Why are your scores different on different apps and with different lenders?

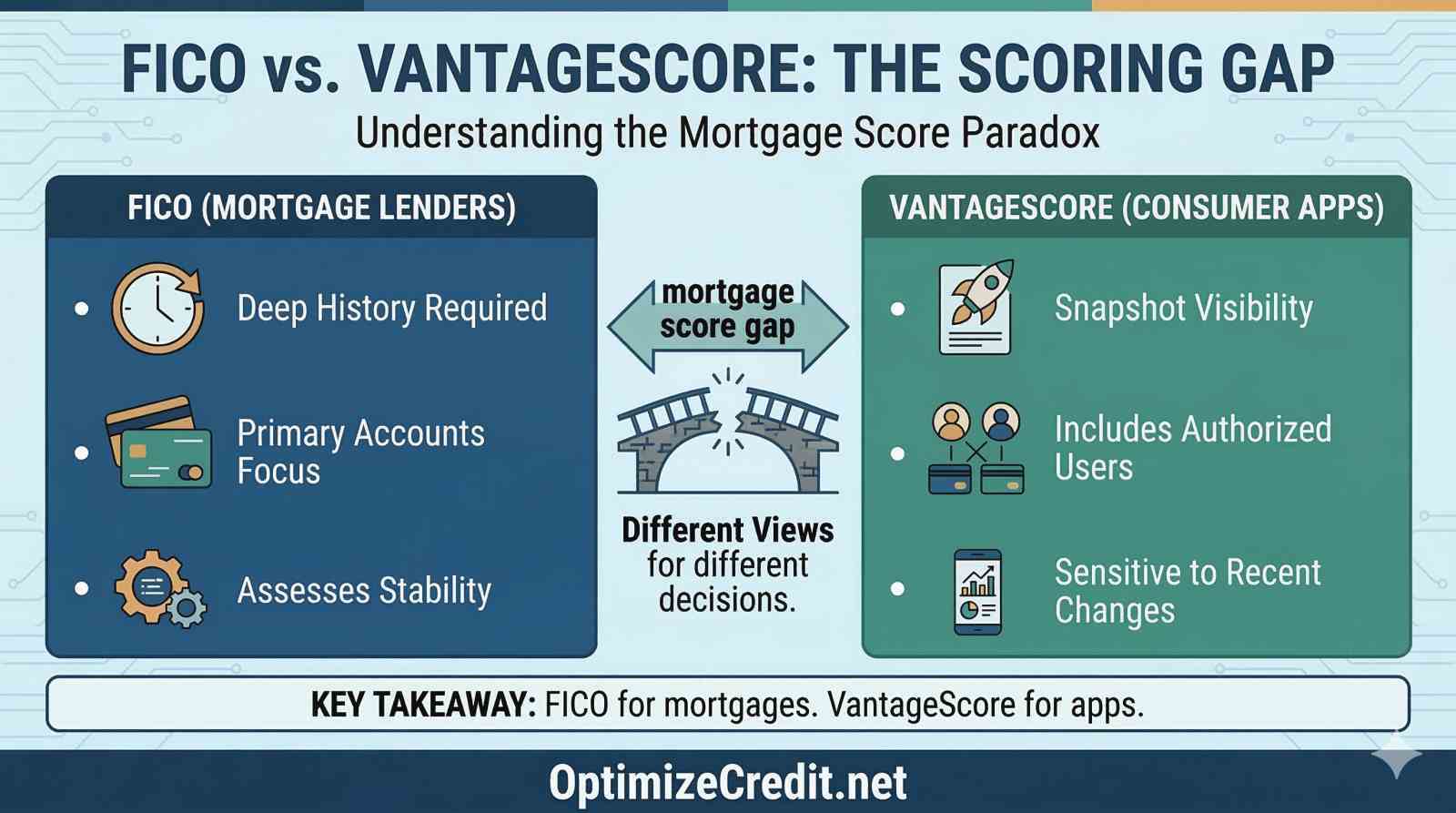

Your credit app score and your lender's score often differ because they are not measuring your file through the same scoring lens. Many consumer apps display VantageScore 3.0 or 4.0, while lenders often rely on FICO scores — and not just one FICO, but specialized versions for mortgages, auto loans, and credit cards. Understanding these scoring mismatches is the only reliable way to predict how your real application is likely to be viewed.

The score you see depends on three things:

- The scoring family

- The version

- The bureau data

If any one of those changes, the number can change. If two or three of them change at once, the gap can become large.

That is why a borrower can look at a healthy app score and still hear a very different number from a lender on the same day.

What is the difference between FICO and VantageScore?

At the highest level, FICO and VantageScore are different scoring families built to predict credit risk. Both use information from your credit report, but they weigh and interpret that information differently.

The important consumer takeaway is not just "they use different formulas." The useful takeaway is that the two systems can respond differently to:

- Utilization

- File depth

- Collections

- Age of accounts

- Recent inquiries

- The amount of usable bureau data

That means one score can be directionally useful while still being the wrong score for your actual lending decision.

FICO vs VantageScore weightings

| Factor | FICO emphasis | VantageScore emphasis | Why the difference matters |

|---|---|---|---|

| Payment history | Very high | Very high | Both punish missed payments, but the exact response can differ by model version |

| Utilization / balances | Major factor | Major factor | FICO often reacts more sharply to revolving balance pressure |

| Length / age of file | Important | Important | Thin or young files can behave very differently across models |

| New credit / inquiries | Meaningful | Meaningful | Thin files can feel inquiry damage more sharply |

| Credit mix / depth | Meaningful | Meaningful | VantageScore can score some thinner profiles earlier than FICO |

The point of this table is not to memorize percentages. The point is to understand that "same file" does not mean "same score."

Why thin files often look stronger in VantageScore

One of the most common mismatches happens with thin files.

VantageScore can often score consumers earlier than FICO. That means a borrower may see an app score and assume they are "score-ready," while a lender either sees no usable FICO score or a meaningfully weaker one. For mortgage prep, that mismatch can be expensive. To understand how this plays out in real lending decisions, see Why Credit Karma Is Not a Mortgage Score.

What score versions do lenders use?

A lender does not simply choose "FICO" in the abstract. Different lending categories pull different FICO score versions.

Examples:

- Mortgage lenders often use classic FICO mortgage versions

- Auto lenders may use FICO Auto Scores

- Credit card issuers may use FICO Bankcard Scores or base FICO versions

This matters because industry-specific FICO versions can use a 250 to 900 range instead of the standard 300 to 850 range. That alone makes casual comparison messy if you do not know which score you are looking at.

The right consumer habit is: ask which model and version the lender uses before you treat a visible score as predictive.

Why bureau data changes the number too

Even if the scoring family stayed the same, your score could still vary because bureaus do not always hold identical information.

Common causes:

- One lender reports to only one or two bureaus

- One bureau updates faster than another

- One bureau still shows an old balance

- One bureau contains a collection the others do not

So "my FICO score" is not really one number. It can be three bureau-specific numbers even before version differences enter the picture.

What is trended data, and why does it matter?

Trended data is one of the biggest concepts consumers hear about but rarely understand.

It does not just look at whether your current balance is high or low. It looks at how you have behaved over time — often across many months.

In simple terms, trended-data models try to distinguish between:

- Transactors: people who regularly pay in full

- Revolvers: people who carry balances month after month

That means one dramatic payoff right before an application may not "erase" a long pattern of revolving behavior in the way a borrower expects. A snapshot-based model and a trended-data model can look at the same current file and tell slightly different stories about risk.

That is why timing tricks alone are less powerful under trended-data logic than under older snapshot-focused assumptions.

Why the same lender can still see different scores for different products

A borrower may assume: "My bank knows me, so it should see one score."

That is not how it works.

A lender may pull one score version for a credit card, another for an auto loan, and a much stricter classic model for a mortgage. So the same person on the same day can be "700-plus" in one context and materially weaker in another.

This is not corruption. It is version selection.

Which score should you actually focus on?

Focus on the score that matches your goal.

If your goal is:

- Mortgage: prioritize the classic mortgage FICO conversation

- Auto loan: understand whether the lender relies on Auto Score versions

- Credit card: know that a bankcard-specific or base FICO may matter more than your app

Use your app score for trend monitoring. Do not use it as a binding underwriting prediction. The optimizer can show you which score version is most relevant to your specific lending goal so you are not debugging the wrong number. For a systematic approach to finding what is actually suppressing your score, see Credit Score Debugging.

That distinction alone can save people from bad timing decisions.

What should consumers do with this information?

- Ask which score family and version the lender uses.

- Pull all three reports before important applications.

- Treat app scores as directional, not definitive.

- Fix the mechanics that most models still care about: payment history, balance pressure, and file stability.

- Remember that version mismatch is real. The score you can see most easily is not always the score that matters most.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →