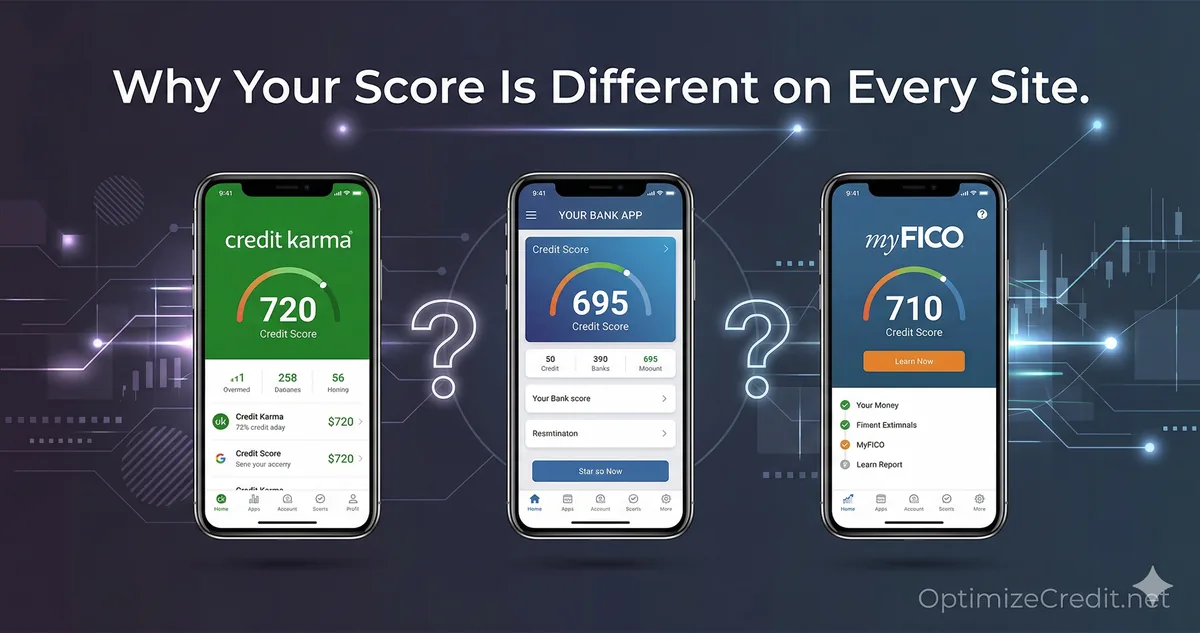

You check Credit Karma and see 712. Your bank app shows 681. A lender later pulls something much lower.

Same person, same month, maybe even the same week, yet three different numbers.

That does not mean one score is fake. It usually means you changed one of three things: the scoring model, the bureau data, or the time the score was pulled. CFPB says consumers can have many different credit scores, and the score sold or shown to a consumer may not be the same score a lender uses in a real credit decision. Credit Karma also says its free scores are VantageScore 3.0 scores from Equifax and TransUnion, and that a score from another source may differ because it used a different model or version.

That is the whole article in one sentence: different formula + different bureau + different day = different score. The real question is not "Which score is the one true score?" The real question is "Which score matters for the loan or approval I care about right now?"

The three variables behind every score difference

1) The scoring model

A credit score is not a fixed fact like your date of birth. It is the output of a formula. Change the formula and the number changes.

This is the biggest source of confusion. Credit Karma says it provides VantageScore 3.0 from Equifax and TransUnion. Many lenders, meanwhile, use some version of FICO. CFPB says lenders use many different scoring models, and the most widely used are FICO scores, but consumers can also be shown many other scores.

That means these can all be valid at once:

- Credit Karma: VantageScore 3.0

- Bank dashboard: FICO Score 8

- Mortgage lender: FICO 2 / 5 / 4

- Auto lender: FICO Auto Score

- Card issuer: FICO Bankcard Score or FICO 8

None of those numbers is automatically "wrong." They are just different models built for different use cases. Understanding the differences between FICO and VantageScore makes this gap less confusing.

2) The bureau data

Even if two companies use the same scoring model, the number can still differ because the underlying credit report is different.

myFICO says your FICO Scores can vary from bureau to bureau because your credit file can vary from agency to agency, and because scores can change depending on when they are calculated. Credit Karma says the same thing in simpler language: different bureaus can have different information, and timing differences can matter.

That is normal. Not every creditor reports to every bureau in the same way or on the same schedule. One bureau may already show a lower balance, while another still shows the prior statement balance. One may reflect a newly opened account while another is a few days behind. Same person, different bureau file, different output. Knowing how lenders use bureau scores helps you understand why these differences matter in real decisions.

3) The pull timing

Scores are snapshots, not live streams.

myFICO says score differences can occur because the scores were not accessed at the same time, and that comparing a week-old score from one bureau with a fresh score from another can be misleading. Credit Karma also notes that more recent activity can affect the score shown on one platform but not another.

This is especially important if your file is sensitive to utilization. A card that reports at 72% utilization on Tuesday can easily produce a lower score than the same file on Monday before the statement balance posted. So even with the same model and same bureau, different timing can still create a visible score gap. The statement date vs. bureau update guide explains exactly how this timing mismatch works.

Why Credit Karma, your bank, and your lender often disagree

This is the most common consumer confusion:

- Credit Karma shows VantageScore 3.0 from Equifax and TransUnion.

- A bank or card issuer may show a free FICO Score, usually from one bureau. Discover offers a free FICO Score through Credit Scorecard. American Express MyCredit Guide provides FICO Score 8 based on Experian. Bank of America says it provides a free FICO Score in Online Banking using TransUnion data.

- A lender may use something else entirely, depending on the product.

That is why "my score is 712" is not enough information. A useful score statement needs four pieces:

- Model family

- Version

- Bureau

- Date pulled

Without those, you are often comparing apples to oranges.

The educational-score problem

A lot of score confusion comes from what I call the educational-score problem.

Some consumer-facing scores are excellent for monitoring trends. They help you spot a utilization spike, a new collection, an inquiry, or a reporting error. But CFPB has repeatedly warned that the score shown or sold to a consumer may not be the same score a lender uses to make a real decision, and its study found that roughly one in five consumers would likely receive a meaningfully different score than a lender would.

That does not make the free score useless. It just means you should treat it as a monitoring tool, not a guaranteed preview of a mortgage, auto, or card underwriting pull.

FICO is not one score — it is a whole family of scores

This is the piece most consumers never get told.

myFICO's official score-version page shows multiple base FICO scores, multiple mortgage scores, multiple Auto Scores, and multiple Bankcard Scores across the three bureaus. That is already well over two dozen active versions before you even count all the bureau-specific implementations listed on the page.

Here is the practical takeaway:

| Product type | Score family commonly relevant | What to know |

|---|---|---|

| Mortgage | Classic mortgage FICO: 2 / 5 / 4 | Historically the key mortgage set |

| Auto loan | FICO Auto Score 8 or 9 | Tuned for auto risk |

| Credit cards | FICO Bankcard Score 8 or 9 or base FICO | Tuned for revolving behavior |

| Free monitoring apps | Often VantageScore 3.0 | Good for trend tracking, not always lender-relevant |

That is why "my FICO score" is not specific enough. You need the version and bureau.

Which score matters by loan type?

Mortgage

For mortgage prep, the traditional answer is still the classic mortgage set:

- Experian FICO Score 2

- Equifax FICO Score 5

- TransUnion FICO Score 4

myFICO identifies those as the versions used in mortgage lending. Fannie Mae still requires a three in-file merged credit report, and for a single borrower the applicable credit score is the representative credit score. In practical mortgage language, that is the middle of the three bureau-specific mortgage scores on the merged report. myFICO's mortgage plan page also explains the same consumer-facing concept: mortgage lenders use the "middle score" from the three bureaus.

One important current nuance: FHFA announced in July 2025 that lenders delivering loans to the Enterprises will be allowed to use either Classic FICO or VantageScore 4.0 during the interim phase, while keeping current credit-reporting requirements in place initially. Classic FICO remains approved, and tri-merge requirements remain in place for now. So for actual mortgage prep today, classic mortgage-score awareness is still essential.

Auto lending

Auto lenders often use FICO Auto Score variants rather than the base FICO score you may see in a bank app. myFICO's version page specifically lists FICO Auto Score 8 and FICO Auto Score 9, along with older bureau-specific Auto Score versions.

So if your bank shows a decent FICO 8 but a dealership quotes something different, that is not automatically a mistake. It may simply be an auto-specific scoring model.

Credit cards

Credit card issuers often use either a base FICO score such as FICO Score 8 or an industry-specific FICO Bankcard Score. myFICO's official list includes FICO Bankcard Score 8 and FICO Bankcard Score 9 among the versions used in credit card decisioning.

That is why the number shown inside a card issuer's app can be closer to real card-approval logic than a generic monitoring score, but still not match your mortgage or auto score.

Where can you see something useful?

If you want scores that are more relevant than a generic monitoring number, use sources that clearly tell you the model and bureau.

| Source | What it is useful for | What it usually shows |

|---|---|---|

| myFICO | Best for mortgage and multi-version prep | Classic mortgage, auto, bankcard, and base FICO versions |

| Discover Credit Scorecard | Good free FICO monitoring | Free FICO Score access |

| American Express MyCredit Guide | Good single-bureau FICO monitoring | FICO Score 8 based on Experian |

| Bank of America FICO dashboard | Good single-bureau FICO monitoring | Free FICO Score using TransUnion data |

| Credit Karma | Good free trend tracking | VantageScore 3.0 from Equifax and TransUnion |

Also remember that AnnualCreditReport.com gives you free weekly credit reports, not lender scores. It is the right place to inspect raw bureau data, not the right place to see your mortgage middle score.

The easiest way to debug score differences

If you want to stop feeling like the system is random, use this sequence:

- Write down the model shown on each site.

- Write down the bureau each score uses.

- Check whether the scores were pulled on the same day.

- Pull your raw reports from AnnualCreditReport.com to see whether balances, limits, inquiries, or collections differ across bureaus.

- Before any major application, check the specific score family that lender type usually uses.

Once you do that, most score discrepancies stop being mysterious. They become explainable.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →