Divorce by itself does not directly damage your credit score. What damages credit is the joint and co-signed debt around the divorce, the missed payments your ex may make on accounts that still legally belong to both of you, the utilization spikes that follow a closed account, and the refinance friction that keeps your name on a loan you no longer want.

That distinction matters. According to Experian's divorce and credit guidance, divorce does not directly affect a credit score. Damage shows up indirectly through joint accounts, late payments, account closures, utilization shifts, and new credit applications around the separation. Treat the rebuild like a debugging problem, not a punishment.

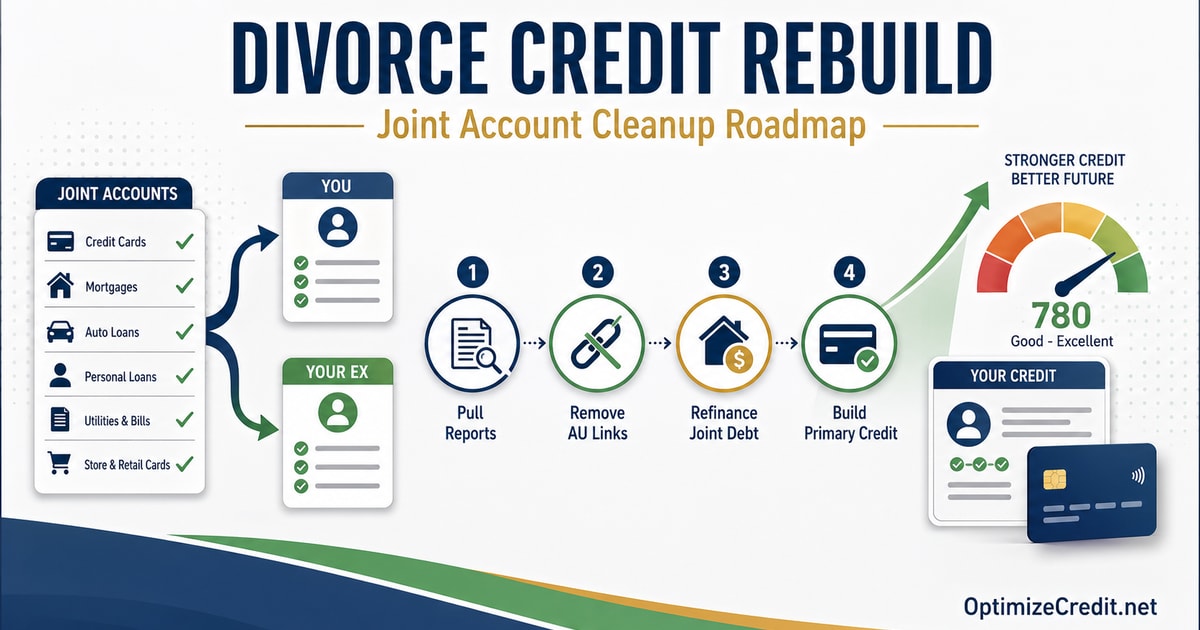

The TL;DR rebuild sequence

- Pull all three credit reports and build a complete account inventory.

- List every joint account, co-signed loan, and authorized user link by bureau.

- Refinance, pay off, or close the joint accounts the divorce assigns to either spouse.

- Remove yourself from authorized user accounts that no longer belong to you.

- Dispute ex-spouse missed payments only when they are factually inaccurate.

- Manage utilization on remaining cards before the statement closes.

- Rebuild independent primary credit slowly with one or two safe accounts.

That is the roadmap. The rest of this article walks through why each step matters and where people go wrong.

Why divorce can punish a credit file even though divorce itself is not scored

Credit scores do not have a marital status field. A credit report does not flag you as divorced. So why does the file so often get hit?

Because the financial structure of marriage usually leaves a long tail of shared liability. Joint credit cards, co-signed auto loans, mortgages with both names, authorized user accounts, and shared household bills all stay attached to one or both files until something changes them. The divorce itself does not move that data. The plumbing underneath it does.

The most common indirect damage paths are:

- One spouse stops paying a joint account and the late payment lands on both files.

- A joint account is closed, available limits drop, and utilization on remaining cards spikes.

- A refinance is supposed to remove one spouse but the lender does not approve.

- An authorized user link still appears on the file and either helps or hurts the score.

- New credit applications during separation generate a wave of hard inquiries.

- Income drops or shifts and reported balances start running closer to the limit.

Each one of these is a normal credit mechanic. None of them is unique to divorce. The reason divorce is dangerous is that they often happen at the same time.

The most important warning: a divorce decree is not a creditor release

This is the single biggest misunderstanding in post-divorce credit work.

The CFPB explains that a debt collector or creditor can generally still contact you about a debt if your name is on the original loan agreement. A divorce decree or property settlement is between you and your ex-spouse. It does not automatically change the contract you signed with the bank. The lender keeps the right to collect from anyone whose name is on the account.

That means a decree saying "the auto loan is solely the husband's responsibility" does not, by itself:

- Remove your name from the loan

- Stop the lender from reporting late payments to your credit file

- Prevent the lender from suing you for the balance if your ex stops paying

- Stop the account from showing on your credit report

To actually be removed from the obligation, the account usually has to be refinanced into your ex's name alone, paid off, or formally released by the creditor in writing (which is rare). Coordinate with your divorce attorney on the legal language, but do not assume the legal language replaces the lender contract. From a credit reporting standpoint, your name stays on the loan until the loan goes away or the lender agrees in writing to take you off.

Step 1: Pull all three reports and build a divorce-credit account inventory

Start with a clean three-bureau pull from AnnualCreditReport.com, the federally authorized source for free reports from Equifax, Experian, and TransUnion. Do not rely on one consumer app or one bureau dashboard. Account-level details often differ between bureaus.

For each open account, write down:

- The account name and last four digits

- Whether you are the primary, joint, or authorized user

- The current balance and credit limit (or original loan amount)

- The reported payment history

- Whether the account appears on all three bureaus

- Which spouse the divorce settlement assigns to that debt

This inventory is the foundation for every later step. Without it, you are guessing about which accounts still expose you and which ones do not. The credit score debugging framework is the parent workflow here. Divorce is just a specific debugging case where shared responsibility is the suppressor.

Divorce credit debugging checklist

- Are there any joint accounts you forgot about, like store cards or older auto loans?

- Are there authorized user links that should be removed?

- Are there accounts that should not be on your file at all (mixed file)?

- Are there late payments that occurred after separation but are reported on a joint account?

- Are there addresses on the file that belong only to your ex?

- Are there any inquiries you did not authorize?

- Are the balances and credit limits accurate as of the most recent statement?

- Has any joint account already been closed by the issuer without your knowledge?

Step 2: Treat joint credit cards as full-balance liability

The CFPB also confirms that joint credit card accounts affect both account holders' credit. Each joint holder can be held responsible for the full balance, regardless of who actually made the charges.

For divorce planning, that means:

- If your ex runs the joint card up after separation, your file can be hit.

- If the joint card has a missed payment, both files can show the late.

- If the joint card stays open with both names, both spouses keep some risk.

The cleanest moves are usually one of:

- Pay the joint card off and close it (with the understanding that closing it can spike utilization on the remaining cards).

- Refinance the balance onto one spouse's individual card via a balance transfer.

- Convert the account to a single name if the issuer allows it, which most do not without effectively closing and reopening.

"We will leave it open and trust each other" is not a credit plan. It works until it does not, and the file pays for the failure mode.

Step 3: Authorized user accounts after divorce -- when to remove first

Authorized user accounts are a special case because they are not legal liability, but they do affect both files.

If you were an authorized user on your spouse's card during the marriage, that card can still be helping or hurting your credit. myFICO confirms that authorized user accounts can appear on credit reports and influence FICO scores. Primary accounts carry more weight when scoring models look at independent credit management, but the AU account is still part of the file. Experian's divorce guidance also notes that authorized users can request removal directly from the issuer.

The decision after divorce comes down to three scenarios:

| Scenario | Action | Why |

|---|---|---|

| The ex's card is well-managed and supporting your file | Decide whether to keep the AU link or remove it | The score support may be useful, but the link gives your ex influence over your file |

| The ex's card has high utilization or late payments | Request removal immediately | The AU link is dragging your score down and you cannot control the host account |

| You do not know what shape the ex's card is in | Pull the report and check before deciding | Decisions made without inventory are coin flips |

To actually remove yourself, contact the card issuer directly and request removal as the authorized user. That is faster and more reliable than asking your ex to remove you, and it does not depend on cooperation.

Step 4: Disputing an ex-spouse missed payment on a joint or AU account

This is where many people get the law wrong.

If a payment was actually missed on an account you are legally on (joint, co-signed, or in some cases authorized user), the late payment is not inaccurate just because your ex was supposed to pay it. The credit reporting system does not enforce divorce decrees. It reports what happened on the account.

You can file a dispute when:

- The payment is reported on the wrong account

- The payment was actually made on time but reported late

- The reporting period is wrong

- You were already removed from the account before the late payment

- The account was never yours (mixed file)

You generally cannot get a legitimate late payment removed simply because your ex was supposed to pay it under the decree. That is a legal claim against your ex, not a credit reporting dispute.

For the actual mechanics of when a payment really posted late versus when it simply has not reported yet, see statement date vs bureau update. Timing matters before you decide an item is wrong.

Step 5: Manage the utilization spike before it lands

One of the quietest credit hits in divorce is the utilization shift after a joint account closes.

Suppose you and your spouse had a joint card with a $15,000 limit and a $3,000 balance, plus your own personal card with a $5,000 limit and a $2,000 balance. Your overall reported utilization is roughly 25% across $20,000 of total revolving credit. If the joint card is paid off and closed, you may suddenly have a $2,000 balance on $5,000 of remaining limit -- 40% utilization on a single card. Same actual debt. Higher reported utilization. Lower score.

This is the same trap covered in the utilization trap, just triggered by a divorce-driven closure instead of a payoff. The fix is the same: control what gets reported on the statement closing date, not what you owe in raw dollars.

Before any joint account closes, consider:

- Paying down individual-card balances so the post-closure utilization stays clean

- Asking for a soft-pull credit limit increase on a card you are keeping

- Letting one card report a small balance and the rest report zero

- Avoiding new applications that would add hard inquiries during the transition

Step 6: Rebuild your independent credit on purpose

If your credit during marriage was largely supported by joint accounts and authorized user links, the file may suddenly look thin once those are removed. That is normal. The fix is not to chase quick score points; it is to rebuild the file on accounts that are clearly yours.

The two starting tools for almost everyone in this situation are:

- One personal credit card in your name only, used lightly and paid off before the statement closes

- A small installment account, often a credit-builder loan or a savings-secured personal loan

If you are starting closer to a thin or rebuild file, the building credit from zero framework still applies after divorce. Only the starting point is different. The secured cards vs credit-builder loans comparison explains which tool to lead with based on whether your file needs revolving control or installment depth.

Avoid the post-divorce credit panic move: opening five new accounts in a single month to "rebuild fast." That creates inquiry noise, drops average account age, and can lower the score before any of the new accounts have time to help.

Step 7: When refinancing the marital home or auto loan

Refinance is the only reliable way to remove your name from a joint mortgage or auto loan when the divorce decree assigns the asset to your ex.

Until that refinance closes, your file is still on the loan. That is why the timing matters:

- Late payments before the refinance still hit both files.

- The DTI on your file still includes the loan, even though the decree says it is the ex's.

- If you are also trying to qualify for a new mortgage, the old one may be counted against you.

If your ex cannot qualify for the refinance, the loan often has to be sold or paid off. Pretending the decree alone solved the problem is the most expensive mistake in this whole sequence. Coordinate the credit timing with your divorce attorney so the legal obligations and the credit reporting line up.

When authorized user tradelines can help after divorce -- and when they should not be the first move

This is the question many divorced clients ask first. The honest answer is that authorized user tradelines can help, but only after the file is actually clean.

An authorized user tradeline can help when:

- The joint accounts have already been closed or refinanced

- You have already been removed from the ex's accounts that were dragging the file

- Disputed errors have been corrected

- Utilization is managed

- The file is now thin, not damaged, and needs additional age or depth before a major purchase

An authorized user tradeline should not be the first move when:

- You still have unresolved missed payments on joint accounts

- Joint accounts still appear on the file and have not been refinanced

- The file is still mid-divorce and the inventory is not stable

- The real problem is income or utilization that a borrowed account cannot fix

The order is: clean the file, build primary credit, then optimize. AU tradelines belong in the optimization phase. They are not a shortcut around an unresolved joint account.

The 12-month divorce credit roadmap

| Timeframe | Main actions | What you are trying to fix |

|---|---|---|

| Months 0 to 1 | Pull all three reports. Build the joint account inventory. Identify authorized user links. Coordinate with your divorce attorney on legal obligations. | Stop guessing about what is on the file |

| Months 1 to 3 | Refinance, pay off, or close the joint accounts the decree assigns. Remove yourself from AU accounts that no longer help. Dispute factual errors only. | Cut shared liability and bad data |

| Months 3 to 6 | Manage utilization on remaining cards before each statement close. Ask for soft-pull credit limit increases where appropriate. Verify everything reported correctly. | Stabilize the post-closure file |

| Months 6 to 12 | Add one or two clean primary accounts in your name only. Keep payments perfect. Rebuild account depth. Consider an AU tradeline only if the file is otherwise stable. | Rebuild independent credit |

How the Credit Optimizer fits the divorce rebuild

The Credit Optimizer is the diagnostic step in this process. It is not a promise to undo a refinance you have not done or remove a legitimate late payment. For a divorce file, it helps identify which suppressor is actually moving the score: an unresolved joint account, an authorized user link, a utilization spike on the remaining cards, a thin file after the joints closed, or reporting errors that crept in during the transition.

That ordering matters because divorce files often have several issues at once. If you start with a tradeline before the joint cards are off, the score may not move. If you start with disputes before the inventory is built, you can dispute the wrong items. The optimizer's job is to put the levers in the right order.

For a focused rebuild plan based on your actual file, upload your three-bureau report to OptimizeCredit.net's free AI analyzer.

What not to do during a divorce credit rebuild

- Do not assume the divorce decree by itself has removed you from a loan. The lender contract still applies.

- Do not close every joint account on the same day without checking how it changes utilization.

- Do not open five new accounts in the first month after separation. The inquiry noise hurts.

- Do not dispute legitimate late payments using "the decree said it was my ex's" reasoning. That argument loses.

- Do not add an authorized user tradeline before the existing joint accounts are resolved. You are layering optimization on top of an unstable file.

- Do not skip the three-bureau pull. One bureau can show a clean file while another still shows the old joint debt.

If you are looking for a faster pre-purchase variation of this work -- for example, you have a mortgage application 90 days out and divorce just closed -- see how to boost a credit score fast for the short-window version of these same mechanics.

Bottom line

Divorce does not directly damage your credit, but it removes the financial cushion that hid a lot of shared-liability mechanics. Joint accounts, co-signed loans, authorized user links, and utilization shifts all become individual problems instead of household ones.

The rebuild works when you treat it like a system: pull the inventory, separate or refinance the joint accounts, remove the authorized user links you do not want, manage the utilization shift, dispute only the actual errors, then rebuild primary credit on purpose. Optimization tools like authorized user tradelines belong at the end of that sequence, not the beginning. And no part of this replaces the legal coordination with your divorce attorney on who is responsible for what under the decree.

The credit will not move all at once. But once the joint accounts are off, the late payments stop, and the new primary credit starts reporting clean, the file usually behaves like a normal individual file again -- sometimes within a year, sometimes longer, depending on what was on the file going in.

Get Your Personalized Credit Roadmap

Upload your credit report and our Credit Analyzer identifies exactly what is holding your score back and gives you a step-by-step 90-day plan to reach 740+.

Trusted by 500+ successful placements and excellent reviews on TrustPilot ★★★★★

Analyze My Credit Free →