Buying tradelines can help, but only if you approach it like a buyer’s guide problem—not like a hype-driven shortcut.

That is where most people go wrong. They start by shopping inventory instead of diagnosing their credit file. Then they overpay for age they do not need, buy from a weak broker, or expect a score result that was never realistic for their profile.

A tradeline is just one piece of credit history. It can help thin files a lot, help established files a little, and help heavily damaged files much less than sales pages imply. The real value comes from buying the right type of tradeline, from the right provider, at the right time.

This guide focuses on what most competitors skip: realistic pricing, how to compare tradeline companies, how long posting really takes, when one tradeline is enough, when a package makes sense, and how to spot scam behavior before you send sensitive identity documents.

If you want the legal background first, read are tradelines legal. If you want the score-impact mechanics, see how AU tradelines affect your credit score.

Step 1: Check your credit profile first

Do not start by buying a tradeline. Start by checking your credit reports and score drivers.

You need to know:

- Is your file thin, average, or already mature?

- Is the main problem age of accounts, utilization, or lack of revolving depth?

- Are negative items dominating the file?

- Are you preparing for a mortgage, auto loan, rental screening, or general rebuilding?

This is the most important step because tradelines are not equally useful for every profile.

Thin files often benefit the most. If you have little or no revolving history, one clean, aged authorized-user account can noticeably change how your file looks. But if your report already has multiple accounts and the main problem is collections, charge-offs, or recent late payments, a tradeline may do much less than you expect.

A tradeline adds positive data. It does not erase bad data.

Step 2: Decide what you actually need

Most buyers say they want “the best tradeline.” That is too vague to be useful.

A better question is: what feature is missing from my file?

Usually buyers need one or more of these:

- More age

- More available credit

- Lower overall utilization

- More revolving-account depth

- A cleaner-looking file for short-term application prep

That leads to smarter buying.

If your file is thin or new, age usually matters a lot. If your balances are too high, limit and utilization may matter more than extreme age. If your report already has several aged accounts, buying a very old premium tradeline may not justify the price.

This is also why many buyers overspend. They chase the oldest, highest-limit line because it sounds strongest, even when a mid-tier line would have solved the actual problem for less money. For more on how utilization math works, see utilization math explained.

Step 3: Understand realistic tradeline pricing

Pricing in this market varies a lot, but realistic buyer expectations are much wider than many sales pages suggest.

A common market-style range is roughly $200 to $3,000+ per tradeline depending on age, limit, issuer, and broker markup. A three-line package around the mid-market often lands near $2,000, though premium packages can be much higher.

Pricing by age tier

| Tradeline Age Tier | Typical Market-Style Price |

|---|---|

| 2–3 years | $295 |

| 5–7 years | $600 |

| 10+ years | $1,000+ |

| 15+ years | $1,500+ |

These are directional buyer-guide ranges, not fixed industry rules.

What many buyers miss is that pricing is not the same thing as usefulness. A 15+ year line may be excellent, but it is not automatically the best buy for every file. A strong 5–7 year line with clean history and low utilization can be the better value if your file just needs a practical boost.

Step 4: Compare tradeline companies like a real buyer

There is no single “most legit” provider for everyone. Inventory changes. Reporting performance changes. Sellers come and go. The better question is how to compare tradeline companies in a disciplined way.

Start by checking whether the company has:

- A real business domain

- A clear website with business identity

- A written contract

- A stated posting or refund policy

- Visible customer-service channels

- A public business footprint such as BBB presence

- Realistic language rather than guaranteed outcomes

A strong company usually sounds less dramatic, not more. It explains timing. It explains what can go wrong. It explains what a tradeline will not fix.

That is one reason most buyer guides on the internet are weak. Some are just sales pages wearing a blog disguise. Others are skeptical but not useful. The best buyer guide is one that helps you buy less stupidly, not one that simply tells you to buy or not buy.

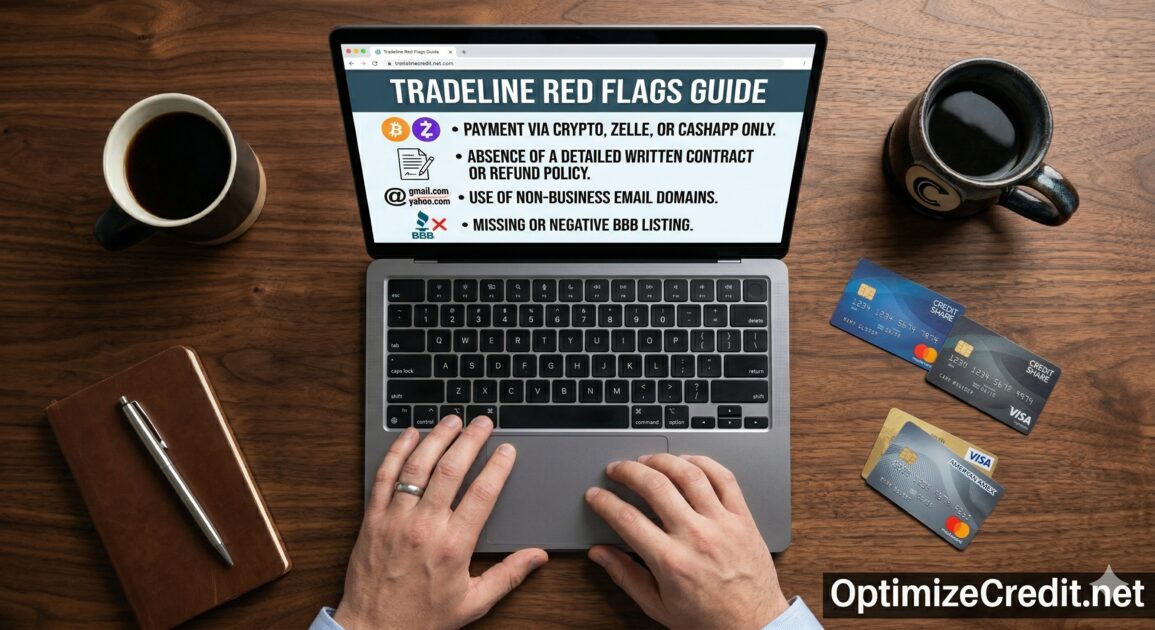

Step 5: Use a scam red-flags checklist

This is where many buyers get burned.

Red flags checklist

- Cash App, crypto, Bitcoin, or wire-only payment

- No written contract

- No business email domain

- No real website

- No BBB listing or public business footprint

- No reporting or refund policy

- Guaranteed point increases

- Guaranteed approvals

- Pressure to buy immediately

- No explanation of statement dates

- Wants ID and SSN before answering basic questions

- Operates mainly through DMs or anonymous chat

None of these alone proves a company is fraudulent, but several together should stop the transaction.

A safer provider should be willing to explain what personal information is needed, why it is needed, when the account is expected to report, what happens if it misses that cycle, how long the tradeline usually stays on file, and what happens if the tradeline does not post.

Step 6: Know what documents you usually need

Yes, identity risk is real in this market.

Many providers require your Social Security number and a copy of your driver’s license or similar government ID so the authorized-user addition matches the correct file. That is one reason this should never feel casual.

Before sending anything, ask:

- Is there a privacy policy?

- How is data stored?

- Is data encrypted?

- How long is it retained?

- Is it deleted after posting or after the order closes?

- Who has access to it?

If a company is sloppy about privacy, that matters as much as price. A cheap tradeline is not worth exposing your identity.

Step 7: Understand posting timelines before you pay

A normal buyer expectation is roughly 15 to 45 days for reporting in many cases.

That is because the process depends on when the seller adds you, the issuer’s next statement date, how quickly the issuer reports authorized-user data, and how each bureau updates.

This is why buying last-minute is usually a bad idea. If you have a hard deadline, a provider should be able to tell you the expected add date, statement date, and estimated reporting window.

If they cannot explain timing clearly, that is a bad sign. For a deeper look at posting timelines, see AU tradeline timing.

Step 8: Be realistic about score impact

This is the section most sales pages distort.

A tradeline can help a lot, a little, or not much at all. Realistic buyer expectations often look like this:

- Thin files: 50–250 points is possible

- Established profiles: often much less

- Damaged profiles with major negatives: highly variable, often disappointing

Thin files tend to benefit the most because the tradeline changes a larger share of the profile. A mature file with multiple accounts may see only modest movement. A badly damaged file may barely move because derogatories still dominate.

This is why “how many points will I gain?” is not really one question. It is several different questions depending on whether you have no credit history, a thin but clean file, a thick file with high utilization, or a file with late payments, collections, or charge-offs.

Step 9: Decide between one tradeline and a package

A lot of brokers push packages because bigger orders mean bigger revenue. But the honest answer is profile-specific.

One tradeline may be enough when:

- Your file is thin but otherwise clean

- You need one strong revolving account

- You want to test impact before spending more

- You have a targeted, moderate goal

A package may make more sense when:

- Your file is extremely thin

- You need more depth, not just one account

- You are trying to improve both age and overall revolving profile

- You are preparing for a higher-stakes application

Still, packages can be wasteful. Three random lines are not automatically better than one strong, well-matched line. That is why “should I buy one tradeline or a package?” should be answered by profile structure, not by bundle marketing. If your file is extremely thin, understanding the thin file problem can help you decide.

Step 10: Which issuer types are usually strongest?

Buyers often ask whether Amex, Chase, or Capital One is “best.”

The honest answer is that issuer matters some, but less than many buyers think. What matters more is:

- Clean history

- Low utilization

- Age

- Available limit

- Reliable authorized-user reporting

Major-bank lines often feel more desirable because they tend to have stronger limits and cleaner profiles. But the specific line matters more than the brand label by itself.

So instead of asking “Is Amex better than Chase?” ask: What is the age? What is the limit? What is the utilization? Does the issuer reliably report AUs? When is the next statement date?

Step 11: Know how long purchased tradelines stay on your report

Purchased tradelines are usually temporary.

A common market-style expectation is about 30 to 90 days for many commercial arrangements. Family authorized-user setups can remain indefinitely if the primary holder leaves you on the account, but purchased tradelines are often designed around a short reporting window.

That matters because some buyers assume the benefit will stay forever. Usually it will not.

When the tradeline is removed, your score may drop because the file loses some of the age, limit, or utilization benefit that account was contributing. How much it drops depends on how dependent your file became on that one line.

Step 12: Can you buy tradelines with no credit history?

Yes. In fact, this is one of the cases where tradelines may help the most.

If you have no credit history at all, a clean authorized-user tradeline can help create a more visible revolving profile. But that does not mean you should stop there. Long-term credit strength still requires primary accounts in your own name. For a full roadmap, see building credit from zero.

A bought tradeline can help open the door. It should not be the whole house.

Final buyer guidance

If you want the simplest version of how to buy tradelines, it is this:

- Check your reports first.

- Identify whether you need age, limit, utilization help, or depth.

- Compare tradeline companies based on contracts, timing, privacy, and business legitimacy.

- Avoid providers using cash-only or crypto-only payment setups.

- Expect realistic pricing—from about $200 to $3,000+ per line depending on the account.

- Plan for a typical 15–45 day reporting window in many cases.

- Do not expect guaranteed score gains.

- Use tradelines as one tool inside a broader credit strategy.

A good tradeline purchase is usually boring: clear fit, clear contract, clear timeline, clear privacy handling, clear expectations.

That is what smart buyers should optimize for.

For a broader view of all the fundamentals, return to the Credit Basics hub.

Tradelines That Actually Report

We focus on what actually moves credit scores: utilization, account age, and clean reporting. With 500+ successful placements and excellent reviews on TrustPilot ★★★★★, every tradeline is screened for reporting consistency before it is listed.