers.

Front-end DTI

Front-end DTI is the housing ratio.

It generally uses the proposed monthly housing payment divided by gross monthly income. In mortgage practice that housing payment typically includes PITIA:

- principal

- interest

- taxes

- insurance

- association dues where applicable

This ratio answers one narrow question: how much of the borrower's income will be consumed by the house payment itself?

Back-end DTI

Back-end DTI is the total debt ratio.

It uses the proposed housing payment plus other counted monthly debts:

- minimum credit card payments

- student loans

- auto loans

- installment loans

- child support or alimony

- leases

- other recurring obligations that must be counted under program rules

This is usually the ratio that matters most in real underwriting.

Conventional DTI: what 28/36 means today

The old 28/36 rule is still useful as a teaching tool. Fannie Mae's consumer glossary still defines it as a guideline suggesting:

- maximum housing ratio of 28%

- maximum total DTI of 36%

That is still a good mental benchmark. But it is not the whole current conventional story.

Under Fannie Mae's Selling Guide:

- manual underwriting starts with a maximum total DTI of 36%

- that manual cap can stretch to 45% if the borrower satisfies the applicable credit-score and reserve requirements in the Eligibility Matrix

- DU loan casefiles can go up to 50% total DTI

So the accurate professional explanation is:

28/36 is the traditional conventional affordability rule of thumb. Real modern conventional underwriting can go higher, but the path depends on whether the file is manual or AUS and whether the borrower has the score, reserves, and overall profile to support the stretch.

That is a much safer statement than saying "conventional is 43%" as if that is a universal hard cap.

FHA DTI: more flexible, but not a free pass

FHA is often described as "more forgiving," and that is usually directionally correct. But the better explanation is that FHA has a more explicit compensating-factor framework.

For manual underwriting, HUD's handbook uses:

- 31% front-end / 43% back-end as the base for borrowers with scores 580 and above

- 37/47 with one compensating factor

- 40/50 with two compensating factors

For borrowers with 500–579 or with no credit score, FHA manual underwriting stays at 31/43.

So the professional takeaway is:

- FHA baseline is 31/43

- FHA can often stretch to 50% back-end on manual files, but only under the compensating-factor matrix

- FHA is often more tolerant than conventional on ratio stress, but that does not mean ratios stop mattering

This is one of the biggest misconceptions in the field. FHA does not ignore DTI. It simply has a more structured way of permitting higher DTI when the rest of the file supports it.

What counts in DTI

Borrowers often misunderstand DTI because they think in terms of spending. Underwriters think in terms of counted obligations.

Debts that usually count

For standard mortgage qualification, the numerator usually includes:

- proposed housing payment

- minimum credit card payments

- auto loans and leases

- personal installment loans

- student loans

- child support, alimony, and maintenance

- HELOC or other real-estate-secured debt when payments are required

- other recurring obligations that underwriting rules require to be counted

Fannie Mae's liabilities guidance is clear that revolving accounts, installment debt, leases, student loans, real-estate loans, HELOCs, and support obligations generally count.

Debts and expenses that usually do not count

Standard DTI generally does not include:

- utilities

- cell phone bills

- internet or cable

- groceries

- streaming services

- commuting costs

- voluntary retirement contributions

- payroll deductions that are not debt obligations

One important nuance: saying "insurance doesn't count" is too sloppy. Homeowners insurance and mortgage insurance are part of the housing payment and therefore count in the front-end and back-end housing calculation. But auto insurance and health insurance are generally not standard DTI liabilities in the same way.

Student loans: this is where many DTI articles go wrong

This is the part that ages the fastest and gets misstated the most.

Fannie Mae student-loan treatment

Current Fannie Mae guidance says:

- if the borrower is on an income-driven payment plan and the lender verifies the actual monthly student-loan payment is $0, the lender may qualify the borrower with a $0 payment

- for deferred loans or loans in forbearance, the lender may use:

- 1% of the outstanding balance, or

- a fully amortizing payment using documented repayment terms

That means the old blanket shortcut "Fannie always uses 1%" is no longer clean enough. Sometimes 1% is used. Sometimes a fully amortizing documented payment is used. Sometimes a documented $0 IDR payment is usable.

FHA student-loan treatment

Current FHA policy is different.

For outstanding student loans, regardless of payment status, FHA generally uses:

- the payment on the credit report or the actual documented payment, if the payment is above $0

- 0.5% of the outstanding balance when the credit report shows $0

That means FHA is not simply "always 0.5%." If the credit report or documented actual payment is above zero, that actual payment can be the underwriting payment.

Why this matters

This is not academic. It changes approvals.

A borrower with $80,000 in student loans can look very different depending on the rule being applied:

- under a 1% proxy, that is an $800 monthly obligation

- under a 0.5% proxy, that is a $400 obligation

- under a documented IDR payment, it may be much lower

- under documented Fannie $0 IDR treatment, it may be $0

That is why bad student-loan assumptions kill otherwise good mortgage files.

Student-loan default, rehabilitation, and what it changes

Federal Student Aid says that after a borrower makes the required rehabilitation payments, Education will send a request to credit reporting agencies to remove the record of default from the account. CFPB adds the important nuance: rehabilitation does not remove the negative information from the missed payments prior to default. CFPB also says consolidation is much faster, but the default remains in the borrower's credit history.

That means rehab and consolidation do different things:

- Rehabilitation can remove the default notation, but it does not erase the earlier delinquencies that led up to default

- Consolidation can get the borrower out of default faster, but the default history remains on the credit file

For DTI purposes, the question is usually the current monthly obligation. For score and underwriting perception, the question is also whether the file still shows prior severe derogatory history. Those are not the same question.

This distinction matters because a borrower may improve the default status without fully cleaning up the historical credit damage, and a broker who does not understand that can overstate how much "rehab" actually changes the whole file.

How DTI and credit score work together

This is the part borrowers usually feel, but do not know how to describe.

A stronger score can support a higher DTI. It does not erase DTI, but it can help justify the stretch.

That is not just intuition. It is visible in the rules:

- Fannie manual ratios above 36% up to 45% require the borrower to meet score and reserve standards

- FHA manual stretch ratios above 31/43 depend on compensating factors and apply only in the higher-score bracket

So when professionals say "a better score helps with DTI," the precise version is:

A stronger score can help a file qualify for higher DTI tolerances because it acts as a compensating factor within the guideline framework.

That is much more accurate than saying "a high score overrides DTI."

Closing a card does not help DTI — paying the right debt can

This is one of the most expensive borrower mistakes.

Closing a credit card

Closing a card usually does not help DTI by itself.

If the borrower pays the balance off at or before closing, Fannie says the monthly payment on that debt does not need to be included for qualification purposes. But the account does not need to be closed for that exclusion to work.

That matters because closing a revolving account can hurt the score side of the file by reducing available credit and raising utilization. So if the goal is qualification, the borrower often needs the payoff, not the closure.

Paying off an installment loan

This is a true DTI lever.

If an installment loan is paid off and the monthly obligation is removed, the back-end ratio can improve materially. Fannie also says installment debts with 10 or fewer remaining monthly payments generally do not need to be included in long-term debt.

But there is a tradeoff: myFICO says paying off the last active installment loan can sometimes cause a score dip because active installment credit mix is part of the score logic.

So the right professional guidance is:

- paying off an installment loan can absolutely help DTI

- it may not help the score

- therefore the file has to be analyzed as a DTI-and-score interaction, not as a one-metric fix

The operational takeaway for professionals

The best DTI conversations do not begin with a target ratio. They begin with a correctly built numerator and denominator.

Use this workflow:

- Calculate front-end and back-end DTI correctly.

- Confirm which debts truly count.

- Treat student loans separately and apply the right program rule.

- Separate score optimization moves from DTI optimization moves.

- Do not tell borrowers to close cards just to "improve the file."

- Use installment payoff strategically when the monthly payment removal matters more than the potential score-side downside.

- Explain that higher scores can support ratio exceptions, but only within the actual guideline framework and lender overlays.

That is how you stop DTI from becoming the surprise that kills the file after the score work is already done.

To see how DTI interacts with rate pricing on the score side, see mortgage rate math. For the full intake workflow that catches DTI issues before they become surprises, see the pre-qualification checklist. For more professional credit strategy content, visit the For Pros hub.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →