Credit utilization is math, not folklore. While the common "stay under 30%" rule is repeated everywhere, that number is closer to a damage-control threshold than a target for top-tier rates. If you want to understand why your score moves, you need to know the formula, the difference between individual-card and overall utilization, and how credit limits and account age change the equation.

How is credit utilization actually calculated?

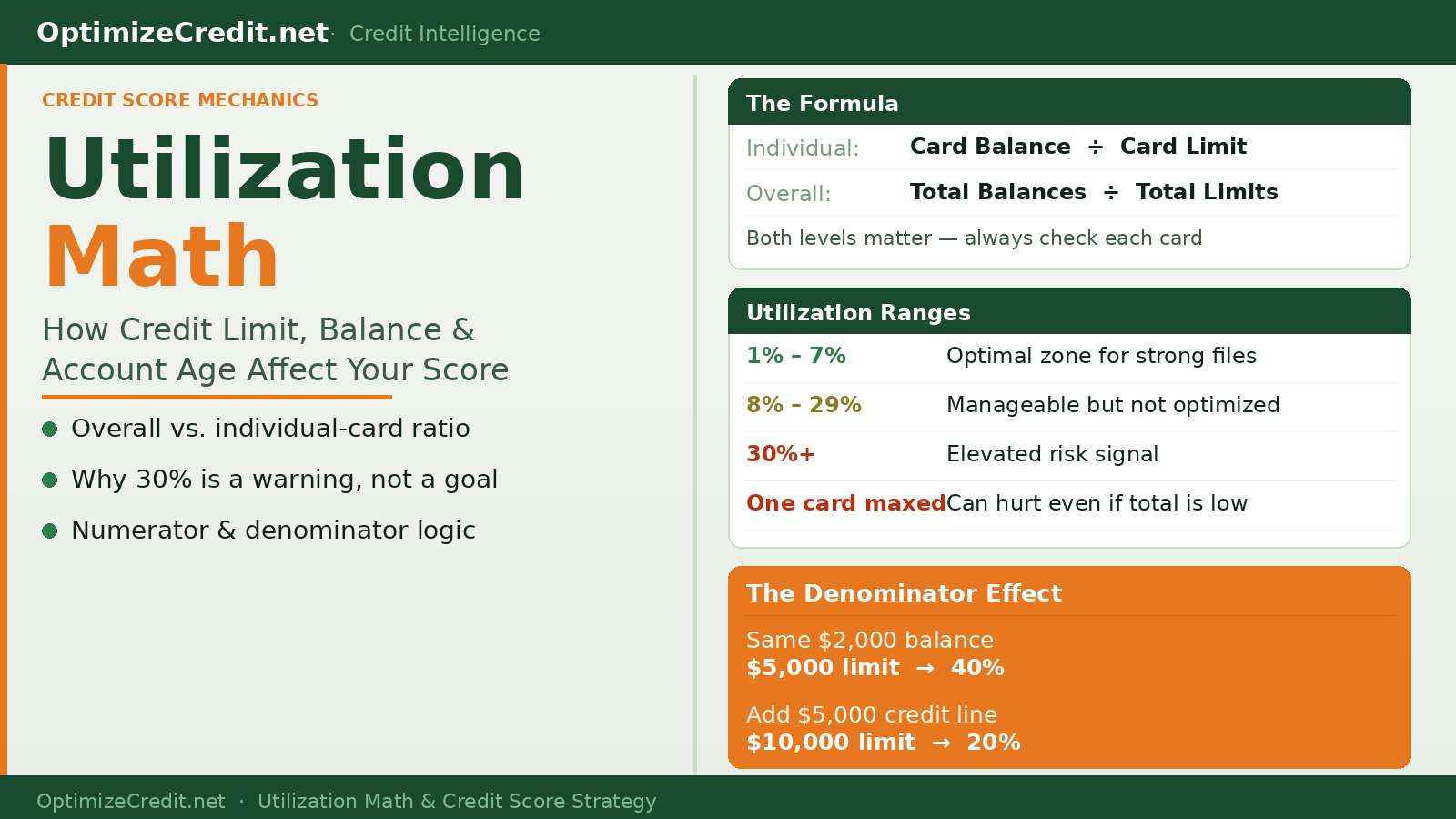

At the simplest level:

Utilization = Reported revolving balance / Reported revolving credit limit

That math exists at two levels:

- Individual-card utilization

- Overall utilization across all revolving accounts

Both matter. You can see the exact formula breakdown from Experian's credit utilization guide.

The formula box

| Formula type | Formula | Why it matters |

|---|---|---|

| Individual-card utilization | Card balance / Card limit | One heavily used card can hurt even when total utilization looks fine |

| Overall utilization | Total revolving balances / Total revolving limits | Gives the model a file-level view of how stretched your revolving debt looks |

This is why utilization analysis always needs two questions:

- What is the total ratio?

- What is the worst single-card ratio?

Why the 30% utilization rule is a failing grade

The 30% rule is useful only as a rough warning line. It is not an "excellent credit" target.

If your goal is top-tier pricing, 30% is often too high. Low single digits are usually much stronger.

That does not mean every file behaves identically. But the practical idea is:

- 30% may be "less bad" than 70%

- It is not the same thing as optimal

So the smarter question is not "am I under 30%?" It is "what ratio gives my file the cleanest risk signal?"

Does one card's utilization hurt your score even if your total is low?

Yes, it can. If you have been told your overall utilization looks fine but your score still dropped, the utilization trap is worth reading.

Example:

- Card A limit: $10,000 — balance: $500

- Card B limit: $1,000 — balance: $900

Overall utilization: $1,400 / $11,000 = about 13%. That sounds fine at first glance.

But Card B is at 90% utilization, and that can still create a strong risk signal. This is why some borrowers say, "My overall utilization is low, so why did my score still drop?" The answer is often that one card is doing disproportionate damage.

The numerator: why reported balance matters more than memory

For utilization purposes, the important number is usually the reported balance, not the balance you remember paying later.

If your card closes with a $2,000 statement balance on a $5,000 limit, the utilization snapshot may be 40% even if you pay it in full a few days later.

That is why the statement-date article matters. The formula works only on the numerator that reaches the bureaus.

The denominator: how total credit limits change the math

The denominator is your total available revolving credit.

If your balances stay the same but your total limits rise, utilization falls.

Example:

- Balances = $2,000

- Total limits = $5,000

- Utilization = 40%

Add a new $5,000 revolving line and keep balances the same:

- Balances = $2,000

- Total limits = $10,000

- Utilization = 20%

That is why adding available revolving credit can improve the math so quickly. There are several ways to increase the denominator without opening a new primary account. Requesting a soft-pull credit limit increase from an existing issuer adds available credit without a hard inquiry on many cards. Choosing a strategic new card that fits the file's age profile is another option. And for files where the primary suppressor is revolving depth, an authorized user tradeline can add limit without a new application — for more on that mechanic, see how AU tradelines affect different credit files.

Does closing a credit card hurt utilization?

Often yes.

If you close a card, you may reduce the denominator. That means the same balances now consume a larger percentage of your available credit.

Example:

- Balances = $1,500

- Total limits = $10,000

- Utilization = 15%

Close a $4,000-limit card:

- Balances = $1,500

- Total limits = $6,000

- Utilization = 25%

The debt did not increase. The denominator shrank.

That is why closing a card can hurt even when you never missed a payment.

How does opening a new card affect your credit score?

Opening a new card is a trade-off.

Potential benefits:

- Increases the denominator

- Lowers utilization if spending stays stable

- May improve file depth over time

Potential costs:

- Adds a hard inquiry

- Lowers the average age of accounts

- Creates a new-account risk signal

- Can hurt more on thin files than on mature files

So the question is not "is a new card good or bad?" The real question is whether the denominator benefit outweighs the age and inquiry costs for your specific file. The optimizer can model this trade-off before you commit to an application.

The account-age trade-off

Utilization is not the only math in play. Age matters too.

That means when you open or close accounts, you are often changing:

- Available credit

- Average age

- The number of active tradelines

- The balance-to-limit ratio

This is why optimization is rarely about one variable in isolation.

Why "30%" and "excellent" are not the same thing

Here is the practical ranking many borrowers miss:

| Utilization range | Rough interpretation |

|---|---|

| 0% | Can be fine, but not always the strongest optimization signal |

| 1% to 7% | Often the cleanest optimization range for strong files |

| 8% to 29% | Usually manageable, but less optimized |

| 30%+ | Elevated risk signal for many use cases |

| Very high single-card utilization | Can hurt even when total utilization looks acceptable |

That is why "under 30%" is too blunt to be the main rule.

Charge cards and no-preset-limit cards are an exception people miss

Cards without a traditional preset limit do not always behave like ordinary revolving cards in utilization calculations.

That means some charge-card products may:

- Not contribute to utilization the same way

- Still affect underwriting perception in other ways

- Create confusion if the borrower assumes every account has the same denominator logic

So if your file includes charge cards, do not assume the utilization math is identical to a standard fixed-limit revolving card.

Why age still matters even in a utilization article

If you optimize only utilization and ignore age, you can make short-term gains at the cost of longer-term file strength.

Examples:

- Opening too many cards quickly can lower average age

- Closing your oldest card can reduce both age strength and denominator

- Thin files can be much more inquiry-sensitive than thick files

This is why utilization strategy should be connected to file structure, not treated as a standalone game.

Where authorized-user tradelines fit into utilization math

Authorized-user tradelines can affect utilization math by adding available revolving credit and, sometimes, lower-balance aged history without opening a new primary account.

That matters because an AU account can improve the denominator without:

- Requiring a new primary application

- Adding a new hard inquiry to the borrower's file

- Lowering average age the same way a new primary account can

That does not mean an AU tradeline is always the right move. It means the denominator effect is one reason they can matter.

What to do with this math

Use the math in this order:

- Calculate overall utilization.

- Calculate each card's utilization.

- Identify which card is causing the worst signal.

- Check when that card reports.

- Decide whether the better move is:

- Paying down the numerator

- Increasing the denominator (soft-pull CLI, strategic card, or AU tradeline)

- Preserving older accounts

- Avoiding a counterproductive new application

That is how you move from vague advice to actual optimization.

Conclusion

Utilization is not just "keep it under 30%." It is a set of formulas interacting with your limits, balances, timing, and account age. Once you understand the numerator and denominator, the score becomes less mysterious. The real goal is not just lower debt. The real goal is a cleaner reported balance-to-limit picture across the entire file.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →