Disclaimer: I am a credit systems engineer and strategist, not a CPA. This article covers credit scoring algorithms and data furnishing mechanics for educational purposes. Always consult a CPA for financial and tax-related matters.

Payment history is the foundational pillar of your FICO score — 35% of the algorithm, the single largest variable. Yet most advice about late payments stays surface-level: "pay on time." That's not engineering; that's a bumper sticker. To actually manage, mitigate, and recover from late payments, you need to understand how data furnishers transmit delinquency data to the bureaus, how the FICO algorithm interprets that data through scorecard segmentation, and what systemic failsafes prevent the damage from ever occurring. This guide covers all of it.

Late to Your Lender vs. Late to the Bureau

One of the most common points of confusion is the difference between missing a due date and receiving a derogatory mark on your credit report. They are not the same event, and they operate on completely different timelines.

The Grace Period: Lender-Level Consequences Only

Under the CARD Act of 2009, credit card issuers must provide a grace period of at least 21 days between the statement closing date and the payment due date. Most issuers offer 21–25 days. If your payment is due on March 5th and you pay on March 10th, you are late to the lender. The consequences at this stage are purely financial — a late fee of $29–$41, possible loss of a promotional 0% APR, or trigger of a penalty APR up to 29.99%. But none of this touches your credit report.

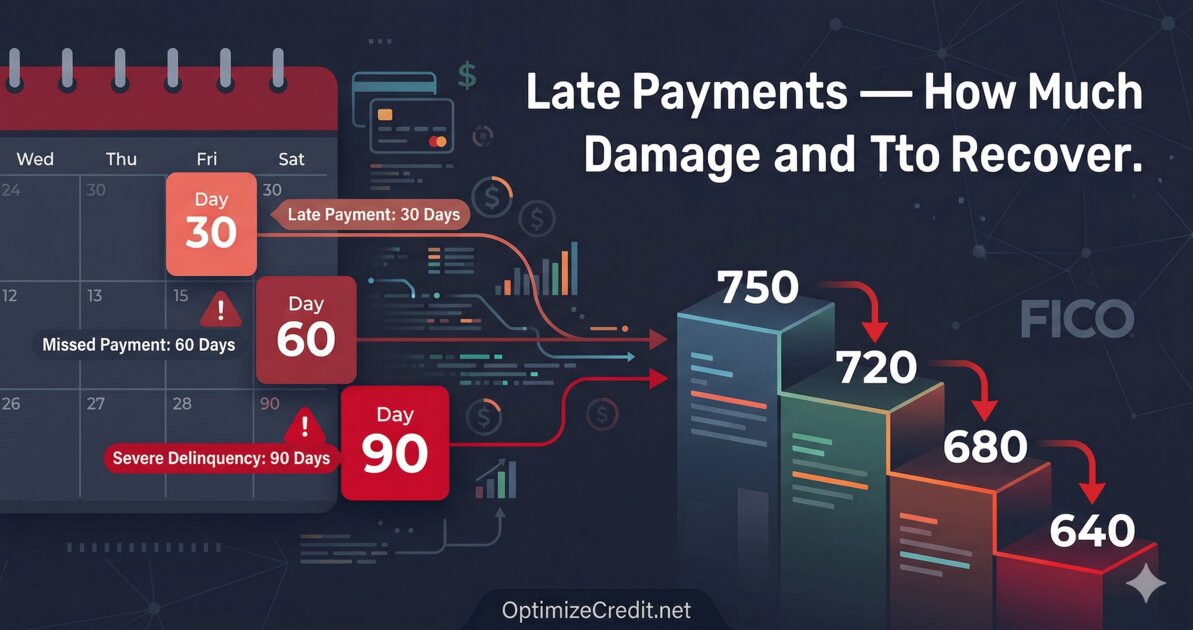

The 30-Day Threshold: Bureau-Level Damage

Credit bureaus don't accept reporting for accounts that are 5, 12, or 25 days past due. The industry-standard reporting format — Metro 2 — doesn't include a status code for anything under 30 days delinquent. A creditor cannot report you as late until you are a full 30 days past the original due date. Once you cross that threshold, the furnisher's automated batch process updates your profile with a Status Code 71 (Account 30–59 Days Past Due), and the algorithmic damage begins.

This means you have a real buffer: grace period (21–25 days after statement close) plus the 30-day reporting floor. But the moment day 31 arrives and your creditor's next Metro 2 file runs, the delinquency is locked into your report.

The Damage Scale: How Much Each Severity Level Costs

Not all late payments hit equally. FICO assigns escalating penalties based on how far past due you go, and the damage compounds at each stage.

| Delinquency Level | ~780 Score | ~680 Score | ~580 Score |

|---|---|---|---|

| 30-day late | −90 to 110 pts | −60 to 80 pts | −40 to 60 pts |

| 60-day late | −120 to 150 pts | −90 to 120 pts | −70 to 90 pts |

| 90-day late | −150 to 180 pts | −110 to 140 pts | −90 to 110 pts |

| 120+ days / Charge-off | −180 to 220+ pts | −140 to 180 pts | −110 to 150 pts |

The asymmetry matters: the cleaner your file, the harder you fall. This is because of FICO's scorecard segmentation system. A consumer with a 780 and no derogatory history sits on a "clean" scorecard. The moment a 30-day late appears, they're moved to a "dirty" scorecard where the maximum achievable score is significantly capped. A 680-score borrower already on a derogatory scorecard takes a smaller relative hit because the algorithm already accounts for prior risk signals.

What Happens at Each Stage

30 days past due — The entry point for credit damage. Manual underwriters may view an isolated 30-day late as an oversight, but automated systems don't distinguish intent. The damage is immediate and mechanical.

60 days past due — Signals a pattern, not a mistake. Lenders may begin "balance chasing" — reducing your credit limit to match your balance, which simultaneously spikes your utilization ratio and compounds the score damage.

90 days past due — Severe algorithmic penalty. Many lenders freeze or close the credit line entirely at this stage. The account may be flagged internally for collections review.

120+ days / charge-off — After 120–180 days, the lender charges off the account, writing it off as a loss. Even if you pay later, the charge-off status notation remains on your report. If the debt is sold to a collection agency, a separate collection tradeline may appear — doubling the visible damage. For recovery strategies at this stage, see our guide on charge-off recovery.

The 7-Year Clock: When It Starts and How the Pain Fades

Under the Fair Credit Reporting Act (FCRA), late payments must be removed from your credit report after 7 years. The clock starts on the Date of First Delinquency (DoFD) — the date of the original missed payment that led to the late status — not the date the account was closed, charged off, or sold to collections.

But the 7-year number is misleading if you think the damage stays constant. FICO's algorithm weights recency heavily, and the impact degrades on a predictable curve:

- Months 1–12: Maximum scoring damage. The late payment carries full algorithmic weight. This is the period most likely to cause application denials or push you out of competitive rate tiers.

- Months 13–24: Still significant, but softening. Borrowers with otherwise clean files begin to see measurable recovery, especially if utilization is controlled and no new delinquencies appear.

- Months 25–48: The late loses the vast majority of its algorithmic bite. Score recovery accelerates, particularly for isolated incidents surrounded by years of on-time payments.

- Months 49–84: Mostly cosmetic on score impact, though lenders conducting manual underwriting (common in mortgage) can still see the full history and may ask about it.

The critical insight: an isolated late payment fades faster than a pattern. One 30-day late surrounded by years of perfect history reads as an anomaly. Multiple lates across accounts reads as behavior — and the recovery timeline stretches accordingly.

Prevention: The Minimum Payment Autopay Failsafe

The single most effective prevention strategy is setting autopay to pull the minimum payment due on every account, scheduled to process 3–5 days before the actual due date.

This doesn't mean you should only pay the minimum — carrying balances at high interest rates is expensive. But minimum-payment autopay ensures that even if you forget, get busy, or miss an email notification, the 30-day clock never starts. You can always make additional manual payments or set a second autopay for the full statement balance.

One critical caveat: autopay requires sufficient funds in the connected bank account. A failed autopay due to insufficient funds doesn't protect you, and the returned payment can generate its own fee. Consider maintaining a buffer of 1–2 months of minimum payments in the linked account.

Goodwill Letters: When They Work and How to Write One

A goodwill letter is a written request to a creditor asking them to remove a late payment from your report as a courtesy. You're not claiming the information is inaccurate — you're acknowledging the late happened and asking the lender to voluntarily submit a Metro 2 update removing the delinquency notation.

When Goodwill Removal Works Best

Success rates run roughly 25–40% for well-crafted, first-time requests under favorable conditions:

- Isolated 30-day or 60-day late on an otherwise perfect payment history

- Long relationship with the creditor (5+ years)

- Clear, honest circumstance (medical emergency, natural disaster, job loss)

- Account is current and in good standing

- Smaller lenders, credit unions, and community banks tend to be more receptive than large national issuers

Sample Letter Structure

Send to the executive office or Office of the President — not general customer service. General frontline reps don't have the system access to manually override a Metro 2 reporting tape.

[Your Name and Address]

[Date]

Re: Account Number [last 4 digits] — Goodwill Adjustment Request

Dear [Executive Office / Office of the President],

I have been a customer since [year] and have maintained on-time payments throughout our relationship, with the exception of [month/year], when a payment posted [X] days late. This occurred because [brief, honest, one-sentence reason]. I take full responsibility and have since brought the account current.

I respectfully request that you exercise goodwill by removing the late payment notation from my credit file. Thank you for your consideration.

Follow up by phone 10–14 days after mailing. If denied, you can try once more in 6–12 months. Stop after two attempts; repeated requests to the same department rarely change the outcome.

When the Late Payment Is Inaccurate

If the late payment is genuinely wrong — the payment was made on time, the account isn't yours, or the dates are incorrect — this isn't a goodwill situation. File a formal dispute directly with each bureau reporting the error and simultaneously with the data furnisher via certified mail under FCRA Section 623.

Recovery Timeline: What to Realistically Expect

Recovery depends on the severity of the delinquency, your starting score, and what happens across the rest of your credit profile after the event.

Single 30-day late, clean file (740+): Most significant suppression occurs in the first 12 months. Expect meaningful recovery by months 12–18, with near-full recovery at 24–36 months assuming perfect subsequent behavior.

Single 30-day late, mid-range file (650–700): Faster relative recovery because the starting impact is smaller. Many borrowers see material improvement within 9–12 months with active credit management.

60–90 day late or multiple lates: Recovery stretches to 2–4 years. The scoring model needs an extended clean history to offset the behavioral pattern signal.

Charge-off: The longest road. Even after payment or settlement, the notation remains for 7 years. Meaningful score recovery typically takes 3–5 years of consistent positive behavior, often supplemented by adding new positive tradelines to rebuild the profile.

During recovery, focus on what you can control: keep utilization below 10% on all revolving accounts, avoid unnecessary hard inquiries, and ensure every payment across every account posts on time. The algorithm rewards consistency — each clean month compounds your recovery trajectory.

Understanding how payment history interacts with the other scoring components — utilization, age, mix, and inquiries — is essential for building an effective recovery plan. Our FICO five factors breakdown explains how these pieces fit together.

If your score dropped and you are not sure whether a late payment or something else caused it, the credit score debugging guide walks through a systematic audit process. For more troubleshooting strategies across payment history, disputes, and reporting errors, visit the troubleshooting hub.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →