Authorized User Tradelines vs Credit Repair: When Each Works Better

A strategic comparison of fixing past credit history versus adding new positive data to improve scores in .

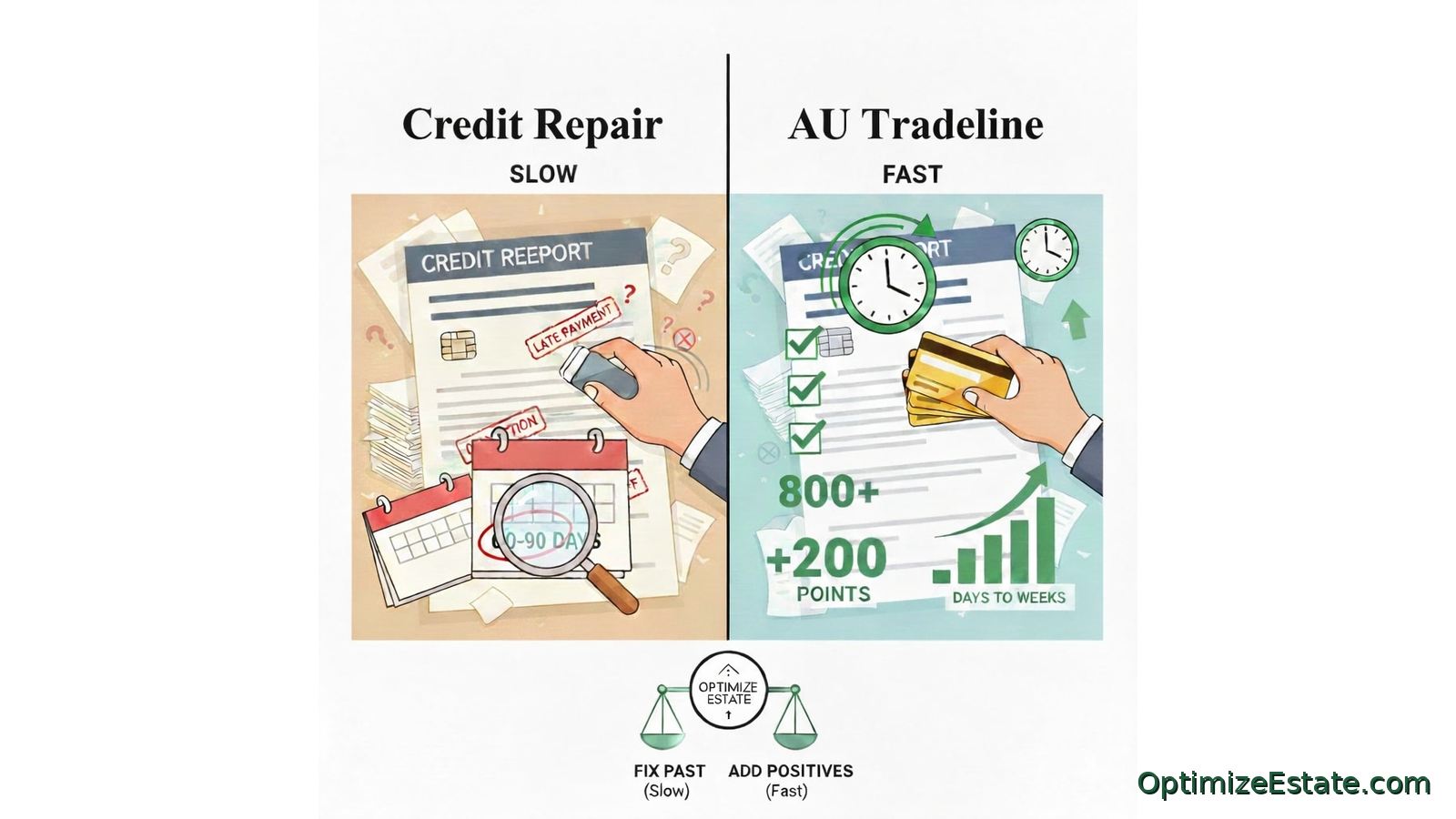

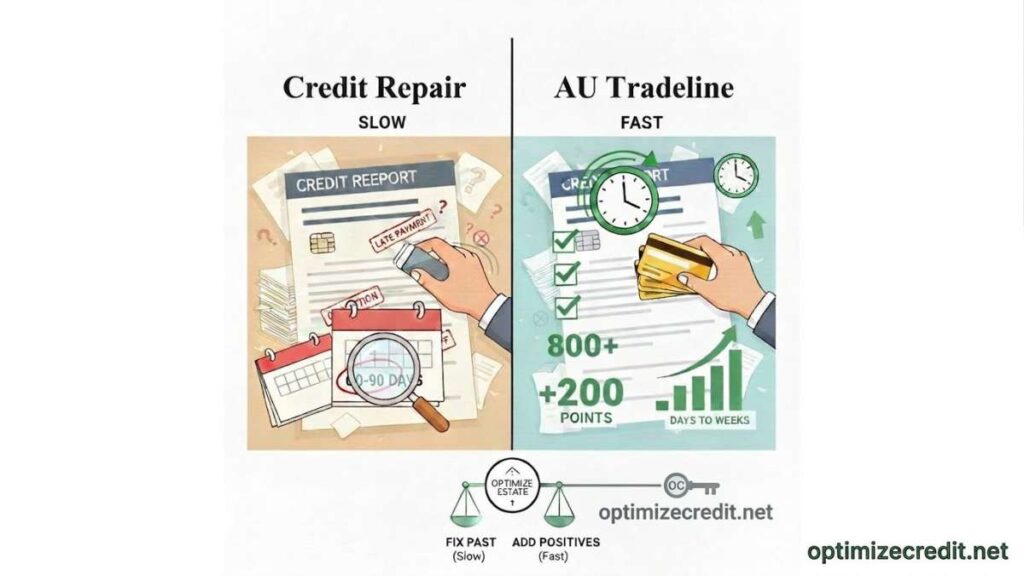

TL;DR: Credit repair focuses on removing or fixing past negative items (takes months). Authorized user tradelines add new positive history and higher limits (takes days to weeks). They are not competitors; they are tools used for different stages of credit improvement.

Two main ways people try to fix their credit

When someone wants to improve their credit score, they usually take one of two approaches. The first approach looks backward and focuses on fixing or correcting past problems on a credit report. This is commonly called credit repair. The second approach looks forward and focuses on adding new positive information to improve how the credit profile looks today. Authorized user tradelines fall into this category.

Credit repair focuses on past history

Credit repair means reviewing your credit report line by line and addressing negative or incorrect items. This applies whether an account is open or closed. A closed account can still hurt your score if it shows an unpaid balance, a charge-off, or a collection status. These often appear as “closed with balance,” “charged off,” or “collection account,” all of which signal unresolved obligations.

In some cases, you can contact the creditor or collection agency and negotiate a partial or full payment. After payment, the account may be updated to show the obligation as satisfied or settled. If an account is still open and past due, another option is to bring it current and request a goodwill adjustment.

Credit repair also includes disputing incorrect information with Experian, Equifax, and TransUnion. Even when everything goes smoothly, credit repair usually takes 60 to 90 days (or longer) before score changes appear.

Authorized user tradelines add positives

Authorized user tradelines work differently. Instead of fixing old problems, they add new positive information to your credit report. When you are added as an authorized user to a well-managed credit card, that account may appear on your credit report and strengthen your overall profile by adding higher credit limits, lower credit utilization, positive payment history, and older account age.

Tradelines do not remove collections or late payments, but they can offset them by improving how your credit looks today. Because tradelines often report within one billing cycle, the timeline can be much faster. Many people see movement within days to weeks once the account reports, depending on statement close dates and bureau update timing.

When tradelines are especially effective

Authorized user tradelines tend to be most effective for people with thin credit profiles, low credit limits, or high credit utilization. Students or borrowers with limited history can benefit from immediate increases in available credit and account age. People with high balances often see meaningful improvements when added credit limits reduce utilization. This is why many people with scores in the 500s or 600s see noticeable improvement once the right tradeline reports.

Which option should you choose?

Credit repair and authorized user tradelines are not competitors. They solve different problems. Credit repair fixes the past and takes time. Tradelines strengthen the present and can work faster. Many people use both by working on disputes and negotiations in the background while using tradelines to improve approval chances for time-sensitive needs.

Resources and references

For more detail on how authorized user tradelines work and when they make the most sense:

Advanced Guides & Deep Dives

Authorized User Tradelines Credit Boost (FICO)

Best if you want the full step-by-step framework and realistic outcomes.

How Long Do Authorized User Tradelines Take to Report?

Best if timing is your main constraint and you need a clear reporting timeline.

How Lenders Use Bureau Scores

Understand why you have three different scores and how lenders decide which bureau to pull.

Frequently Asked Questions

Do authorized user tradelines fix bad credit history?

No, authorized user tradelines do not fix or remove bad credit history from your report. They work by adding new, positive data—such as a high credit limit and a long history of on-time payments—to your profile. While this can offset the impact of negative items by improving your overall debt-to-credit ratio and account age, the original mistakes remain on your report until they expire or are removed through credit repair.

Is it better to use credit repair or tradelines?

It depends on your specific goals and timeline. If you have errors or old collections dragging you down, credit repair is the most permanent solution to cleaning up your profile. However, if you need a score increase within weeks for a pending loan or mortgage application, tradelines are often more effective because they typically report within one billing cycle, which is much faster than the 60- to 90-day dispute cycle.

Can I use both credit repair and tradelines at the same time?

Yes, many people use both strategies simultaneously to maximize their score improvement. You can work on disputing inaccuracies and negotiating with creditors in the background (the backward-looking approach) while adding a high-limit tradeline to strengthen your current profile (the forward-looking approach). This dual-path strategy addresses both the negative and positive aspects of your credit report at once for a more comprehensive result.

Will tradelines help if I have high credit utilization?

Yes, authorized user tradelines are particularly effective for individuals struggling with high credit utilization. By adding a credit card with a large limit to your profile, your overall utilization percentage drops significantly across your entire credit report. Since utilization is a major factor in FICO scoring, this reduction often leads to a fast and noticeable improvement in your score, provided the new account is managed responsibly.