Why closing a credit card can hurt your score right away

The Consumer Financial Protection Bureau says closing an existing card can increase your credit utilization ratio and lower your score. That is the most important immediate mechanism to understand.

Under FICO scoring, Amounts Owed is a major category, and myFICO says it accounts for about 30% of the score. That category looks at revolving debt and utilization, not just whether you have debt. Length of Credit History is also important, but it is smaller at about 15%.

So when people close a card and see a score drop, the first question is usually not "Did I lose all that age?" The first question is: Did my available credit shrink while my balances stayed the same?

The utilization math before and after closing

Here is a simple example.

| Card | Limit before closing | Balance | Utilization |

|---|---|---|---|

| Card A | $8,000 | $1,000 | 12.5% |

| Card B | $7,000 | $500 | 7.1% |

| Card C | $5,000 | $0 | 0% |

| Total before closing | $20,000 | $1,500 | 7.5% |

Now assume you close Card C, the unused zero-balance card.

| Card | Limit after closing | Balance | Utilization |

|---|---|---|---|

| Card A | $8,000 | $1,000 | 12.5% |

| Card B | $7,000 | $500 | 7.1% |

| Card C | $0 | $0 | n/a |

| Total after closing | $15,000 | $1,500 | 10.0% |

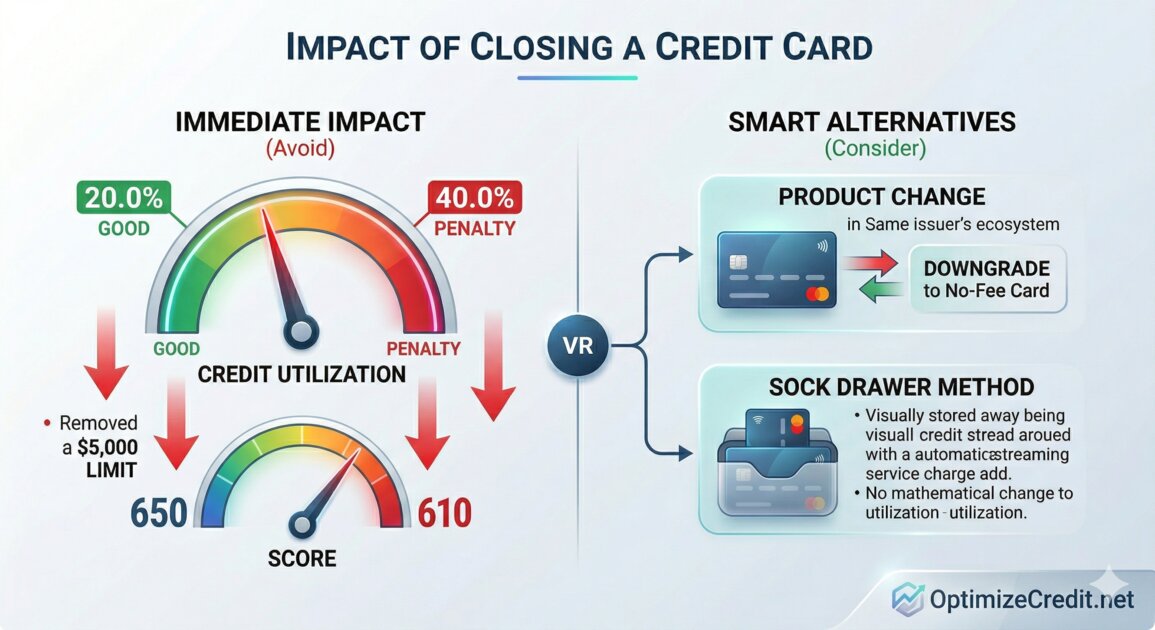

Nothing about your debt improved. Your total balance stayed the same. What changed is the denominator. That is why a zero-balance card can still be helping you. It may be contributing available credit that keeps your utilization lower. The CFPB specifically warns about this effect.

If you want a deeper breakdown of how the percentages work, the most relevant companion read is Utilization Math.

What closing a card does not usually do immediately

This is where a lot of articles get sloppy.

A positive closed account does not usually disappear from your credit reports the moment you close it. Experian says positive closed accounts can stay on your reports for up to 10 years, and continue to affect your scores during that period. Negative information generally follows the normal 7-year reporting timeline.

That means closing a card in good standing does not usually erase its age value overnight. While it remains on your report, it can still contribute to age-related metrics. So for standard FICO framing, the bigger near-term danger is usually utilization, not an instant collapse in average age.

The long-term catch is different: when that positive closed account eventually ages off, your file can lose an older account at that point. So the age issue is real, but it is often delayed rather than immediate.

When closing a credit card actually makes sense

1. The annual fee no longer makes economic sense

If a card charges an annual fee and you are no longer getting enough value from it, closure can be rational. But the best first move is usually to ask for a product change or downgrade to a no-fee version. That can preserve the account line and available credit while removing the fee burden. This is often better than a full closure if the issuer offers it. This is an inference from common issuer practice, not a CFPB/FICO rule.

2. The card fuels overspending

Credit scoring logic and behavioral finance are not the same thing. If one specific card reliably leads to overspending or balance creep, closing it can be the healthier move even if it costs some points. Protecting cash flow and avoiding high-interest revolving debt can matter more than preserving every score advantage. This is strategy, not a scoring fact.

3. Divorce, separation, or legal cleanup

Sometimes the right move is not the highest-scoring move. If an account is joint or tied to a breakup, clarity and liability control may matter more than score optimization. Separation is one of the clearest real-world reasons a closure can make sense.

When closing a credit card is usually a bad idea

1. Right before a mortgage, auto loan, or rental application

If you are close to a major application, stability matters. The CFPB's guidance on utilization is enough to make this a practical rule: avoid optional closures that could change your score right before underwriting.

2. When the card has a large credit limit

A large-limit card can be doing a lot of invisible work by keeping your aggregate utilization lower. Closing a high-limit unused card is often worse than closing a low-limit unused card for that reason. If you are not sure whether your utilization is already in a danger zone, the utilization trap guide covers the most common patterns.

3. When you still carry balances on other cards

This is the classic backfire. Your balances stay the same, but your total available credit drops. That usually makes the utilization math worse immediately.

4. When it is your oldest no-fee revolving card

Even though the age impact may not be immediate, an old no-fee card is often worth preserving unless there is a strong reason to close it. Older accounts help the depth and maturity of your profile over time.

Smarter alternatives to closing

Downgrade to a no-fee version

If the problem is the fee, a downgrade is often the cleanest solution. You may keep the account history and limit while eliminating the annual charge. This is often the best first diagnostic step before considering closure.

Use the sock-drawer strategy

If the card has no fee and you simply do not want to use it, a common strategy is to put it away, add one tiny recurring charge, and set autopay in full. That keeps the account active without turning it into a spending trigger. This is practical guidance, not an official bureau rule.

The diagnostic process before you close any card

Before closing a card, run this checklist:

- Calculate your current aggregate utilization. Add all revolving balances and divide by total revolving limits.

- Recalculate utilization without that card's limit. This is the most important number.

- Check whether the card is one of your oldest or highest-limit accounts. Those are usually the hardest ones to close safely.

- Check your timeline for major applications. If you are within the next few months of a mortgage, auto loan, or rental screening, optional closures are often a bad gamble.

- Ask the issuer about a downgrade first. If the issue is the annual fee, this is often the cleaner path.

- Pay down other balances before making a structural change. Lower balances soften the utilization impact if you still decide to close.

This is the best way to think about the decision: not as "Should I keep fewer cards?" but as "What will happen to my utilization and file stability if this limit disappears?" If something looks off in your score after closing a card, the credit score debugging guide walks through how to isolate the cause.

Bottom line

Closing a credit card can be the right move, but it is often the wrong move for the wrong reason. The immediate score risk is usually higher utilization, not an instant loss of age. Positive closed accounts can stay on your reports for up to 10 years, so age effects are often slower and more nuanced than many articles suggest.

So the best rule is simple: close a card for a real reason—fee burden, liability cleanup, or spending control—not because you think fewer open cards automatically looks better to FICO. That is not how the math works.

For more guides on diagnosing and fixing credit issues, browse the full Troubleshooting hub.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →