Why the FICO Algorithm Cares About Inquiries at All

Credit inquiries are one of the most misunderstood mechanics in the FICO model. Ask five people whether checking your credit damages your score and you will get five different answers — most of them wrong. The reality is straightforward once you understand how the bureaus classify inquiries and how the scoring algorithm actually weighs them.

FICO models are risk-prediction algorithms. They forecast the probability that a consumer will go 90+ days delinquent on a credit obligation within the next 24 months. "New Credit" — the category that includes inquiries — makes up approximately 10% of your total FICO score.

When you apply for credit, the algorithm reads that as credit-seeking behavior. Statistically, consumers who aggressively pursue multiple new credit lines in a short period present higher default risk. The inquiry is the algorithm's first signal of this behavior — a placeholder penalty that precedes the actual new account reporting to the bureaus 30–60 days later.

But the Fair Credit Reporting Act (FCRA) requires that consumers not be penalized for checking their own data or for promotional offers they did not initiate. This legal framework forces the bureaus to separate inquiries into two distinct classifications.

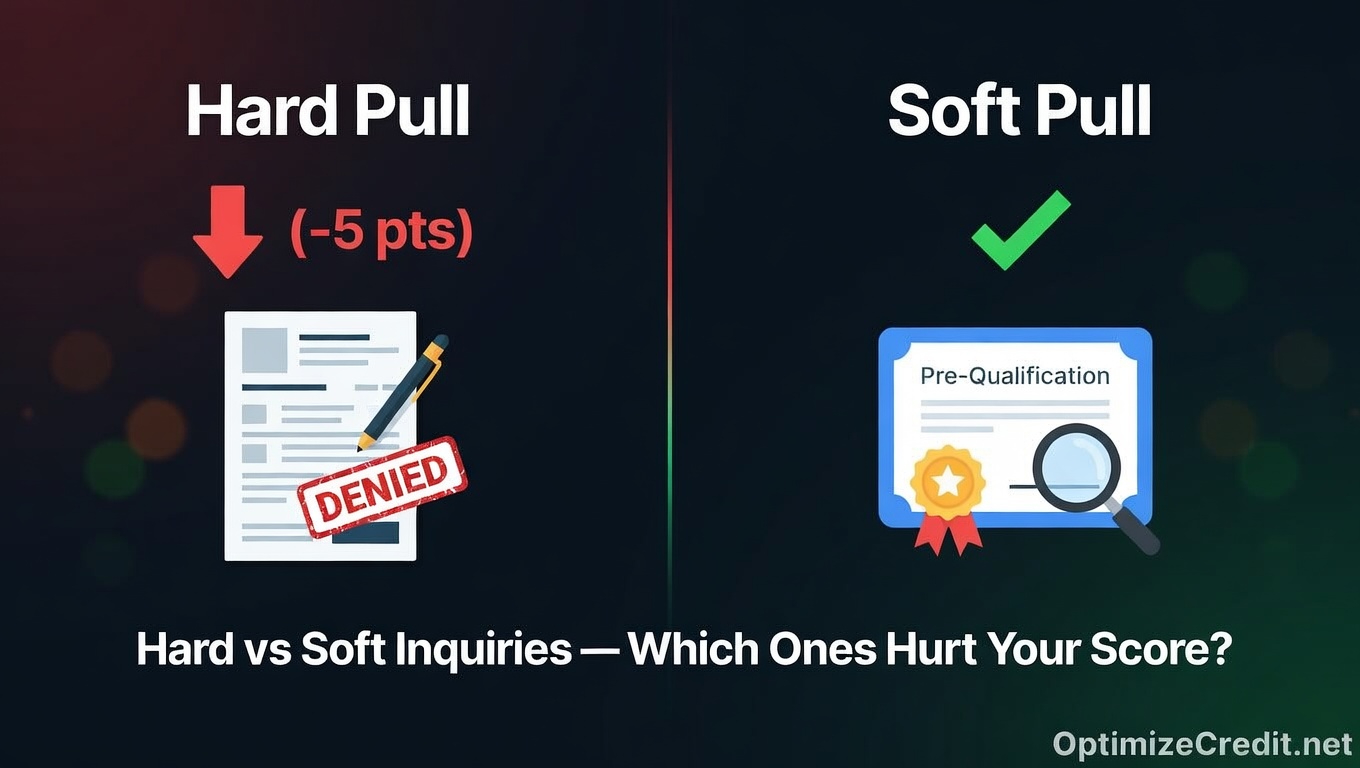

Hard Inquiries: The Only Type That Affects Your Score

A hard inquiry is logged when you authorize a lender to pull your credit report for the purpose of making a lending decision. You initiated a request for credit, and the lender needs your full file to decide whether to approve you and at what terms.

What Triggers a Hard Inquiry

- Credit card applications (approvals and denials both generate a pull)

- Mortgage applications

- Auto loan financing

- Personal loan and student loan applications

- Some apartment rental background checks

- Post-paid cell phone contracts

- Credit limit increase requests (issuer-dependent — always ask before submitting)

The Actual Point Impact

The commonly cited range is 2–5 points per inquiry, but the number is dynamically calculated based on your specific FICO scorecard:

- Thick file (10+ years of history, multiple active accounts, low utilization): A single inquiry might cost 1–3 points. The model sees a long, stable borrowing history and treats one more application as routine.

- Thin file (1–2 accounts, under 2 years of history): That same inquiry could cost 5–10 points. With limited history, each new data point carries disproportionate weight. If this describes your situation, understanding the thin file problem is essential before you apply for anything.

Real-world lender overlay data confirms the pattern: a consumer with a 640 FICO who adds one credit card hard inquiry typically drops to 636–638. The same consumer adding three card inquiries in 10 days might land at 628–632.

The 12-Month Scoring Window and 24-Month Reporting Window

Hard inquiries follow a strict data-aging lifecycle:

- Months 1–12: The inquiry actively factors into your FICO score. This is when the 2–5 point penalty applies.

- Months 13–24: The inquiry remains visible on your credit report, but FICO assigns it a mathematical weight of zero. Your score automatically rebounds from the initial deduction.

- After 24 months: The bureaus purge the inquiry from your file entirely under FCRA requirements.

This means the score damage from a hard inquiry is self-healing. Unlike a late payment that scars your file for seven years, an inquiry's scoring impact expires after 12 months and disappears from your report after 24.

Soft Inquiries: Zero Score Impact

A soft inquiry occurs when your credit file is accessed for a purpose other than a direct lending decision you initiated. The FICO algorithm is programmed to completely ignore them. No scoring model — FICO, VantageScore, or any custom lender scorecard — deducts points for soft pulls.

Lenders pulling your file for underwriting cannot even see your soft inquiries. They are only visible to you on your consumer disclosure report.

Common Soft Inquiry Triggers

- Self-checks: Pulling your own report through AnnualCreditReport.com, Credit Karma, or your bank's free score tool

- Pre-approval offers: When a card issuer mails you a "pre-qualified" offer, they ran a soft pull to prospect you — you did not apply

- Account reviews: Your existing creditors periodically soft-pull your file to manage risk, adjust limits, or consider product upgrades

- Employment background checks: Employer screenings use a modified version of your report via soft inquiry

- Insurance underwriting: Auto and homeowners insurance companies checking credit-based insurance scores for premium calculations

The math on soft inquiries: 0 points lost. Always.

Rate Shopping: FICO's Deduplication Algorithm

One of the most destructive credit myths is that shopping for the best mortgage or auto rate will wreck your score. The opposite is true — FICO's algorithm has built-in deduplication logic specifically designed to protect rate shoppers.

How the Deduplication Window Works

When FICO detects multiple hard inquiries from mortgage lenders, auto lenders, or student loan providers within a defined window, it bundles them and counts them as a single inquiry for scoring purposes. The window size depends on which scoring model is being used:

| Scoring Model | Rate Shopping Window | Notes |

|---|---|---|

| FICO 8 and FICO 9 | 45 days | Used by most credit card issuers and auto lenders |

| Older FICO models | 14 days | Still mandated by Fannie Mae/Freddie Mac for mortgage underwriting |

| VantageScore 4.0 | 14 days | Applies across all loan types |

What Rate Shopping Looks Like in Practice

You apply with four mortgage lenders over three weeks. Your credit report shows four hard inquiries from mortgage companies. But FICO's algorithm sees four inquiries of the same loan type within the 45-day window and scores them as one. Total score impact: 2–5 points, not 8–20.

You can verify these deduplication guidelines directly through myFICO.

The Critical Exception: Credit Cards

Rate shopping protection does not apply to credit card applications. Each credit card application generates its own independently scored hard inquiry. FICO treats card applications differently because each card is a distinct product — there is no natural "shopping" behavior the way there is with mortgage or auto rates.

This distinction is the single most important thing to understand if you are preparing for a mortgage.

When Hard Inquiries Actually Become a Problem

Despite being the smallest FICO factor, there are specific scenarios where inquiry management becomes strategically critical.

Before a Mortgage Application

Mortgage underwriting is the most inquiry-sensitive lending scenario for two reasons:

Underwriters review raw reports, not just scores. Even if FICO deduplicates your rate-shopping pulls, a human underwriter sees every inquiry. Recent credit card inquiries in particular will trigger a required Letter of Explanation (LOE) under Fannie Mae/Freddie Mac guidelines.

New accounts create a double hit. A hard pull that also opens a new account triggers two separate penalties inside the model: the inquiry itself (new credit factor) plus the new account lowering your average age of accounts (length of history factor). This compounds the damage beyond what the inquiry alone would cause.

The practical rule: Stop applying for credit cards, personal loans, or store cards at least 6 months before you plan to apply for a mortgage. Rate shopping for the mortgage itself within the deduplication window is fine — that is what it is designed for.

On a Thin File

If you only have two or three accounts and limited history, every hard pull represents a larger share of your "new credit" activity. Be selective — apply only when you have researched approval odds and the product genuinely serves your plan.

During Active Rebuilding

If you are recovering from collections or charge-offs with a score in the 550–620 range, unnecessary inquiries create drag. Each application needs to be strategic.

Inquiries in Context: The Full FICO Weighting

To keep inquiry anxiety in perspective, here is how FICO distributes scoring weight across all five factors:

| Factor | Weight | What It Measures |

|---|---|---|

| Payment history | 35% | On-time vs. late payments |

| Amounts owed | 30% | Utilization ratios, total balances |

| Length of credit history | 15% | Age of oldest/newest accounts, average age |

| Credit mix | 10% | Variety of account types (revolving, installment, mortgage) |

| New credit | 10% | Recent inquiries and newly opened accounts |

Notice that "new credit" is not just inquiries — it also includes recently opened accounts. The inquiry itself is a fraction of that 10% slice. A single late payment can cost 60–100+ points. A hard inquiry costs 2–5. The math is not close.

Common Myths, Corrected

"Checking your own credit hurts your score." False. Self-checks are always soft inquiries. Check daily if you want.

"I can dispute legitimate inquiries to get them removed." No. If you applied for a card and the issuer pulled your report, that inquiry is accurate and will not be removed. Only unauthorized pulls — where a lender accessed your file without permissible purpose under the FCRA — qualify for dispute and removal.

"All inquiries within 30 days are bundled together." Only mortgage, auto, and student loan inquiries get rate-shopping deduplication. Credit card, personal loan, and retail card inquiries are always counted individually.

"Hard inquiries destroy your credit." At 10% weighting (shared with new accounts), inquiries are the least impactful scoring factor. A 2–5 point dip recovers within 12 months. A 30-day late payment leaves a mark for seven years.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →