Why a clean credit report can still get denied

A clean credit report is not necessarily a strong one. Many borrowers are shocked to get denied despite having zero late payments, but the denial is often about insufficient data, not negative data. If your report only has one or two young accounts, you may be thin, fragile, or effectively unscorable to the underwriting model that matters.

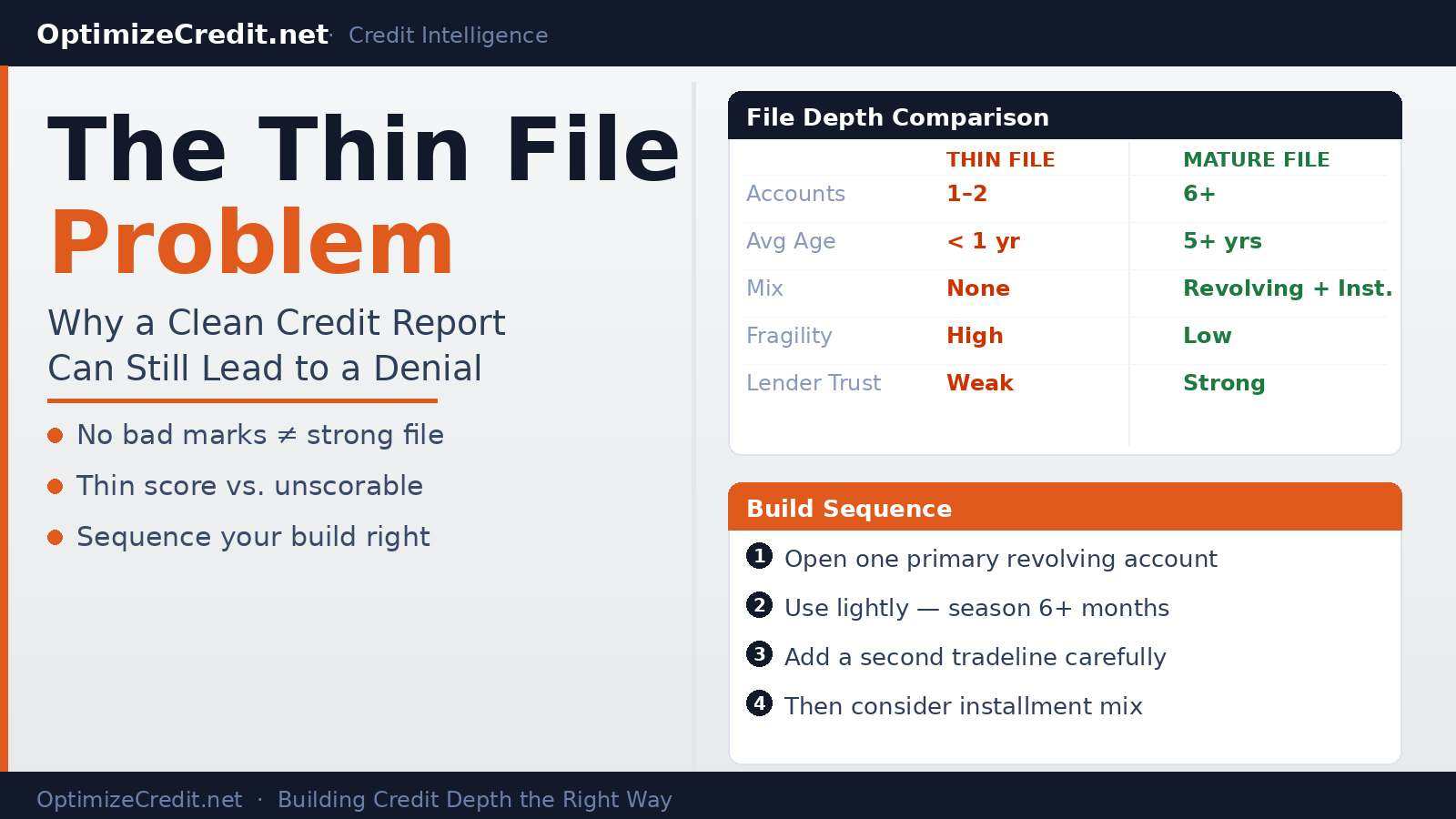

Lenders do not only look for bad behavior. They also look for enough history to trust the score. A spotless file with one young card is not the same as a mature file with years of primary tradelines. To an underwriting model, the first file may look untested, not safe. That is the thin-file problem.

Before assuming your file needs new accounts, run the optimizer to diagnose whether your file is genuinely thin or whether existing accounts are simply missing from one or more bureaus. The distinction matters because the fix for an under-reported file is a dispute, not a new application.

What is the difference between no credit and a thin file?

These are related, but they are not identical.

| Situation | What it means | Why it matters |

|---|---|---|

| No credit / unscorable | Too little data for the model to generate the score needed for that use case | Some lenders cannot evaluate you through normal automated scoring |

| Thin credit / lightly scorable | A score exists, but the file still lacks depth, seasoning, or primary tradelines | You may have a number, but the file can still fail overlays or automated underwriting expectations |

That distinction matters because a consumer can say, "But my app says 720," while the lender sees a file that is still too shallow to trust.

What unscorable credit really means

The phrase unscorable credit does not always mean your report is blank. It can mean the score model the lender needs either cannot generate a score at all, or treats the file as too weak or too new to support a strong automated approval.

That is especially important in mortgage settings, where older FICO models and tri-merge practices create a much stricter standard than a free app score.

Why automated underwriting dislikes thin files

Automated underwriting systems are built to evaluate patterns. Thin files do not give them enough pattern to work with confidently. That can lead to:

- A "refer" or caution-type finding

- Tighter overlays

- A narrower lender pool

- More documentation requests

- A practical denial even when the report looks clean

This is why the distinction between "no bad marks" and "enough proof" matters. Thin files often fail because they have not proven enough yet.

Why a 740 on a thin file is not the same as a 740 on a thick file

A 740 built on one young card is not the same as a 740 built on years of primary accounts, low utilization, installment experience, and clean payment history. One reason is scorecard migration.

Scoring models group consumers into different profile buckets. A borrower can move from a fragile thin-file bucket into a more stable scorecard once the file gains enough age, enough accounts, or enough mix. That migration can matter as much as the numeric score itself. If your file is stuck in a thin-file scorecard, the credit score debugging guide can help you identify what is holding it there.

So the goal is not only "raise the score." It is also "change the file category the score is being computed inside."

Thin files are more fragile than people realize

Thin files tend to be hypersensitive to small disruptions. A thick file may absorb a new inquiry, a utilization spike, or a new account more gracefully. A thin file often cannot.

Common thin-file pressure points:

- One hard inquiry

- One new account

- One card reporting a high balance

- One missed payment

- One account closure

That is why thin-file borrowers should be much more cautious about stacking applications.

What manual underwriting really means

People often hear "manual underwriting exists" and assume it is a universal fallback. It is not. The real-world version is more complicated:

- Some FHA situations may allow manual underwriting

- Many conventional lenders do not want manual-file work

- Even where manual review is technically allowed, many retail lenders simply do not offer it in practice

So the real question is not whether manual underwriting exists somewhere in theory. The real question is whether your target lender actually does it, and whether your file meets that program's documentation standards.

Credit-builder strategies that do not require a tradeline

Not every thin file needs a purchased tradeline. Several organic strategies can build depth effectively:

Secured cards. For many thin-file borrowers, secured cards are still the most practical first step. Look for a card that reports to all three major bureaus, has no unnecessary fees, and offers a real graduation path to unsecured status. A secured card is not glamorous, but it is often the cleanest way to create primary revolving history.

Credit-builder loans. A small credit-builder loan from a credit union or online lender can add installment history. The CFPB's credit-building guide explains how these products work and what to look for. Timing matters: a primary revolving account often comes first, then a builder loan once the revolving tradeline has started seasoning.

Retail store cards. Some retail cards have lower approval thresholds than major bank cards. They report to the bureaus just like any other revolving account. The downside is typically a low limit and high APR, but for the sole purpose of building file depth, they can work.

Becoming an authorized user on a family member's card. This is the organic version of the AU strategy. If a parent or spouse has a well-managed card with long history and low utilization, being added as an authorized user can help build your file without any cost. The same scoring mechanics apply as with purchased tradelines.

The dispute angle: thin files with missing accounts

Some files look thin but are actually under-reported. If you have accounts that are not showing on one or more bureaus, the file appears weaker than it should be. The optimizer can diagnose this by comparing what is on each bureau report against what you actually have open.

Common under-reporting situations:

- A credit union card that only reports to one or two bureaus

- An installment loan that dropped off a bureau prematurely

- An old account that was closed but should still appear in your history

If missing accounts are the issue, a dispute or data-furnisher correction may be more effective than opening new accounts. This is a different problem from a genuinely thin file, and it requires a different solution.

How to build credit depth in the right order

If your file is truly thin, the fix is not to open random accounts. The fix is to build depth in sequence.

- Open one primary revolving account. Usually a secured card or starter unsecured card.

- Use it lightly and predictably. Small charges, clean payments, and stable statement-balance management matter more than volume.

- Let it season. Six months is an important milestone for many FICO contexts, but seasoning is broader than a single date. You want usable age, not just account existence.

- Add a second tradeline carefully. Often another revolving account, sometimes with the same institution if your history is already clean.

- Then think about installment mix. A modest credit-builder loan can help later, but it is usually not the first move.

That sequence is what makes the file stronger instead of simply busier.

Why same-bank expansion can work better than random applications

Once a borrower has one clean primary card, a second tradeline from the same institution can sometimes be easier than starting from zero elsewhere. That is because the lender already has payment history, usage history, risk visibility, and relationship data. For thin-file borrowers, this can be a more controlled way to build depth than spraying applications across multiple banks.

Authorized users can help, but they are not the whole answer

Authorized-user accounts can help thin files, especially when the borrower lacks age or revolving depth. But they have limits:

- Some models or lenders discount them

- Underwriters can see the authorized-user designation

- Some mortgage workflows still care about your own primary tradelines

- Anti-padding logic can limit the boost

So an AU tradeline can be a bridge. It is rarely the whole bridge. A tradeline works best when it addresses a specific diagnosed weakness, not as a substitute for building primary credit history.

Rent reporting and app scores: useful, but limited

Alternative data and app scores can sometimes improve visibility, but they do not automatically solve mortgage readiness. A borrower may have a consumer-facing score in an app, cleaner visibility from rent reporting, and still not have the exact score depth the lender wants. Thin-file borrowers need to be careful not to confuse consumer visibility with underwriting strength.

What to avoid on a thin file

- Opening multiple accounts quickly

- Chasing approvals from several lenders at once

- Carrying high balances to "show activity"

- Closing your first useful tradeline too early

- Treating one AU account as a complete solution

- Assuming one good app score means the file is ready

Conclusion

A thin file is not bad credit. It is incomplete credit. That is why the solution is less about repair and more about sequencing. Build one primary account. Let it season. Add depth carefully. Keep inquiries limited. Use the optimizer to diagnose whether your file is truly thin or under-reported, and choose the right strategy accordingly. Done in the right order, the same clean report that once triggered a denial can become a genuinely lendable file.

Tradelines That Actually Report

We focus on what actually moves credit scores: utilization, account age, and clean reporting. With 500+ successful placements and excellent reviews on TrustPilot ★★★★★, every tradeline is screened for reporting consistency before it is listed.