Why Do Authorized User Tradelines Help Some Credit Files More Than Others?

TL;DR:

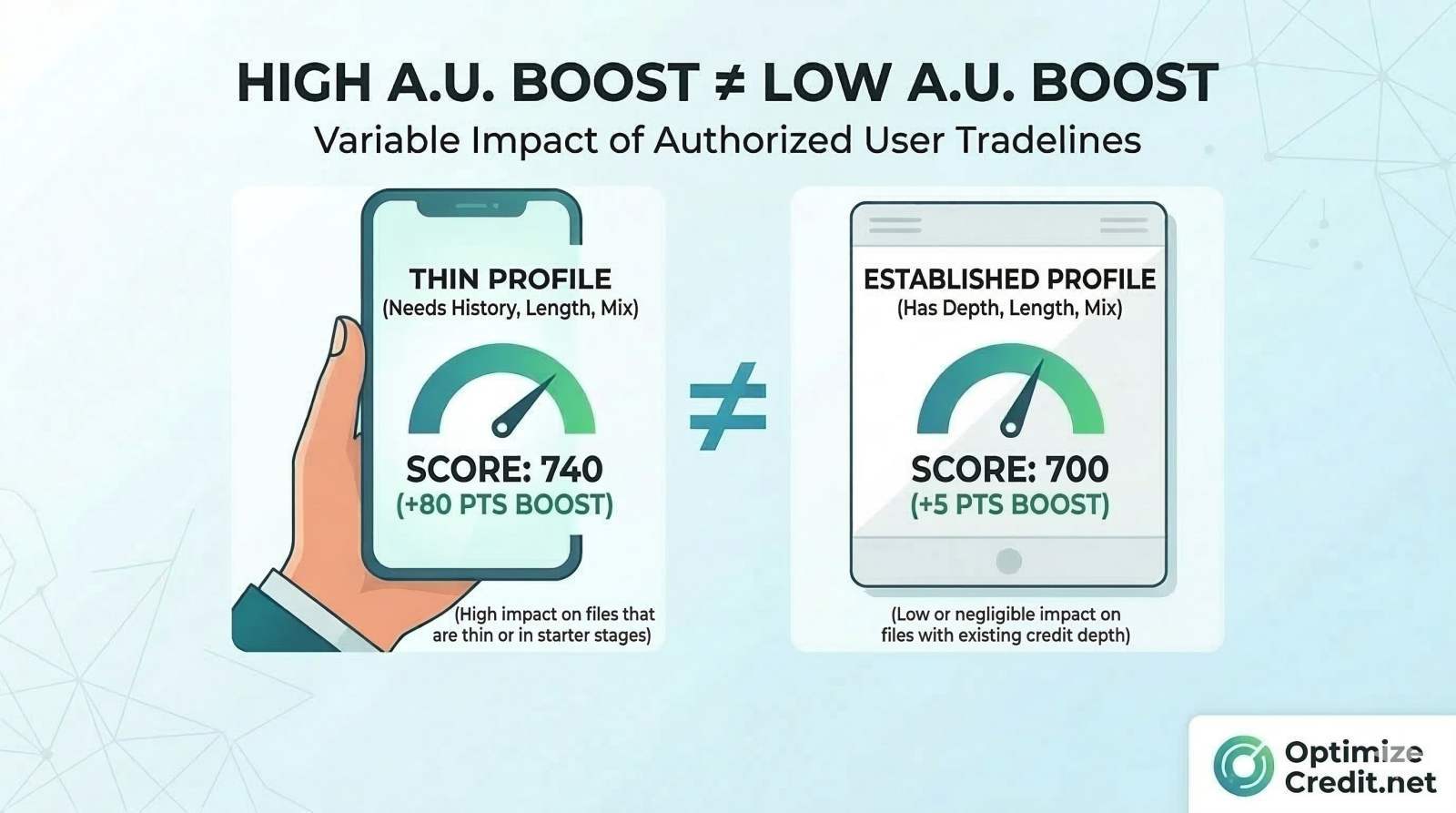

Authorized user tradelines do not affect every borrower the same way because credit scores respond to the overall file, not just the added account. Thin files, younger files, high utilization profiles, and weaker revolving depth often benefit more than already-strong profiles. The right tradeline can improve age, available credit, and revolving depth, but the impact depends on what is already helping or suppressing the file.

One of the biggest misconceptions about authorized user tradelines is that they work like a fixed point boost. They do not. A tradeline is not a magic coupon for your score. It works by changing parts of your credit profile that scoring models care about, such as account age, revolving depth, and utilization. If those are already strong, the gain may be limited. If those are weak, the same tradeline may have a much larger effect.

This is why two people can buy very similar tradelines and get very different results. One file may be missing mature revolving history. Another may already have strong age and low utilization, so the added line does much less. If you want a broader framework for hidden score suppressors, see our internal guide on credit score debugging and hidden score suppressors.

Why do tradeline results vary so much?

Credit scoring models do not judge a tradeline in isolation. They judge the entire file. That means the same added account can be highly meaningful in one file and only mildly helpful in another.

Common reasons the outcome varies include:

- the file is thin and lacks enough revolving accounts

- the borrower has high utilization and the added limit changes the ratio materially

- the borrower has short average age, so an older tradeline helps more

- the borrower already has good or excellent credit, so there is less room to improve

- negative items, recent late payments, or collections are still dragging the file

What parts of a file can a tradeline help?

An authorized user tradeline can potentially help in three core ways:

| Credit factor | How the tradeline may help | When the benefit is usually stronger |

|---|---|---|

| Account age | An older account can improve the age profile of a thinner or younger file. | When the borrower has few old revolving accounts or a very young file. |

| Available credit / utilization | A higher-limit line can reduce overall utilization if existing balances are high. | When revolving balances are elevated and utilization is suppressing the score. |

| Revolving depth | An added revolving account can strengthen a file that lacks enough bankcard depth. | When the borrower has a thin file, limited revolving history, or weak profile depth. |

Financial Disclosure: This guide is for educational purposes only and does not constitute legal or financial advice. I am not a financial advisor or a credit repair organization. While authorized user tradelines can positively impact credit factors like age and utilization, results vary significantly based on your individual credit profile. Credit score increases are not guaranteed, and you should consult with a qualified professional before making major financial decisions, such as applying for a mortgage.

FICO itself explains that scoring models evaluate categories such as payment history, amounts owed, length of credit history, new credit, and credit mix, which is why a tradeline helps only when it improves a weak part of the file rather than just adding noise. For a primary source overview, see FICO’s explanation of score factors here: What’s in your FICO Scores.

Which credit files usually benefit the most?

The strongest candidates are usually borrowers whose files are not yet fully developed. That often includes:

- thin-file borrowers with too few revolving accounts

- borrowers with short average age

- borrowers whose utilization is too high relative to their available credit

- borrowers near a meaningful lending threshold who need profile strengthening

In these cases, the right tradeline may materially improve how the scoring model reads the file because it addresses a real structural weakness.

Which files may see less impact?

Some borrowers see smaller gains, even when the tradeline is good quality. That usually happens when:

- the borrower already has strong age and strong revolving depth

- the score is already in a high range, so there is less room to improve

- major negatives like late payments, collections, or recent derogatories remain the main problem

- the buyer picked a tradeline that does not match the actual weakness in the file

In other words, a tradeline can be valuable, but it cannot fully overpower a file that is being dragged down by the wrong problem.

Quick comparison table

| File type | Likely tradeline impact | Main reason |

|---|---|---|

| Thin file with few revolving accounts | Often stronger | Added depth and mature history can change how the file is interpreted. |

| High-utilization profile | Often stronger | Higher available credit may improve utilization ratios meaningfully. |

| Young file with limited age | Often stronger | Older tradeline may improve age-related profile strength. |

| Already strong 750+ profile | Often smaller | The file may already be well optimized, leaving less room for gain. |

| File with major recent derogatories | Often limited | Negative items may remain the dominant suppressor. |

How should you choose the right tradeline?

The right choice depends on the weakness you are trying to address. If the problem is age, an older line matters more. If the problem is utilization, a stronger limit matters more. If the problem is a thin file, the best line is the one that improves overall revolving depth in a credible way.

This is why “best tradeline” is not one universal answer. It is file-specific. Choosing the wrong line can lead to disappointment even if the tradeline itself is legitimate and well-seasoned.

What should you check before buying?

Before buying a tradeline, it helps to ask:

- Is my main weakness age, utilization, or thin-file depth?

- Do I already have major negatives suppressing the score?

- Is my current score already high enough that improvement may be smaller?

- Am I choosing the line based on my file’s weakness rather than just the biggest number in the table?

Borrowers who answer those questions first usually make better purchases and have more realistic expectations.

FAQ

- Do authorized user tradelines help everyone the same way?

- No. The effect depends on the overall credit file. A thin or younger file often responds more strongly than a file that is already mature and well optimized.

- Why would one person get a bigger boost than another from the same line?

- Because the tradeline may be fixing a real weakness in one file but adding little in another. The scoring model looks at the full profile, not just the added account.

- Is older always better?

- Older is often better when account age is the weakness, but it is not the only factor. A borrower struggling mainly with utilization may benefit more from a stronger limit than from a modest age increase alone.

- Can a tradeline still help if I already have good credit?

- It can, but the impact is often smaller because the file may already be strong. The biggest gains usually happen when the tradeline addresses a real structural gap.

- What is the biggest mistake buyers make?

- The biggest mistake is buying based on the biggest age or limit without first identifying what is actually suppressing the file.