Start with diagnosis, not a purchase

Before evaluating whether a tradeline fits your file, use the optimizer to identify your actual suppressors. A tradeline is a powerful tool when correctly matched to a specific weakness, but it is not a universal solution. The right question is not "how many points does this tradeline give?" The right question is "which weakness in my file is this tradeline supposed to fix?"

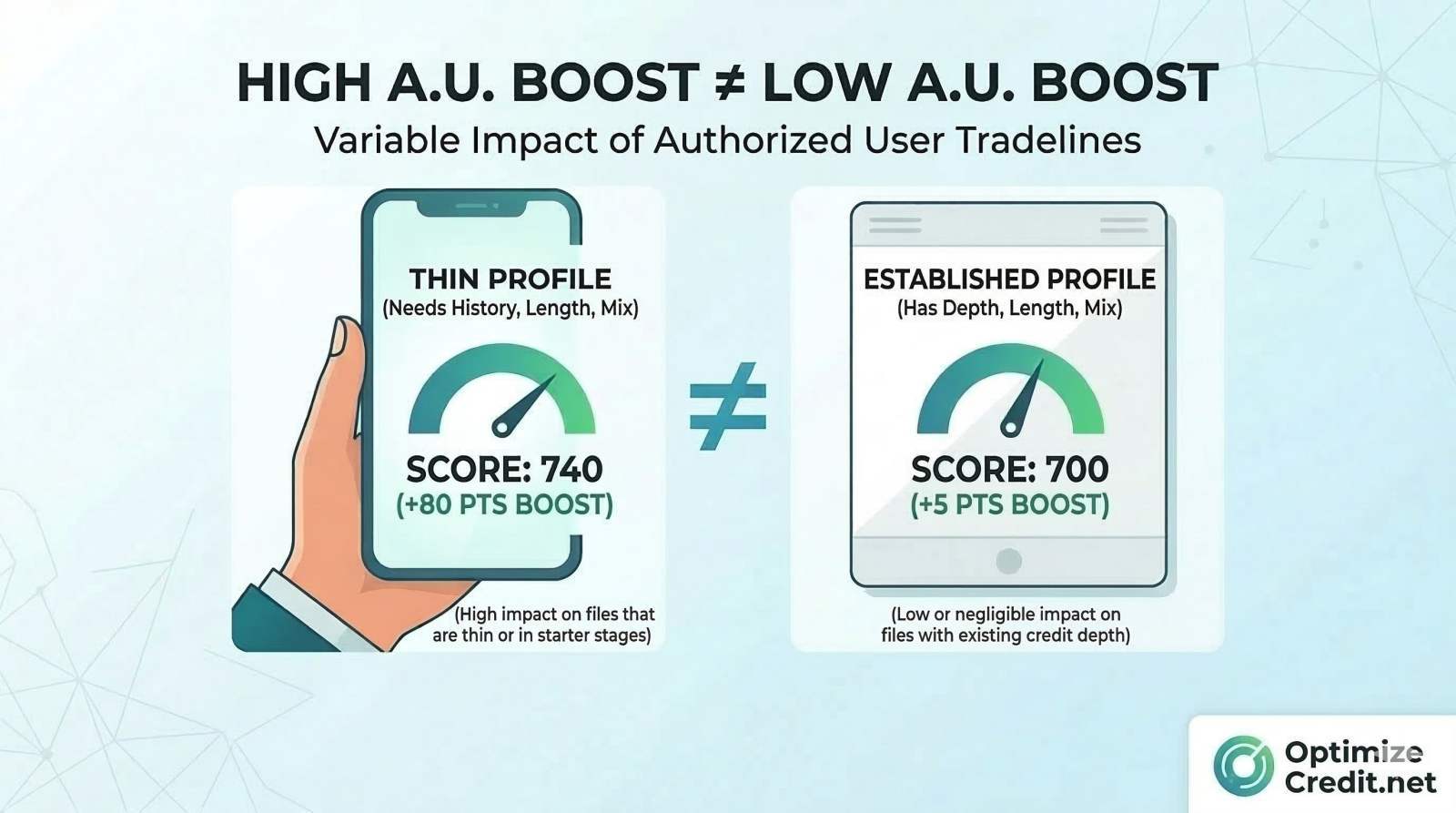

An authorized user tradeline does not provide a fixed point boost. Its value depends on the file depth of the person receiving it. A seasoned, high-limit account can materially improve a thin file or dilute high utilization, but it may do almost nothing for a mature file that already has strong age, low balances, and enough primary accounts.

Do authorized user tradelines actually work?

Yes, they can work. But "work" does not mean the same thing for every file.

If an authorized user account reports to the bureaus, it can influence three areas that often matter a lot in scoring:

- Revolving age

- Available credit

- Utilization math

That is why an authorized user credit score boost is most likely when the receiving file is thin, young, or balance-heavy. If the borrower already has plenty of age and low utilization, there may be very little left for the tradeline to improve.

The same tradeline can feel transformative on one file and irrelevant on another because scoring models react to gaps, not to the tradeline in the abstract.

Why thin files often see the biggest jump

Thin files usually get the largest boost because they are missing foundational ingredients. A borrower with one young credit card and a short history may be weak in several ways at once:

- Not enough revolving depth

- Very short average age

- High utilization sensitivity

- Limited credit limit denominator

Add one older, well-managed authorized user account and several things can improve at once. The average age can rise. The total available credit can increase. The utilization percentage can fall. The file may suddenly look less fragile.

That is why thin-file borrowers often react more strongly to a tradeline than borrowers with already-established primary accounts. If this describes you, the thin file problem guide explains why sparse data creates denial risk even on clean reports.

Why mature files often see little or no boost

A mature file already has its own structure. If the borrower has several primary accounts, long credit age, low utilization, and strong payment history, then the authorized user account may not solve anything important.

That does not mean the tradeline "failed." It means the file did not have much headroom in the categories the tradeline can influence. This is where people get disappointed. They hear a point-gain story from someone else and assume the same result should happen on their file. But a mature file and a thin file are not solving the same problem.

What structural weakness is the tradeline supposed to fix?

Before anyone evaluates a tradeline, they should answer this directly. Is the tradeline meant to fix:

- Lack of age?

- Lack of revolving depth?

- High utilization?

- Thin bureau coverage?

- Weak denominator math from low limits?

If you cannot name the weakness, you are not really evaluating the tradeline. You are gambling on a result.

The most realistic positive use cases are:

- A thin file that needs age and revolving depth

- A balance-heavy file that needs a larger utilization denominator

- A file missing enough high-quality revolving history to stabilize score behavior

The weakest use cases are:

- A mature file that already has multiple old primary tradelines

- A file with serious derogatories where the suppressor is not age or utilization

- A mortgage applicant who still lacks enough primary tradelines to satisfy underwriting comfort

When a tradeline is NOT the answer

A tradeline cannot fix every credit problem. Understanding when it will not help is just as important as knowing when it will.

Derogatory history is the real suppressor. If your score is being held down by late payments, collections, charge-offs, or public records, adding positive tradeline data does not erase those items. The scoring model still sees them. A tradeline may soften the impact slightly by improving other factors, but the derogatory history remains the dominant drag.

Utilization is already low. If your revolving utilization is already under 10 percent across all cards, adding more available credit through a tradeline will not move the needle meaningfully. The file has already optimized that factor.

The file needs primary accounts for underwriting. In mortgage and other manual-review contexts, underwriters want to see that the borrower manages their own accounts. An AU tradeline does not demonstrate independent credit management. If the lender's overlay requires two or three primary tradelines, an AU account does not count toward that requirement.

Too many recent inquiries or new accounts. If the file already has several recent hard pulls or newly opened accounts, adding a tradeline may not overcome the new-account penalty. In some cases, it can even reinforce the appearance of credit-seeking behavior.

The optimizer identifies a different root cause. Sometimes the real issue is a reporting error, a balance that posted at the wrong time, or a closed account dragging down average age. In those cases, a dispute or timing adjustment is the correct fix, not a new tradeline.

Why utilization can make a tradeline look powerful

One of the biggest reasons a tradeline helps is simple math. If the primary account has a large limit and reports a low balance, being added can increase total available credit. That can lower overall utilization. Sometimes the "boost" is not really about age first. It is about the denominator.

Example:

| Before tradeline | After tradeline |

|---|---|

| Total limits: $4,000 | Total limits: $20,000 |

| Reported balances: $1,200 | Reported balances: $1,200 |

| Utilization: 30% | Utilization: 6% |

Even if nothing else changes, the utilization profile may look much healthier. That is why the primary cardholder's behavior matters so much. If they run the card hot, the tradeline can help less or even hurt.

Primary cardholder behavior is not a side issue

A tradeline is only as clean as the account behind it. If the primary cardholder pays on time, keeps balances low, and has a long positive history, the tradeline has a better chance of helping. If the primary cardholder reports high balances, misses payments, or lets the card drift into riskier patterns, the authorized user can inherit those negatives or at least fail to receive the expected benefit.

This is why bureau reporting and card management matter more than marketing claims. An account with a giant limit is not automatically useful if it reports the wrong balance at the wrong time. Experian's guidance on authorized users reinforces the basic rule: AU accounts can help or hurt depending on the condition of the primary account and what actually lands on the report.

Do all issuers report authorized user accounts the same way?

No. Some issuers report authorized user data consistently to all three bureaus. Some do not. Some may be less predictable. And bureau timing can still differ.

That means two consumers added to accounts that look similar on paper may not get the same result if one account reports everywhere and the other does not, one reports quickly and the other lags, or one carries low balances and the other does not.

This is also why timing matters. If someone is trying to qualify for a loan on a deadline, "eventually" is not enough. The account has to report cleanly and in time to matter.

What is scorecard placement, and why does it matter?

A credit scorecard is a profile bucket. Scoring models do not evaluate every borrower in one giant undifferentiated pool. They compare borrowers against similar file types.

In plain terms:

- A thin clean file is judged differently from a mature clean file

- A derogatory file is judged differently from a non-derogatory file

- A file with weak revolving depth is not scored exactly like one with rich revolving history

That is why the same tradeline can produce a meaningful shift for one person and a tiny shift for another. The tradeline may move one borrower into a better comparative bucket, while leaving another borrower in essentially the same scoring neighborhood.

You do not need to know the exact internal scoring architecture to use the concept correctly. You only need to understand the implication: a tradeline matters most when it changes the structure of your file, not just one surface metric.

Do lenders treat authorized user accounts the same way scoring apps do?

Not always. This is a major source of confusion.

A score can include an authorized user account, but an underwriter or lender can still see that the tradeline is tagged as authorized user. In manual underwriting or closer file review, they may decide the account deserves less weight if the borrower has not shown enough primary-account management of their own. Understanding how lenders use bureau scores in practice helps set realistic expectations.

This matters especially in mortgage preparation. A borrower may see a higher score after being added as an authorized user, but the lender can still ask harder questions:

- Does this borrower have enough primary tradelines?

- Is the relationship to the primary cardholder clear?

- Is the profile stable without the authorized user account?

That does not mean authorized user accounts never help. It means the score effect and the underwriting interpretation are not always identical.

When an authorized user tradeline is most likely to help

It is most likely to help when:

- The file is thin

- The borrower lacks old revolving age

- Utilization is high and the tradeline expands total limits

- The primary account is clean, old, and low-balance

- The borrower is not relying on the tradeline as the only sign of creditworthiness

When it may help very little

It may help very little when:

- The file already has enough age and depth

- Utilization is already low

- The file's real suppressor is derogatory history

- The authorized user account reports poorly

- The borrower is applying in a context where underwriters care more about primary tradelines

How to evaluate a tradeline realistically

Ask these questions first:

- Is my file thin, young, or utilization-heavy?

- Am I trying to fix age, denominator math, or revolving depth?

- Does the issuer report authorized user accounts reliably?

- Is the primary cardholder's payment and balance behavior excellent?

- Would my target lender still want stronger primary tradelines from me directly?

If you cannot answer those questions, you are not in position to estimate whether the tradeline is likely to matter. Use the optimizer to diagnose your file first, then decide whether a tradeline addresses the actual weakness it found.

Tradelines That Actually Report

We focus on what actually moves credit scores: utilization, account age, and clean reporting. With 500+ successful placements and excellent reviews on TrustPilot ★★★★★, every tradeline is screened for reporting consistency before it is listed.