What score does Credit Karma usually show?

If you are house hunting, the 740 score you see on Credit Karma is effectively a consumer-monitoring score, not the underwriting score that determines whether your mortgage gets priced at a top tier or dropped into a more expensive bracket. Mortgage lenders usually look at classic FICO mortgage models rather than the VantageScore shown in many apps. If you do not understand the middle-score rule and the joint-applicant rule, you can be off by 40 or 50 points at exactly the wrong time.

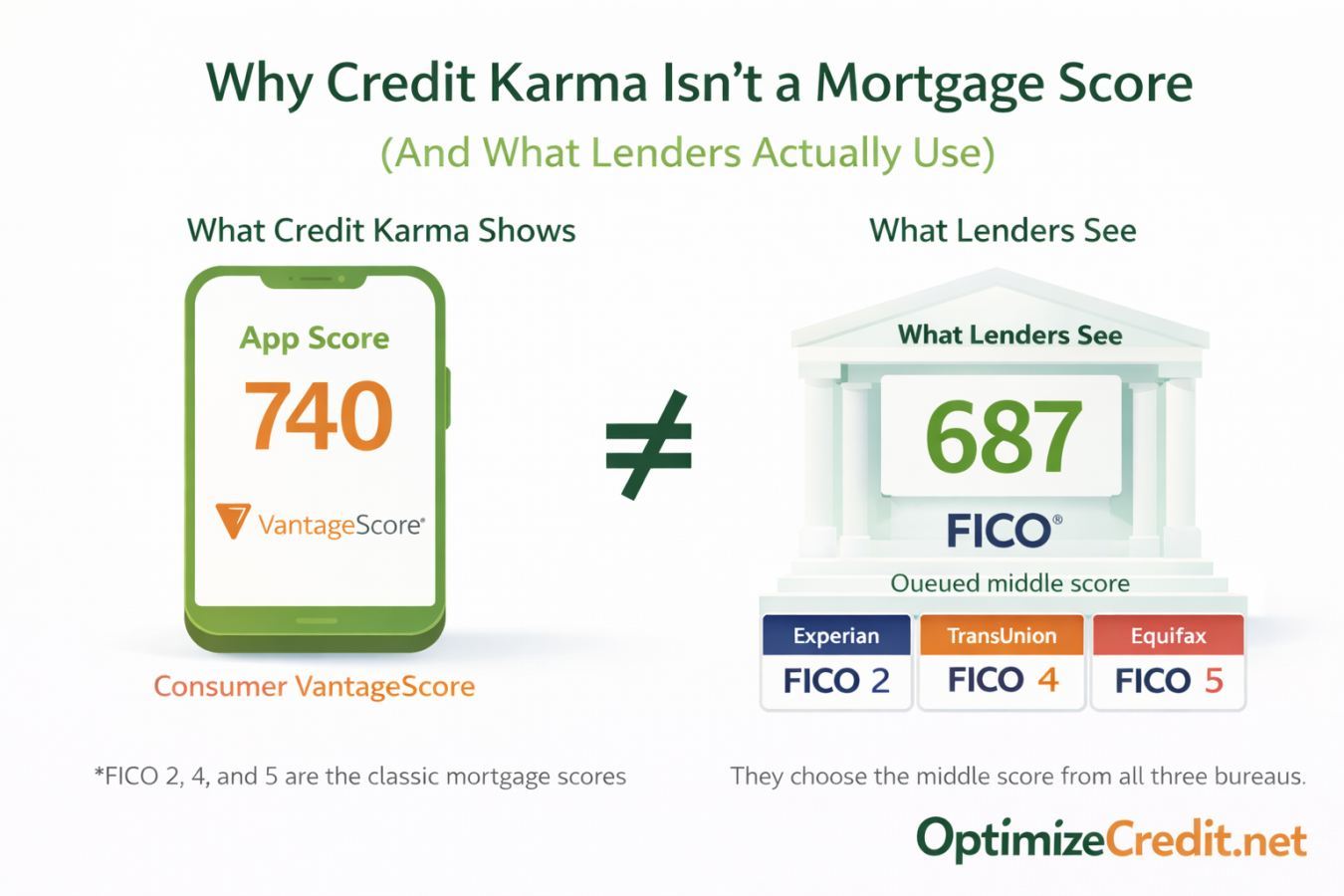

Credit Karma usually shows a VantageScore, not the classic mortgage FICO scores used in most mortgage underwriting. That does not make the score fake. It is a real score generated from your credit report. The problem is that it is usually not the score version your mortgage lender is pricing.

This distinction matters because consumers often treat any visible score as "my credit score." In practice, you have a family of scores. A credit card issuer may look at one FICO version. An auto lender may look at another. A mortgage lender typically uses much older classic FICO versions that are less forgiving about certain negatives and less impressed by the same things that help consumer-app scores. The optimizer shows your estimated FICO mortgage scores alongside free-app scores so you can see the gap before your lender does.

What FICO versions do mortgage lenders usually use?

For conventional mortgage lending, the classic mapping is:

- Experian = FICO Score 2

- TransUnion = FICO Score 4

- Equifax = FICO Score 5

Those are older mortgage-focused models. They are still central because mortgage underwriting standards and secondary-market requirements have historically been built around them. That is why people get surprised. They assume the newest score they can see in an app must also be the score their lender sees. Usually, it is not.

The practical takeaway is simple: if you are preparing for a mortgage, do not optimize only for a consumer-facing app score. Optimize for the score family the lender will actually use. Understanding why FICO and VantageScore differ is the first step.

Why is your mortgage score often lower than your app score?

There are four common reasons:

First, the scoring family is different. VantageScore and FICO do not weigh the same file exactly the same way.

Second, the version is different. Even one FICO version may treat balances, collections, and timing differently from another FICO version.

Third, the bureau data is different. One bureau may show a collection, an old balance, or a missing tradeline that the others do not.

Fourth, the mortgage models are generally less forgiving than the score a borrower sees in a consumer app. A paid collection, a medical collection, a thin file, or even the wrong balance reporting date can create a much bigger gap than the borrower expects.

For some borrowers, the gap is modest. For others, especially thin-file borrowers or people carrying balances, the gap can be large enough to move them into a worse pricing tier. Knowing what the score gap costs in dollars over a 30-year loan makes the stakes concrete.

What is a tri-merge report?

A mortgage lender usually orders a tri-merge report. That is not just a normal consumer credit report. It is a consolidated mortgage credit report pulling together data from all three major bureaus. It is designed for underwriting, not casual monitoring.

The important thing about a tri-merge report is that it can reveal bureau-level issues a borrower never noticed in an app. One bureau may contain a stale balance, one may be missing an account, and one may show a collection that the other two do not. A borrower looking at one convenient app score may think their file is stable when the mortgage report says otherwise.

What is the middle-score rule for a single borrower?

For a single borrower, lenders typically use the middle of the three mortgage FICO scores.

Example:

| Bureau | Model | Score |

|---|---|---|

| Experian | FICO 2 | 705 |

| TransUnion | FICO 4 | 667 |

| Equifax | FICO 5 | 689 |

The lender does not use the highest score of 705. The lender does not use the lowest score of 667. The lender usually uses the middle score of 689. That middle score is often the one that matters for pricing and eligibility.

This is why bureau-specific cleanup matters. If one bureau is dragging badly, the middle score can stay lower than the borrower expects even if another bureau looks fine.

How does the joint-applicant rule work?

This is where many couples get blindsided. For a joint application, the lender generally determines each borrower's middle score first. Then the lender uses the lower of those two middle scores for the loan.

Example:

| Borrower | Score 1 | Score 2 | Score 3 | Middle Score |

|---|---|---|---|---|

| Borrower A | 742 | 731 | 724 | 731 |

| Borrower B | 692 | 661 | 648 | 661 |

The loan is generally priced from 661, not 731. That lower middle score does not just affect whether the weaker borrower qualifies. It can determine the pricing for the entire loan. The stronger borrower's score does not override the weaker borrower's middle score on a standard joint application.

That is why joint-applicant strategy matters. Sometimes the best move is to clean up the weaker profile first. Sometimes it is worth running the qualification math to see whether one borrower should apply alone.

Which mortgage score thresholds matter most?

The exact pricing grid changes by lender, loan type, loan-to-value ratio, and market conditions. But in practice, borrowers should treat these ranges seriously:

| Threshold | Significance |

|---|---|

| 620 | Often the basic conventional threshold |

| 640 / 660 / 680 | Common meaningful pricing steps |

| 700 / 720 | Stronger conventional tiers |

| 740+ | Often where borrowers reach top-tier pricing |

The point is not that one single number solves everything. The point is that small changes can matter. A borrower moving from 659 to 681 is not just gaining 22 points in the abstract. They may be crossing a meaningful underwriting or pricing line.

That is why lowering reported utilization before application can matter so much. It is often one of the fastest legitimate ways to move a middle score.

Why lowering utilization is often the fastest mortgage-prep move

If your goal is a mortgage application in the near future, reducing reported revolving balances is often the cleanest short-term lever. Payment history and derogatories are harder to fix quickly. Utilization is more responsive.

But the key word is reported. Mortgage scores react to the balances that appear on your report, not just the balances you know you paid yesterday. If the card reported before the payment hit the bureau, your mortgage score may still reflect the old number.

That is why utilization work should be tied to statement timing, not just payment timing. The fastest route is often to lower the balance that gets reported on the statement date.

Why your score can still be surprising even when you did everything right

Borrowers often say: I paid my cards down, I have no late payments, Credit Karma says I am fine. All three statements can be true, and the mortgage score can still disappoint.

Common reasons:

- One bureau is missing an account that helps you

- One bureau is still showing an old high balance

- Your file is thin, so the classic mortgage models are harsher

- You applied jointly and the lower borrower's middle score drives pricing

- Your lender pulled a stricter model than the one you assumed mattered

Mortgage prep is not just about good credit habits. It is about aligning your file with the score version that will actually be used.

What about FICO 10T and VantageScore 4.0?

This area causes confusion because people hear that newer models are coming and assume the old system has already changed. The reality is more complicated.

FHFA approved newer models, including FICO 10T and VantageScore 4.0, for future use in the Enterprises' ecosystem, and FHFA has described an ongoing transition process that also includes movement toward bi-merge reporting. But that does not mean every mortgage lender has already switched or that a borrower should assume their next pre-approval will be based on those newer models. For many borrowers, the classic mortgage FICO framework still governs the real underwriting conversation.

So the practical rule is simple: do not optimize for the transition headline. Optimize for the score your actual lender says they will use today.

What should you do before mortgage pre-approval?

- Pull all three reports and compare them line by line.

- Identify your likely mortgage score family, not just your app score.

- Lower reported utilization before application.

- Avoid unnecessary new inquiries or new debt.

- If applying jointly, test the lower middle score issue before you assume both borrowers should be on the loan.

- Give yourself enough time for reporting cycles to catch up.

The biggest avoidable mistake is shopping for homes based on a consumer-app score and only learning your real usable mortgage score after the lender has already run the file.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →