A borrower with a 642 FICO is often closer to an approval than they think — but only if they work on the right factor.

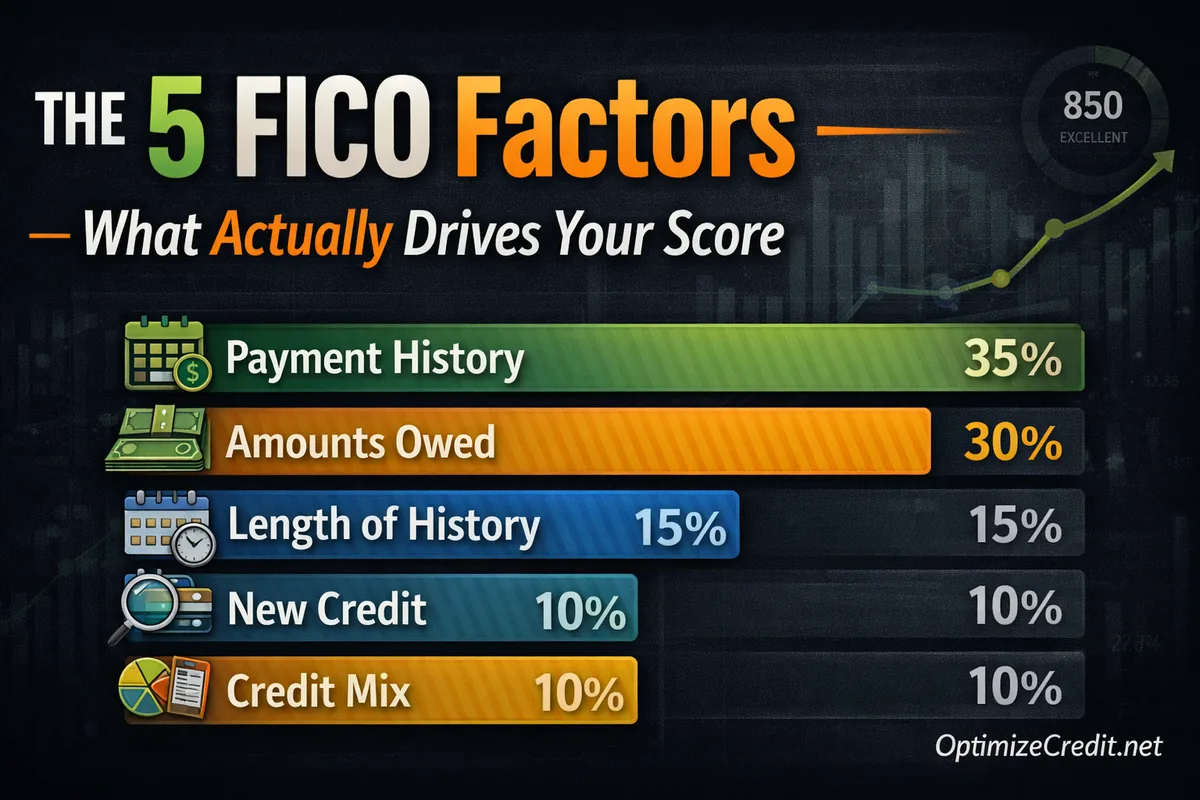

That is the part most people miss. A FICO score is not one vague judgment about whether you are "good with money." It is a weighted model built from five categories of credit data: payment history (35%), amounts owed or utilization (30%), length of credit history (15%), new credit (10%), and credit mix (10%). Those percentages come directly from myFICO's published breakdown.

The problem is that these factors do not move at the same speed. Some are slow, reputation-based signals that improve over months or years. Others are monthly math variables that can change as soon as the next reporting cycle hits the bureaus. If you are preparing for a mortgage, auto loan, or apartment application, that difference matters more than the percentages alone.

The practical takeaway is simple:

- Payment history is the most powerful factor, but it is usually the slowest to repair.

- Utilization is the second-largest factor and the fastest optimization lever because revolving balances typically update monthly.

- Length of history matters more than people think, but usually improves slowly.

- Credit mix helps, but is rarely the first lever to pull.

- New credit is easy to control fast by simply not making the file worse.

If you want one companion deep dive after this article, the most relevant is Utilization Math.

For the official weightings, see myFICO's explanation of what's in your FICO score.

The five factors at a glance

| Factor | Weight | What it measures | Speed of change | Best near-term use |

|---|---|---|---|---|

| Payment history | 35% | Whether you paid accounts as agreed | Slow | Stop new damage immediately |

| Utilization / amounts owed | 30% | How heavily you use revolving credit | Fast | Lower reported card balances |

| Length of credit history | 15% | Age of oldest, newest, and average accounts | Slow | Preserve older accounts |

| Credit mix | 10% | Variety of revolving and installment accounts | Medium to slow | Let it develop naturally |

| New credit | 10% | Recent hard inquiries and newly opened accounts | Fast to hurt, slower to help | Limit applications before major financing |

The control question is not just "Which factor matters most?" It is "Which factor matters most and can still move in time?" For most borrowers, that is utilization.

1. Payment history (35%): the heavyweight factor

Payment history is the biggest part of a FICO score. myFICO puts it at 35%, which is why lenders care so much about whether you have actually paid obligations on time.

This category reflects patterns like:

- on-time payments

- 30-, 60-, and 90-day late payments

- collections

- charge-offs

- bankruptcies and other severe derogatories

The hard truth is that this factor usually improves slowly. A legitimate late payment does not vanish just because you started paying on time again. The damage fades with time, but it does not usually disappear quickly.

That said, there are still fast actions that matter:

- Do not add a fresh late payment.

- Bring any past-due account current if possible.

- Dispute information only when it is actually inaccurate or incomplete.

- Set up systems — autopay, reminders, due-date alignment — so the file stops getting worse.

The CFPB says you can dispute errors on your credit report with both the credit reporting company and the company that supplied the information. The credit reporting company generally must investigate within 30 days, though some situations can extend to 45 days.

Why this factor feels unfair

Because it is backward-looking by design. Payment history is supposed to tell lenders whether you have a track record of honoring debt. That is why it is the most important factor and why it does not respond quickly to cosmetic changes.

Student loan note

Student loans fit here too. Federal student loan servicers say delinquency is generally reported to the nationwide consumer reporting agencies starting at 90 days past due, and default creates additional negative credit consequences. If a defaulted federal loan is later rehabilitated, the default notation can be removed, but the earlier missed-payment history remains.

2. Utilization (30%): the fastest major lever

If payment history is the anchor, utilization is the steering wheel.

myFICO says amounts owed makes up 30% of your score, and revolving utilization is a major part of that category. Utilization compares reported balances with available revolving limits. For the full math breakdown, see Utilization Math.

The basic formula is:

total revolving balances ÷ total revolving credit limits

That means the same $4,000 balance can look very different:

- $4,000 on $5,000 of limits = 80% utilization

- $4,000 on $20,000 of limits = 20% utilization

Same debt. Different scoring signal.

Why utilization is the #1 optimization lever

Experian says lenders and creditors typically update credit information at least monthly, and credit card issuers commonly report after the billing cycle closes. That means when you lower reported balances, the score can react relatively quickly once the new statement balance hits the bureaus.

That is why utilization is the best near-term target for many borrowers preparing for financing. It is not the largest factor overall, but it is the largest factor that often moves on a monthly cycle.

What helps most

- Pay down balances before statement closing dates, not just before the due date.

- Reduce balances on cards that are heavily utilized, even if total utilization looks acceptable.

- Avoid large charges right before an application.

- Verify whether recent payments have actually been reported yet.

What people get wrong

They assume "I paid it" and "the bureau sees it" are the same thing. They are not. Scoring works off reported balances, not your internal math.

3. Length of credit history (15%): slow, but structurally important

Length of credit history is 15% of a FICO score. myFICO says this category considers how long your accounts have been established, including the age of your oldest account, newest account, and the average age of all accounts.

This is one reason seasoned files often outperform brand-new files even when both are currently paid as agreed. Time adds evidence.

Can you control it fast?

Usually only a little. Time does most of the work.

But you can avoid damaging it:

- Keep strong older accounts open when practical.

- Avoid opening unnecessary new accounts.

- Be cautious about "credit-building" moves that reduce average age without solving the real problem.

Where authorized users fit

Experian says becoming an authorized user on someone else's credit card can help establish or improve credit history if the issuer reports authorized-user data and the primary account holder manages the account well. That means an older, well-managed authorized-user account can sometimes help a thinner or younger file faster than waiting years. But the benefit is not universal or guaranteed.

What people get wrong

They open several new cards to "build credit faster," then wonder why the score gets temporarily worse. New accounts may help in the long run, but they can reduce average age immediately.

4. Credit mix (10%): useful, but often overplayed

Credit mix is 10% of a FICO score. It reflects the variety of credit types on the report, especially the difference between revolving accounts and installment accounts. myFICO says installment loans such as mortgages, car loans, and student loans, along with revolving accounts like credit cards, contribute to this category.

This is the category people tend to misread. Yes, a balanced file can help. No, that does not mean you should open random loans just to "improve mix."

Where student loans fit

Student loans are installment debt, so they can support credit mix and positive payment history when managed well. Experian says student loans can help establish your credit report, thicken your file, add to credit mix, and build payment history if paid on time. Missed payments, on the other hand, can hurt just like with other loans.

Best practical use

For most borrowers, let mix improve naturally. If your file is extremely thin, mix may matter more — but it is still usually not the first lever before a short deadline.

What people get wrong

They chase new installment accounts when the real issue is a maxed-out credit card or a recent late payment.

5. New credit (10%): the easiest factor to stop hurting

New credit accounts for 10% of a FICO score. myFICO says inquiries can remain on your credit report for two years, though FICO Scores generally consider them for the past 12 months. Opening new accounts can also lower your average age of accounts.

This category is about:

- hard inquiries

- newly opened accounts

- how recently you have sought credit

What you can control fast

You can stop making it worse immediately.

That means:

- no unnecessary card applications before a mortgage, auto loan, or lease screening

- no "store card for 15% off" decisions right before financing

- no opening of accounts just because a preapproval email arrived

What people get wrong

They hear "only 10%" and think it barely matters. On a borderline file, a few avoidable inquiries or a brand-new account can still be the difference between clearing a threshold and missing it.

The control matrix: what moves fastest, and what to do first

| Factor | Weight | Speed to improve | Best strategy | Common mistake |

|---|---|---|---|---|

| Payment history | 35% | Slow | Prevent new lates; dispute only true errors | Focusing on old damage while still paying late now |

| Utilization | 30% | Fast | Lower reported card balances before statement close | Paying after statement close and expecting immediate score relief |

| Length of history | 15% | Slow | Preserve older accounts; avoid needless new ones | Opening multiple new accounts to "build faster" |

| Credit mix | 10% | Medium to slow | Let mix improve naturally unless file is very thin | Opening loans you do not need just for mix |

| New credit | 10% | Fast to hurt, slower to help | Pause applications before major financing | Treating preapprovals like harmless offers |

Which factor should you attack first?

Usually this order works best:

- Stop current damage — get current and stay current.

- Fix utilization — this is the fastest major lever.

- Review for errors — use actual reports, not just score apps.

- Protect age — avoid unnecessary new accounts and casual closures.

- Let mix develop naturally.

The CFPB notes that each credit bureau may have somewhat different information, which is why reviewing the underlying reports matters so much when you are trying to understand or improve a score.

Bottom line

The five FICO factors are not equal in either weight or speed.

- Payment history matters most, but usually heals slowly.

- Utilization is the fastest major optimization lever.

- Length of history matters more than people think and is easy to damage.

- Credit mix helps, but usually later.

- New credit is easy to underestimate and easy to mishandle.

If you remember only one thing, remember this: utilization is the best short-term lever, but payment history is still the foundation. Fast score improvement usually comes from managing the 30% factor without damaging the 35% factor.

To understand how these factors play out across different scoring models, see FICO vs. VantageScore. And if you are working with a lender who can push updated data mid-process, the rapid rescore guide explains how that works.

For a broader view of all the fundamentals, return to the Credit Basics hub.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →