How to help your kid reach a 750 credit score before turning 18

Direct answer: You can help your teenager work toward a 750 credit score before they turn 18, but it is not a button you press. It depends on adding them as an authorized user to a clean, older, low-utilization card whose issuer reports authorized users to all three bureaus, monitoring the file, and layering primary credit once they turn 18. The 750 result is realistic, not guaranteed.

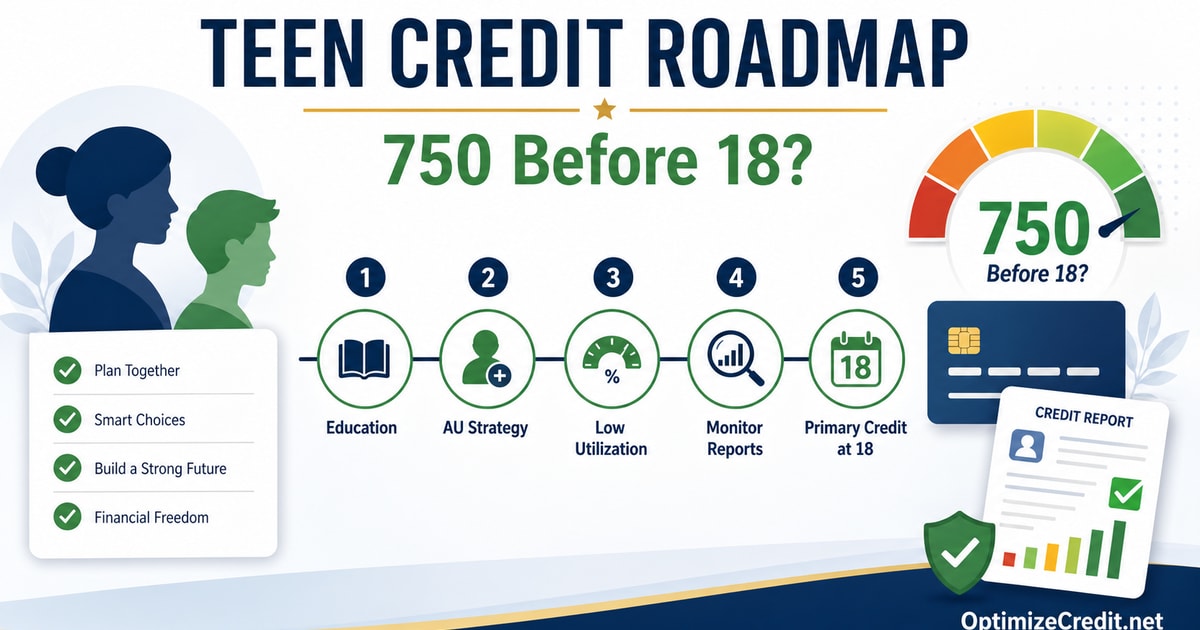

The fastest path is usually: teach the basics, open a teen checking account, audit your own card, add the teen as an authorized user on that card if it qualifies, monitor the credit report, and graduate the teen to a primary secured card at age 18. Each move builds on the last. None of them require buying anything, in most cases.

The 7-step parent roadmap

- Teach the basics first. Before any account is added, the teen should understand statements, due dates, utilization, and what a credit report actually is. Credit follows behavior, and behavior follows literacy.

- Open a teen checking account. Banking habits come before credit. A teen checking account introduces statements, balances, and direct deposit, and is usually available with a parent as a joint owner.

- Audit your own card before adding them. The card you choose should be at least 2 years old, low-utilization, and on perfect payment history. If your own card has any 30 day late or chronic high balance, do not use it.

- Confirm the issuer reports authorized users to all 3 bureaus. Call the issuer or read the cardholder agreement. Some issuers do not report AU activity. Some only report after age 18. That single detail decides whether the strategy works at all.

- Add the teen as an authorized user. You do not have to physically issue a card to your teen. Reporting is what matters. The card can stay in your wallet.

- Monitor the teen's credit report monthly. Pull the file from AnnualCreditReport.com about 30 to 60 days after the AU is added, and again every month while the AU account is in place.

- Layer a secured card or starter card at 18. When your teen turns 18, transition them to a primary account in their own name so the file is no longer dependent on inherited authorized user history.

How authorized user status actually works

An authorized user is a person added to someone else's credit card account. The authorized user can be issued a card and can make purchases, but they are not legally responsible for the debt. The primary cardholder owns the account and the balance.

What makes the strategy powerful for teens is that many issuers report the entire account history -- age, payment record, utilization -- to the authorized user's credit file. That means a teen with no credit history can inherit a multi-year clean account in one move. myFICO confirms that authorized user accounts can appear on credit reports and influence FICO scores, that both positive and negative information from the primary account can matter, and that the authorized user is never legally responsible for the debt.

Experian's parent guide reinforces the same approach. It tells parents to help teens build credit by teaching credit basics, opening checking accounts, adding teens as authorized users, monitoring credit history, considering secured cards once the teen is age-eligible, and modeling good credit behavior themselves.

What kind of card do you actually want to use?

Not every card is a good authorized user candidate, even when the issuer technically allows minors. The card you select for your teen should hit four conditions:

- Old. Ideally 2 or more years of history. The longer, the more age the teen inherits.

- Clean. No 30, 60, or 90 day late payments anywhere in the history. No charge-offs. No collections.

- Low utilization. Reported balance under 10 percent of the limit, ideally under 5 percent, every statement.

- Reports AU data to all 3 bureaus. Without this, the rest of the work goes to waste.

Experian explicitly warns that authorized user status can help if the primary account owner manages the card well, and it can hurt if the account has high utilization or missed payments. The same logic applies in reverse when you are the primary and your teen is the authorized user -- your card behavior becomes their credit history.

The teen credit-building moves at a glance

| Teen credit-building move | Minimum age or timing | Risk | Best use |

|---|---|---|---|

| Teen checking account | Usually 13+ with parent as joint owner | Very low | Build banking habits before any credit account exists |

| Authorized user on parent's card | Issuer-dependent (some allow any age, others 13+ or 16+) | Low if the parent's card is clean and low-utilization | Inherit age, payment history, and utilization profile from a strong primary card |

| Authorized user via marketplace tradeline | Issuer-dependent | Moderate (cost, temporary, depends on issuer reporting) | Used when the parent's own card does not qualify as a clean AU candidate |

| Secured credit card | 18+ | Low if paid in full each month | First primary account in the teen's own name |

| Credit-builder loan | 18+ | Low (the loan amount is locked in savings) | Add an installment account so the file is not card-only |

| Student credit card | 18+ with verifiable student status or income | Low if utilization stays under 10 percent | Replace the AU strategy with a real primary account once eligible |

Issuer rules vary -- verify before you add

Issuer policies on minor authorized users are not standardized. Some issuers allow authorized users at any age. Some require 13, 15, or 16. Some allow minors but only report the AU account to the bureaus once the teen turns 18. Some report to one bureau, some report to all three. None of this is consistent across the industry, and policies change.

Before you add your teen, confirm with your issuer:

- The minimum age for an authorized user on this card

- Whether the issuer reports authorized user accounts to Experian, Equifax, and TransUnion

- Whether reporting starts immediately or only at age 18

- Whether the issuer will physically mail a card to the teen, or just add them on file

If your issuer does not report authorized user activity to all three bureaus, your teen's score will only build on the bureaus that receive the data. That is not always a deal-breaker, but it caps the upside.

Banking habits and basic education come first

Credit follows behavior. Before any card touches your teen's file, they should know how to:

- Read a bank statement

- Reconcile spending against expected balance

- Plan for a recurring bill

- Understand that minimum payment is not the same as paid in full

- Recognize that a credit card is a loan, not free money

A teen checking account is the simplest way to introduce all of this. Once the teen has handled a debit card responsibly for several months, the leap to a secured card or authorized user account is much smaller. The building credit from zero guide walks through the same logic for adults starting from scratch, and the playbook applies cleanly to teens too.

Secured cards and credit-builder loans at 18

Once the teen turns 18, they can apply for credit in their own name. The two most common starter products are:

- Secured credit cards. The teen deposits a refundable amount that becomes the credit limit. The card reports as a primary account on their own file.

- Credit-builder loans. A small installment loan that locks the loan amount in a savings account while the teen makes monthly payments, building a payment record.

Both products work, but they fit different goals. The secured cards vs credit-builder loans comparison shows when each one wins and how to choose. The point of layering a primary account at 18 is to give the teen independent credit, not just inherited authorized user history. myFICO notes that primary accounts matter more over time, and that is the structure lenders eventually want to see.

Monitoring the teen's credit file

Pull your teen's credit report at least once before the AU account is added (to confirm there is no fraud or identity issue), and again 30 to 60 days after.

AnnualCreditReport.com is the official free source for credit reports from all three bureaus. Many teens have no file at all on record there, which is normal and not a problem. After the AU account is added, the report should start showing the new account once the issuer reports the next cycle. If nothing appears within 60 days, call the issuer.

Timing across bureaus is not always identical. The statement date vs bureau update guide explains why one bureau can show a new account weeks before another, and what to do when the gap looks longer than expected.

Watch the utilization on the AU account

Your teen's apparent utilization is your utilization. If the parent runs the card to 60 percent before paying it off, the teen's file may briefly look like a 60 percent utilization profile to scoring models. The utilization math guide walks through why even a one-month spike at the statement closing date can land on the report.

The clean rule: keep the reported balance under 10 percent of the limit at the statement closing date, every month, while your teen is an authorized user. If the parent cannot reliably commit to that, the AU strategy on that card is the wrong move.

Warnings parents need to take seriously

- Do not add a teen to a card with late payments. A 30 day late on the primary account can flow through to the teen's file. You are not handing them a head start, you are handing them your problem.

- Do not add a teen to a high-utilization card. A card that consistently runs above 30 percent utilization will hurt the teen's file the same way it hurts yours.

- Do not hand over spending access unless the teen is ready. Authorized user status does not require giving the teen a physical card. You can add them for credit-reporting purposes only and keep the card in your wallet.

- Do not promise an exact score. A 750 score before age 18 is realistic for a teen riding a clean older account, but it is never guaranteed. Issuer reporting rules, AU age policies, and the parent card's utilization all change the result.

When OptimizeCredit's authorized user tradelines fit, and when your own card is better

If the parent has a clean older card with low utilization and the issuer reports authorized users to all three bureaus, the parent's own card is almost always the better choice. It is free, it is permanent for as long as the parent keeps the teen on it, and there is no marketplace involved.

The calculation only changes when the parent's own profile cannot do the job:

- The parent has no card older than about 2 years

- The parent's card history includes a recent late payment or charge-off

- The parent runs high balances and cannot reliably keep utilization low

- The parent's issuer does not report authorized user accounts to all three bureaus

- The parent does not want their teen tied to a personal account for relationship or estate reasons

In any of those cases, a seasoned authorized user tradeline from OptimizeCredit's tradeline marketplace can give the teen a clean, vetted account that is age-appropriate and known to report to all three bureaus. Tradelines are paid and they are temporary, so the right call is usually: use the parent's card if it qualifies, and use a marketplace tradeline only if the parent's card does not. The AU tradeline effect guide explains what determines whether the boost is meaningful for the file receiving it. The same logic applies whether the authorized user is the parent's spouse, the parent's teen, or anyone else.

Use the optimizer to plan the move

Every teen file is different. Some have nothing on file. Some already have a thin checking record. Some have a fraudulent account because of identity theft, which is more common than parents expect. Before you change anything, run the teen's credit report -- or the parent's, if you are deciding which card to add the teen to -- through the OptimizeCredit free credit analyzer. It identifies the actual weak points and tells you which moves matter most for that specific situation, in the right order. The boost credit score fast guide walks through the diagnostic flow and shows what kind of recommendations the optimizer returns.

The 750 score question, answered honestly

A teen can cross 750 before age 18 when the file conditions are strong enough. It happens routinely when:

- The parent's card is 5 or more years old

- Utilization stays under 5 percent at the statement closing date

- The card has no late payments, no charge-offs, no collections

- The issuer reports the authorized user account to all three bureaus

- The teen has no derogatory items, no fraud, and no competing thin accounts pulling the file in the wrong direction

It does not happen when those conditions are violated. The score is a math result, not a promise. Build the conditions correctly and the score has a better chance to follow. Diagnose first, add the right account, monitor the file, and graduate to primary credit at 18 -- that is the entire game.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →